Your dream college sent you an acceptance letter.

Engineering at VIT. MBA at IIM Bangalore. Computer Science at the University of Toronto. Medicine at a leading private college. Whatever the institution — the next line in the letter is always the same: the fee structure that makes your heart sink a little.

₹8 lakhs. ₹25 lakhs. ₹60 lakhs. ₹1.2 crore.

For most Indian families — these numbers are not in the savings account. And yet, across the country and across developing markets, millions of students fund exactly these dreams every year through education loans — one of the most powerful, most tax-efficient, and most misunderstood financial products available.

The education loan calculator cuts through the confusion. It shows you — before you sign anything — exactly what your monthly EMI will be after your course ends, the true total cost of your education financing, and whether the career income you expect after graduation justifies the loan you are considering.

Here is the complete guide to everything an education loan borrower needs to know.

👉 Calculate your education loan EMI and total repayment cost with our free Education Loan Calculator →

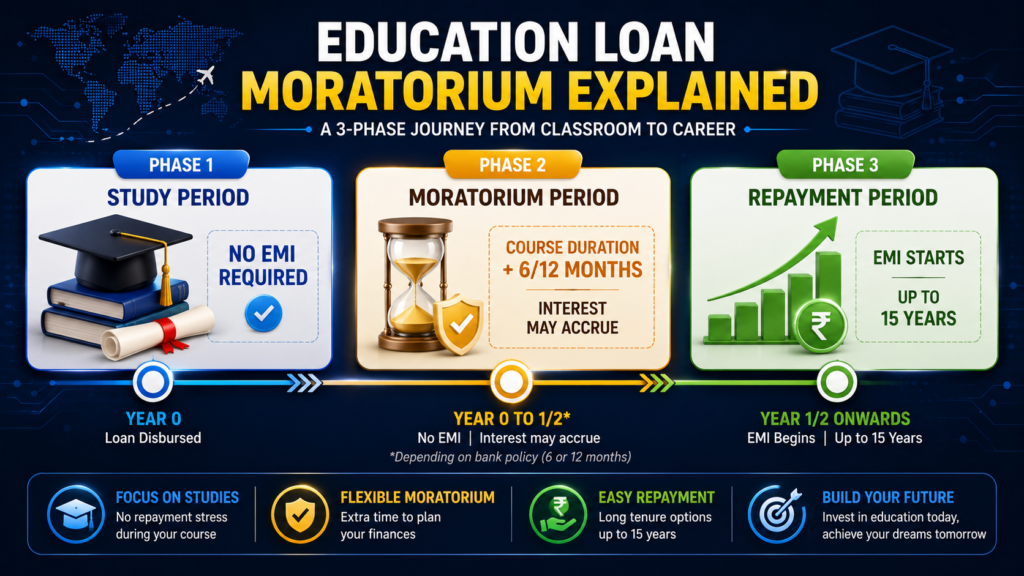

How an Education Loan Works: The Unique Structure

Education loans are fundamentally different from personal loans and home loans in one critical way: the moratorium period — a built-in repayment holiday that aligns with your financial reality as a student.

Education Loan Timeline:

Phase 1 — Study Period

EMI: Zero (no repayment while studying)

Interest: Accrues on the outstanding loan amount

Phase 2 — Moratorium Period

Duration: Course duration + 6 months (most banks) or + 12 months (SBI)

EMI: Zero (still no repayment required)

Interest: Continues to accrue — SIMPLE interest during this period (most banks)

Phase 3 — Repayment Period

Duration: 5 to 15 years depending on loan amount and bank

EMI: Full EMI (principal + interest) begins

Tax Benefit: Section 80E deduction on entire interest paid

Total Moratorium = Course Duration + 6 or 12 Months

Example: 4-year B.Tech + 6 months moratorium = EMI starts in Month 55This structure is specifically designed for students — you study without financial pressure, find employment, begin earning, and then start repaying from income. No other loan product offers this genuine alignment with your life stage.

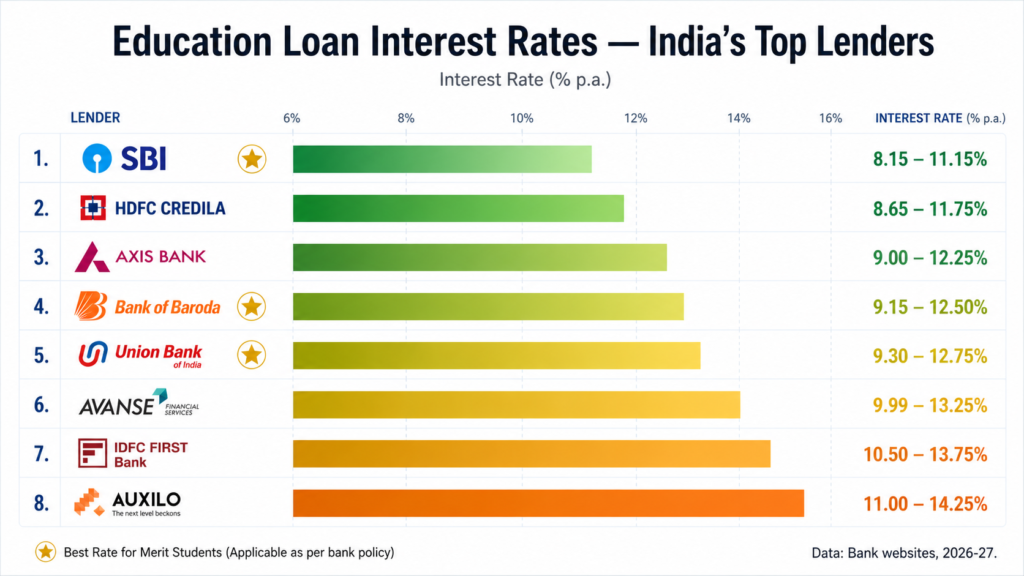

Education Loan Interest Rates: Complete Lender Comparison

Interest rates on education loans vary by lender, loan amount, course type, and institution ranking. Here is the current landscape:

| Lender | Interest Rate | Processing Fee | Max Amount | Key Advantage |

|---|---|---|---|---|

| SBI Scholar Loan | 8.15–11.15% | Nil for premier institutes | ₹40 lakhs (India), ₹1.5 crore (abroad) | Lowest rates; IIT/IIM/AIIMS etc. get best rates |

| Bank of Baroda | 8.15–10.65% | 1% (max ₹10,000) | ₹80 lakhs | Strong for study abroad |

| Union Bank of India | 8.30–11.30% | 0.5% | ₹40 lakhs | Good rates for Tier-2 institutions |

| HDFC Credila | 10.50–13.75% | 0.5–1.5% | No upper limit | No collateral for select institutions |

| Axis Bank | 13.70–15.20% | Up to 2% | ₹75 lakhs | Fast processing |

| Avanse Financial | 11.00–14.50% | Up to 2% | No upper limit | Flexible — accepts wide range of courses |

| IDFC First Bank | 10.00–14.00% | 1.5% | ₹50 lakhs | Good for non-traditional courses |

| Auxilo Finserve | 12.00–16.00% | 1–2% | ₹2 crore | Premium study abroad specialist |

Government bank vs private lender — the real difference:

On a ₹15 lakh education loan for 5 years — the monthly EMI difference between SBI (8.5%) and a private NBFC (14%) is ₹3,012 per month and ₹1,80,720 in total interest over the repayment period. This is not a trivial difference — it represents two months of EMI-free income every year.

The merit institution advantage: SBI, Bank of Baroda, and Union Bank offer significantly lower rates for students admitted to listed premier institutions (IITs, IIMs, NITs, AIIMS, NLUs). If you are admitted to a premier institution — always start your loan inquiry with PSU banks.

Education Loan Calculator: Understanding Your Numbers

The education loan calculator produces outputs that are very different from a standard EMI calculator — because the moratorium period fundamentally changes the math:

The Interest Capitalisation Question

During the moratorium period, interest accrues on your outstanding loan. Most banks collect simple interest during this period. If you do not pay this interest as it accrues — it gets added to your principal at the start of repayment (capitalised), making your effective loan amount larger than what you originally borrowed.

Example:

Original Loan: ₹15,00,000 at 10% p.a.

Study Period: 4 years

Moratorium Addition: 6 months

Total Moratorium: 4.5 years = 54 months

Interest Accrued During Moratorium (simple interest):

₹15,00,000 × 10% × 4.5 years = ₹6,75,000

If NOT paid during moratorium — principal at repayment start:

₹15,00,000 + ₹6,75,000 = ₹21,75,000

EMI on ₹21,75,000 at 10% for 10 years: ₹28,737/month

Total repaid: ₹34,48,440

If interest PAID during moratorium (₹12,500/month):

Principal at repayment: ₹15,00,000 (unchanged)

EMI on ₹15,00,000 at 10% for 10 years: ₹19,819/month

Total repaid: ₹23,78,280 + ₹6,75,000 already paid = ₹30,53,280

Saving from paying moratorium interest: ₹3,95,160The single most powerful education loan advice: If you can arrange to pay the simple interest during the moratorium period — even partially — you save lakhs in total repayment. Many students find part-time or internship income during their studies that can cover this interest.

👉 Calculate your exact moratorium interest and post-study EMI with our Education Loan Calculator →

Domestic vs Study Abroad: How the Numbers Differ

The education loan landscape changes significantly based on whether you are studying in India or abroad:

| Parameter | Study in India | Study Abroad |

|---|---|---|

| Average Course Cost | ₹5–₹20 lakhs (4-year professional) | ₹30–₹1.5 crore (1–2 year Master’s) |

| Loan Amount — No Collateral | Up to ₹7.5 lakhs (most banks) | Up to ₹4 lakhs (extremely limited) |

| Loan Amount — With Collateral | Up to ₹40 lakhs | Up to ₹1.5 crore (SBI), no limit (HDFC Credila) |

| Interest Rate Range | 8.15–14% | 10.5–16% |

| Typical Moratorium | Course + 6 months | Course + 6 months (or 1 year after getting job) |

| Currency Risk | None | Present — course fees in USD/GBP/AUD |

| Repayment Period | 5–15 years | 5–15 years |

| Tax Benefit (80E) | Yes — full interest deductible | Yes — full interest deductible |

Study Abroad: The Currency Risk Factor

When you take an education loan for an overseas degree — the fees are in a foreign currency (USD, GBP, CAD, AUD). Your loan may be disbursed in Indian Rupees, converted at the time of each fee payment.

If the rupee depreciates 10% during your 2-year course — a course that cost ₹60 lakhs at the start now effectively costs ₹66 lakhs. This currency risk is real and must be factored into your education loan planning.

Mitigation: Some banks (HDFC Credila, Avanse) offer foreign currency education loans disbursed directly in USD — eliminating conversion risk for overseas fee payments. Evaluate this option for large study-abroad loans.

Section 80E: The Unique Tax Benefit That Makes Education Loans Special

The Section 80E income tax deduction is one of the most generous provisions in the Income Tax Act — and it is exclusively available for education loan borrowers:

| Feature | Section 80E Education Loan Deduction |

|---|---|

| What is deductible | Entire interest paid during the financial year |

| Maximum deduction | No upper limit — 100% of interest paid |

| Duration | Up to 8 consecutive assessment years from repayment start |

| Available for | Self, spouse, children, or student for whom you are legal guardian |

| Loan from | Financial institution or approved charitable institution (NOT informal) |

| Tax regime | Old regime only |

Section 80E in Action:

Year 1 of repayment:

Annual interest paid: ₹1,60,000

Section 80E deduction: ₹1,60,000 (full amount — no cap)

Tax saved at 20% bracket: ₹33,280

Tax saved at 30% bracket: ₹49,920

Over 8 years of repayment (if interest averages ₹1,20,000/year):

Total interest deducted: ₹9,60,000

Total tax saved (20% bracket): ₹1,99,680

Total tax saved (30% bracket): ₹2,99,520An education loan borrower in the 30% tax bracket who pays ₹1.6 lakhs of interest in the first year of repayment saves ₹49,920 in income tax — effectively reducing their net interest rate from 10.5% to approximately 7.35%.

This makes education loans even more competitive than their headline interest rate suggests — particularly for borrowers who quickly enter higher income brackets after graduating from premium institutions.

👉 Related Reading: Income Tax Calculator — Save Maximum Tax Legally → — understanding how Section 80E fits into your complete tax planning.

Real EMI Examples: Education Loan Calculator Results

Scenario 1: B.Tech at NIT — ₹8 Lakh Loan

| Detail | Value |

|---|---|

| Loan Amount | ₹8,00,000 |

| Interest Rate | 9% (Bank of Baroda, NIT — merit category) |

| Study Period | 4 years |

| Moratorium | 4 years + 6 months = 54 months |

| Repayment Tenure | 10 years |

| Interest accrued during moratorium (if unpaid) | ₹3,60,000 |

| Effective principal at repayment start | ₹11,60,000 |

| Monthly EMI | ₹14,690 |

| Total Amount Repaid | ₹17,62,800 |

| Section 80E saving over 8 years (20% bracket) | ₹1,20,000 (approx) |

| Net effective cost after tax | ₹16,42,800 |

Scenario 2: MBA Abroad (USA) — ₹60 Lakh Loan

| Detail | Value |

|---|---|

| Loan Amount | ₹60,00,000 |

| Interest Rate | 12% (HDFC Credila — with collateral) |

| Study Period | 2 years |

| Moratorium | 2 years + 6 months = 30 months |

| Repayment Tenure | 12 years |

| Interest accrued during moratorium (if unpaid) | ₹18,00,000 |

| Effective principal at repayment start | ₹78,00,000 |

| Monthly EMI | ₹1,04,895 |

| Total Amount Repaid | ₹1,51,04,880 |

| Section 80E saving over 8 years (30% bracket) | ₹5,40,000 (approx) |

| Net effective cost after tax | ₹1,45,64,880 |

The MBA abroad ROI check: At ₹1,04,895 monthly EMI — you need a starting salary after graduation that comfortably covers this. The generally accepted benchmark: your first year’s post-graduation salary should exceed the total education loan amount. A ₹60 lakh loan requires a ₹60 lakh+ annual salary to be financially justified — achievable for top MBA programs, but requiring careful research before committing.

Government Education Loan Schemes: India

The Indian government has several schemes specifically designed to make education loans more accessible and affordable:

| Scheme | Benefit | Eligibility |

|---|---|---|

| PM Vidyalaxmi Scheme (2024) | 3% interest subvention for loans up to ₹10 lakhs for students from top 860 institutes | NIRF-ranked institutions; family income up to ₹8 lakhs/year |

| Central Sector Interest Subsidy (CSIS) | Full interest subsidy during moratorium for loans up to ₹7.5 lakhs | Family income below ₹4.5 lakhs/year; studying in India |

| Padho Pardesh | Interest subsidy for study abroad loans for minority students | Economically weaker minority students |

| Dr. Ambedkar Central Scheme | Interest subsidy for OBC/EBC students going abroad | OBC/EBC students with family income below ₹3 lakhs/year |

| State-specific schemes | Various — some states offer 0–2% interest for first-generation graduates | Varies by state |

The PM Vidyalaxmi Scheme (launched November 2024) is the most significant recent development — providing a 3% interest subvention (rate reduction) on loans up to ₹10 lakhs for students at NIRF-ranked institutions, with family income below ₹8 lakhs. This effectively brings the SBI rate down from 8.5% to 5.5% for eligible students — making education loans extraordinarily affordable.

Always check your eligibility for government schemes before finalising your education loan — the interest saving can be ₹50,000–₹2,00,000 over the repayment period.

How to Choose the Right Education Loan: 6-Step Framework

Step 1 — Calculate the total education cost (not just tuition)

Tuition is only part of your loan requirement. A complete education cost estimate includes:

| Cost Component | Domestic | Abroad |

|---|---|---|

| Tuition Fee | Major component | Major component |

| Hostel / Accommodation | ₹60,000–₹1,50,000/year | ₹4–₹12 lakhs/year |

| Exam/Lab/Library Fees | ₹10,000–₹30,000/year | ₹50,000–₹1 lakh/year |

| Books and Stationery | ₹15,000–₹30,000/year | ₹50,000–₹1 lakh/year |

| Travel (to/from home) | ₹20,000–₹50,000/year | ₹1–₹3 lakhs/year |

| Health Insurance | ₹5,000–₹15,000/year | ₹1–₹2 lakhs/year |

| Living Expenses | ₹60,000–₹1,20,000/year | ₹6–₹18 lakhs/year |

Many students under-borrow initially — taking a loan for just tuition — and then scramble for emergency personal loans mid-course. Borrow the complete amount from the start.

Step 2 — Calculate your post-graduation EMI capacity

Before taking any education loan — project your expected starting salary and apply the 30% EMI rule:

Expected starting salary: ₹8,00,000/year = ₹66,667/month

Safe EMI (30% of monthly): ₹20,000/month

Maximum loan supportable (10%, 10 years): ₹15,00,000 approxIf your projected loan amount produces an EMI above 30% of your expected starting salary — you need to either find a more affordable program, increase the repayment tenure, or seek scholarships.

Step 3 — Check collateral requirements

| Loan Amount | Typical Collateral Requirement |

|---|---|

| Up to ₹4 lakhs | None — third-party guarantee may be required |

| ₹4–₹7.5 lakhs | Third-party guarantee (parent or guardian) |

| ₹7.5 lakhs–₹15 lakhs | Collateral required (property, FD, LIC) |

| Above ₹15 lakhs | Collateral mandatory — higher value collateral |

For study abroad loans above ₹20–₹30 lakhs — ensure your collateral (property valuation, FD, etc.) comfortably exceeds the loan amount as lenders typically lend up to 75–85% of collateral value.

Step 4 — Compare at least 3 lenders before deciding

Never accept the first loan offer. Compare at minimum: SBI or Bank of Baroda (best government bank rates), your relationship bank (may offer loyalty discounts), and one specialist education loan NBFC (for speed or institutions government banks may not cover).

Step 5 — Understand the complete terms

Read the fine print on: interest rate type (fixed or floating), prepayment penalty (most education loans allow prepayment without penalty), default consequences (impact on parents’ credit score as co-borrowers), and what constitutes a valid expense for disbursement.

Step 6 — Apply early — at least 3 months before fees are due

Education loan processing takes 2–6 weeks for documented applications at PSU banks. NBFC processing is faster (3–7 days) but at higher rates. Apply early to avoid fee payment delays that universities are increasingly inflexible about.

Education Loan Repayment Strategies: Clear It Faster

Strategy 1: Pay Moratorium Interest as You Go

As discussed — paying simple interest during the moratorium period prevents capitalisation and saves lakhs. If you earn anything during your studies (internship stipend, part-time work, scholarship disbursement above fees) — direct it here first.

Strategy 2: Step-Up Repayment Aligned With Career Growth

Many banks offer step-up repayment for education loans — lower EMIs in early career years that gradually increase. This aligns with career salary growth and makes the first 2–3 years of repayment more manageable.

Strategy 3: Prepay Aggressively in Peak Earning Years

Education loans typically have no prepayment penalty — unlike home loans with fixed rates. When you receive a salary hike, annual bonus, or variable pay — direct a portion toward prepayment. Each prepayment reduces the principal on which interest accrues.

Example: ₹15 lakh loan, 10% rate, 10-year repayment

Standard EMI: ₹19,819/month

Total interest without prepayment: ₹8,78,280

Annual prepayment of ₹50,000 (bonus):

Loan closes in 7.5 years instead of 10

Interest saved: ₹2,41,000

Total saving: ₹2,41,000Strategy 4: Claim Section 80E Every Year Without Fail

File your ITR every year and claim the full Section 80E deduction on interest paid. This is automatic money — the government literally rebates a portion of your education loan interest. Do not miss it for 8 straight years of repayment.

👉 Related Reading: Tax-Saving Investment Calculator — 5 Best Options → — integrating education loan tax benefits with your overall tax strategy.

Education Loan ROI: Is Your Course Worth the Debt?

This is the question most students never ask — and should always ask before signing any large education loan:

Education Loan ROI Framework:

Step 1: Total education loan cost (principal + interest)

Step 2: Expected starting salary at graduation

Step 3: Salary growth over 5 years (realistic trajectory)

Step 4: EMI as % of starting salary (should be below 30%)

Step 5: Break-even analysis (when cumulative salary benefit > loan cost)

Example — MBA from Top-20 B-School:

Loan: ₹30 lakhs at 10%, 10 years

Total repayment: ₹47.76 lakhs

Expected starting salary: ₹18–₹25 lakhs/year

Pre-MBA salary: ₹6–₹8 lakhs/year

Annual salary uplift: ₹12–₹17 lakhs

Break-even: ₹47.76 lakhs ÷ ₹14 lakhs avg uplift = 3.4 years

Verdict: Strong ROI — break-even in 3–4 years| Course | Avg Loan | Avg Starting Salary Post-Study | EMI (₹ per month) | Break-Even |

|---|---|---|---|---|

| IIT B.Tech (4yr) | ₹8–₹12 lakhs | ₹8–₹20 lakhs | ₹10,500–₹15,800 | 1–2 years |

| IIM MBA (2yr) | ₹25–₹35 lakhs | ₹18–₹35 lakhs | ₹33,000–₹46,000 | 2–3 years |

| Medical MBBS Private (5yr) | ₹40–₹80 lakhs | ₹6–₹12 lakhs (early career) | ₹53,000–₹1,06,000 | 7–12 years |

| MS in USA (2yr) | ₹50–₹80 lakhs | ₹30–₹50 lakhs equiv. | ₹66,000–₹1,05,000 | 2–4 years |

| Law (NLU, 5yr) | ₹10–₹15 lakhs | ₹8–₹15 lakhs | ₹13,000–₹20,000 | 2–4 years |

The MBBS caution: Medical education loans are among India’s largest (₹40–₹80 lakhs at private colleges) but early-career doctor salaries are relatively low. The EMI as a percentage of starting salary can exceed 50%+ — creating genuine financial stress in the first years of practice. Medical students should plan loan repayment with realistic early-career income projections, not peak earning projections.

Education Loan Across Developing Markets: Global Guide

Education financing approaches vary dramatically across developing markets:

| Country | Primary Loan Source | Interest Rate | Unique Feature |

|---|---|---|---|

| 🇮🇳 India | PSU Banks + NBFCs | 8.15–16% | Section 80E deduction; government subsidies |

| 🇵🇭 Philippines | CHED UniFAST, SSS | 0–8% (government) | Government scheme offers near-zero rate |

| 🇳🇬 Nigeria | NELFUND (new 2024), commercial banks | 8–15% | NELFUND launched 2024 for federal universities |

| 🇧🇷 Brazil | FIES (Government), ProUni (scholarship) | 3.4% (FIES) | Government scheme — very low rates |

| 🇰🇪 Kenya | HELB (Higher Education Loans Board) | 4% | Government lender with income-based repayment |

| 🇵🇰 Pakistan | HEC, commercial banks | 3% (HEC) + commercial | Government scheme for select universities |

Kenya’s HELB stands out — with a 4% fixed rate and income-contingent repayment (repayment scales with salary), it is one of the most student-friendly education loan systems in the developing world. Nigeria’s newly launched NELFUND (2024) is an important step for a country where commercial education lending has been prohibitively expensive.

Frequently Asked Questions

Q: What is the maximum education loan I can get without collateral?

A: Under RBI guidelines, banks can offer education loans up to ₹7.5 lakhs without collateral (third-party guarantee from parents is sufficient). For premier institutions under government schemes, some banks extend collateral-free loans up to ₹10–₹15 lakhs. NBFCs like HDFC Credila and Avanse may offer higher collateral-free amounts based on the institution’s reputation and your academic profile.

Q: When does the education loan EMI start?

A: EMI starts after the moratorium period ends — which is your course duration plus 6 months (most banks) or 12 months (SBI). For a 4-year B.Tech with 6-month moratorium, your first EMI is due in Month 55 (4 years + 6 months + 1 month). Some banks allow you to choose when repayment starts within the moratorium window.

Q: Does taking an education loan affect my parents’ CIBIL score?

A: Yes — if your parents are co-borrowers (which most lenders require), any default or delayed payment affects their CIBIL score equally. Many parents have had their home loan applications rejected because of a child’s education loan default. Treat the education loan as a serious family financial commitment.

Q: Can I get a top-up on my education loan if costs increase?

A: Most banks allow a top-up loan during the study period if initial costs increase (fee revision, additional living expenses). You need to provide updated fee receipts and cost estimates. The top-up is typically processed within the same loan account at the same interest rate.

Q: Is education loan interest rate fixed or floating?

A: Most Indian education loans are on a floating rate — linked to the bank’s MCLR or repo rate. This means your rate can increase or decrease with RBI policy changes. SBI’s education loan rate is explicitly repo-linked — rate cuts are passed on quickly. Some NBFCs offer fixed-rate education loans at slightly higher starting rates — useful if you want repayment certainty.

Q: What happens if I do not get a job immediately after graduation?

A: Contact your lender immediately and request a moratorium extension — most banks allow an additional 1–2 year extension for genuine unemployment post-graduation. The interest continues to accrue. Some schemes (CSIS) extend the interest subsidy during this period for eligible borrowers. Do not default — it damages both your and your parents’ credit score for years.

Conclusion

An education loan is not debt — it is an investment in your most valuable asset: your earning capacity.

A ₹15 lakh education loan at IIT or IIM that opens a career earning ₹15–₹25 lakhs annually generates a return on investment that no stock, mutual fund, or property can match. The Section 80E tax deduction that comes with it reduces the effective cost further. And the moratorium period gives you the breathing room to graduate, find employment, and begin repaying from actual earned income.

But — like all investments — it requires clarity before commitment. Calculate your total cost accurately. Project your realistic starting salary honestly. Ensure the EMI is below 30% of your expected monthly income. Apply for every government subsidy you qualify for. And pay moratorium interest during your studies whenever you can afford to.

The education loan calculator does not just tell you what your EMI will be. It tells you whether your educational investment makes financial sense — before you spend years of your career repaying the answer.

Use it before you decide. Not after.

👉 Calculate your education loan EMI and total cost with our free Education Loan Calculator →

👉 Related Reading: How to Calculate EMI for Personal Loan →

👉 Related Reading: Best Loan Tenure — Short vs Long EMI Calculator →

👉 Related Reading: Income Tax Calculator — Save Maximum Tax Legally →

👉 Related Reading: Personal Loan vs Credit Card — Which Is Cheaper? →

👉 Related Reading: What Happens If You Miss an EMI Payment? →

👉 Related Reading: Financial Calculator Guide for First-Time Earners in Asia & Africa →