You own a property worth ₹80 lakhs.

Your savings account has ₹3 lakhs.

And you need ₹30 lakhs — for your child’s overseas education, to expand your business, to consolidate high-interest debt, or to handle a medical situation that cannot wait.

Most people in this situation do two things: they borrow at 20%+ from personal loan lenders, or they seriously consider selling the property they have spent years building equity in.

There is a third option that most people overlook entirely — a Loan Against Property (LAP).

Your property is not just a place to live or a long-term investment. It is a financial asset that can be activated today — generating large, long-tenure loans at rates far below personal loans — without you giving up ownership, vacating the premises, or disrupting your life in any way.

The LAP calculator shows you exactly how much you can borrow, what your monthly EMI will be, and whether this powerful financial tool fits your specific situation.

👉 Calculate your exact LAP loan amount and EMI with our free Loan Against Property Calculator →

What Is a Loan Against Property?

A Loan Against Property is a secured loan where you pledge your existing property — residential house, commercial shop, office space, or land — as collateral to borrow a large sum. You continue to occupy and use the property throughout the loan tenure. The lender only exercises their rights over the property if you default and fail to resolve the default after due process.

LAP Core Formula:

Maximum Loan Amount = Property Market Value × LTV Ratio

Where:

LTV (Loan-to-Value) = Percentage of property value the bank will lend

Typical LTV: 50–75% depending on property type and lender

Example:

Residential property market value: ₹80,00,000

LTV ratio (65%): 0.65

Maximum LAP: ₹80,00,000 × 65% = ₹52,00,000Unlike a home loan (which funds the purchase of a new property), LAP uses an already-owned property as security for a loan that can be used for any legitimate purpose — business, education, medical, debt consolidation, renovation, or personal financial need.

The LTV Ratio: The Most Important LAP Number

The Loan-to-Value (LTV) ratio determines how much of your property’s market value the bank will actually lend you. Understanding this number before you approach any lender prevents the most common LAP surprise: discovering you qualify for less than you expected.

| Property Type | Typical LTV Range | Maximum Loan |

|---|---|---|

| Self-occupied residential | 60–75% | Up to ₹5 crore (most banks) |

| Rented residential | 55–70% | Up to ₹5 crore |

| Commercial property (shop/office) | 50–65% | Up to ₹3 crore |

| Industrial property | 50–60% | Up to ₹2 crore |

| Plot / Land (residential zone) | 50–60% | Up to ₹2 crore |

| Mixed-use property | 50–60% | Lender-specific |

Why LTV varies by property type:

Residential properties have the highest LTV because they are the most liquid — easiest to value accurately and sell quickly if needed. Commercial properties are harder to sell in a distress situation, so lenders apply a more conservative LTV. Agricultural land often does not qualify for LAP at all at most scheduled banks.

The valuation catch: Banks do not lend against your purchase price or your personal estimate of value. They send an independent, empanelled valuer who determines the current fair market value — which may be lower than you expect, particularly for older properties or those in areas with limited recent transaction data. Always factor in a 10–20% valuation haircut from your optimistic estimate when planning your LAP requirement.

LAP Interest Rates 2025: Lender-by-Lender Comparison

| Lender | Interest Rate | LTV Offered | Max Tenure | Processing Fee |

|---|---|---|---|---|

| SBI | 9.15–11.30% | Up to 65% | 15 years | 1% (max ₹50,000) |

| HDFC Bank | 9.50–11.00% | Up to 70% | 15 years | 1–1.5% |

| ICICI Bank | 9.85–11.25% | Up to 70% | 15 years | 1% |

| Axis Bank | 9.90–12.00% | Up to 65% | 15 years | 1% |

| Bajaj Housing Finance | 9.75–14.00% | Up to 75% | 18 years | 0.35% |

| Piramal Finance | 10.50–14.00% | Up to 70% | 10 years | 1.5–2% |

| L&T Finance | 10.00–13.50% | Up to 65% | 15 years | 1% |

| LIC Housing Finance | 9.50–11.00% | Up to 65% | 15 years | 0.5% |

The rate range matters: On a ₹40 lakh LAP over 15 years — the difference between SBI’s 9.5% and a higher-rate NBFC’s 14% is ₹13,250 per month in EMI and over ₹23.85 lakhs in total interest paid. This is a number worth taking 2–3 weeks to secure the right lender.

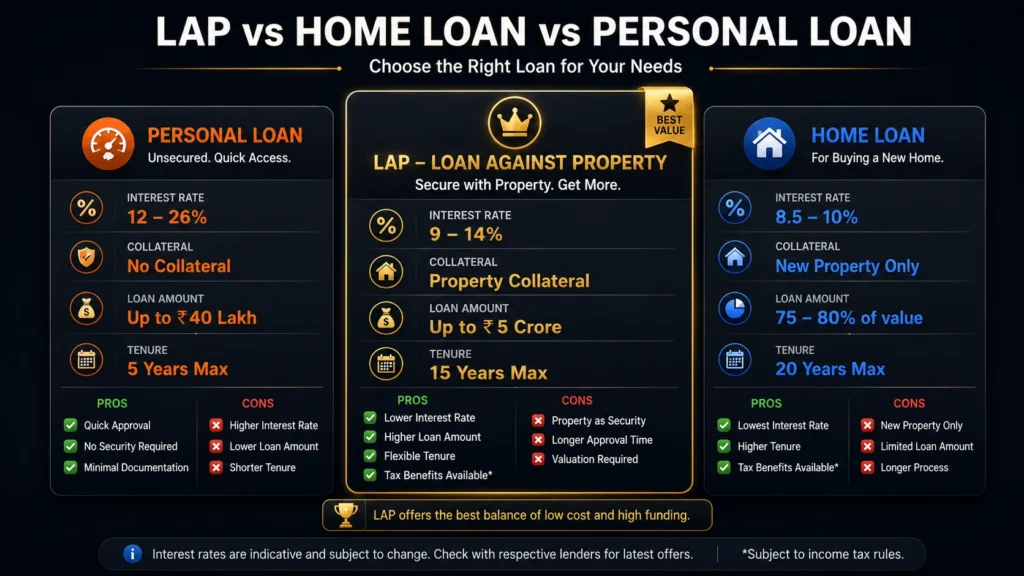

LAP vs Home Loan vs Personal Loan: Which Is Right for You?

This is the comparison every large-amount borrower must run before choosing their borrowing instrument:

| Parameter | Personal Loan | Loan Against Property | Home Loan |

|---|---|---|---|

| Purpose | Any | Any legitimate purpose | New property purchase only |

| Security | None | Existing property | New property being purchased |

| Interest Rate | 12–26% p.a. | 9–14% p.a. | 8.5–10% p.a. |

| Loan Amount | ₹50K–₹40L | ₹5L–₹5 crore | Based on property value |

| Tenure | Up to 5 years | Up to 15–18 years | Up to 30 years |

| EMI (₹30L, best rate) | ₹67,124 (12%, 5yr) | ₹30,448 (9.5%, 15yr) | ₹26,935 (8.5%, 20yr) |

| Property Ownership | Not required | Must own property | Acquired through the loan |

| Tax Benefit on Interest | None (personal use) | Business: deductible; Personal: none | Section 24(b) — up to ₹2L p.a. |

| Approval Time | 1–3 days | 7–21 days | 7–30 days |

| Credit Score Required | 720+ preferred | 700+ | 700+ |

The critical insight from the EMI comparison above: A ₹30 lakh personal loan at 12% for 5 years costs ₹67,124/month. The same amount as a LAP at 9.5% for 15 years costs just ₹30,448/month — less than half the monthly EMI. This is why large-amount borrowers with property ownership should almost always evaluate LAP before accepting personal loan terms.

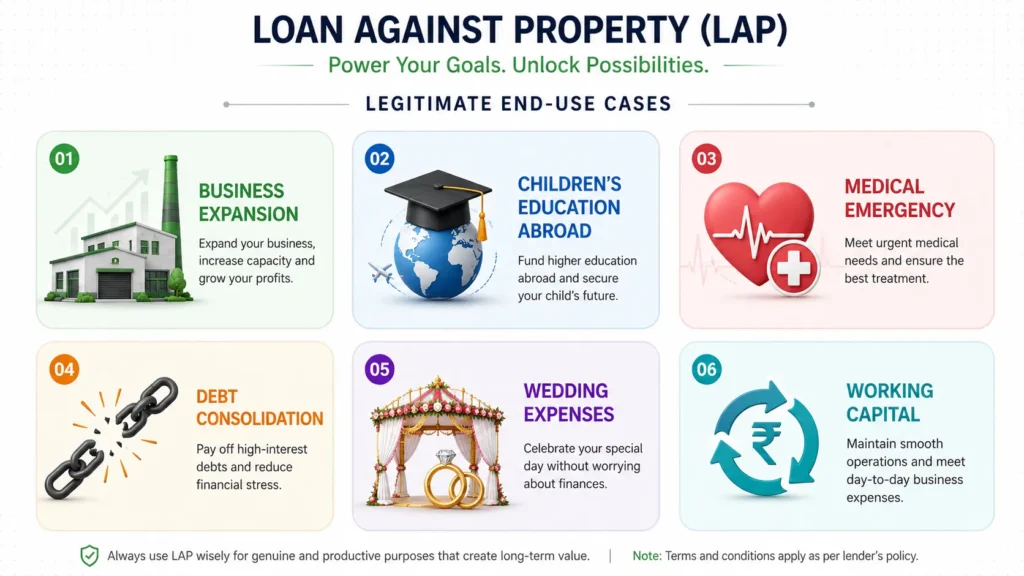

What Can You Use a LAP For?

One of LAP’s most significant advantages over a home loan is its complete flexibility of end use. While a home loan can only fund a property purchase, LAP proceeds can be deployed for virtually any legitimate financial need:

High-Value Use Cases Where LAP Makes Clear Sense

Business Expansion:

If your business needs ₹25–₹50 lakhs for machinery, inventory, or a new outlet — LAP at 10% significantly undercuts unsecured business loan rates of 15–25%. The entire interest is tax-deductible as a business expense.

Children’s Overseas Education:

Education loans for premium international programs can be slow to process and have strict eligibility. A LAP provides faster access to ₹30–₹80 lakhs at rates competitive with education loans — without the moratorium complexity.

Debt Consolidation:

If you have multiple high-interest debts — personal loans at 18%, credit cards at 36%, business loans at 22% — consolidating them into a single LAP at 10–11% can cut your effective interest cost by 50–60% and dramatically reduce monthly obligations.

Medical Emergencies:

Large medical procedures (organ transplants, cancer treatment, cardiac surgeries) can cost ₹15–₹50 lakhs. LAP provides rapid access to large amounts at rates far below medical loans or credit facilities.

Working Capital Bridge:

For business owners waiting on large receivables — a LAP provides a working capital bridge at rates well below short-term unsecured business credit.

Important Use-Case Caution

Never use LAP for: Speculation (stock market trading, cryptocurrency), lifestyle upgrades (luxury holidays, high-end consumer purchases), or funding another property purchase as a down payment — situations where the asset funded by the LAP cannot service the debt independently. The risk of losing your pledged property makes frivolous end-use a serious financial danger.

LAP EMI Calculator: Real Scenarios

Scenario 1: Business Owner Expanding Operations

| Detail | Value |

|---|---|

| Property Value | ₹1,20,00,000 |

| LTV (60%) | ₹72,00,000 available |

| Loan Required | ₹50,00,000 |

| Interest Rate | 10.5% (Axis Bank) |

| Tenure | 12 years |

| Monthly EMI | ₹61,332 |

| Total Interest | ₹38,31,904 |

| Monthly Business Revenue Needed (DSCR 1.25) | ₹76,665 |

| Tax Deduction on Interest (business) | Full interest — ₹38.3L over tenure |

Scenario 2: Debt Consolidation — Replacing High-Interest Loans

Existing debt situation:

- Personal Loan: ₹8L at 18% → ₹20,364/month

- Business Loan: ₹12L at 22% → ₹33,924/month

- Credit Card: ₹5L at 42% → ₹17,500/month (interest-only)

- Total: ₹71,788/month, ₹8.59 lakhs/year in interest

After LAP consolidation:

| Detail | Value |

|---|---|

| Total Debt Consolidated | ₹25,00,000 |

| LAP Rate | 10% (residential property, bank) |

| Tenure | 10 years |

| Monthly EMI | ₹33,038 |

| Annual Interest Cost | ₹1,46,256 (Year 1) |

| Monthly Saving | ₹38,750 |

| Annual Saving | ₹4,65,000 |

| 10-Year Total Interest Saving | ₹33,41,100 |

This borrower saves ₹38,750 every single month — over ₹4.65 lakhs per year — simply by consolidating their high-interest debt into a single LAP. The pledged property generates ₹33.41 lakhs in lifetime interest savings.

👉 Model your own LAP scenario with our free Loan Against Property Calculator →

The Complete LAP Application Process

Getting a LAP approved involves more steps than a personal loan but significantly fewer than most borrowers expect when first researching the product:

Stage 1 — Pre-Application (Week 1)

Gather property documents (title deed, sale agreement, property tax receipts, approved building plan, occupancy certificate). Obtain your latest property tax assessment to establish a baseline valuation. Shortlist 3 lenders and compare their stated LAP rates and LTV policies.

Stage 2 — Application Submission (Week 1–2)

Submit application with: Identity proof, income documents (last 3 years ITR for self-employed; 6 months salary slips for salaried), 12 months bank statements, property documents, and existing loan statements.

Stage 3 — Property Valuation (Week 2–3)

Lender appoints an empanelled valuer who visits the property. This is the most variable step — valuation can take 3–10 days depending on the lender and locality. The valuer produces a report establishing fair market value and confirming clear title.

Stage 4 — Legal Verification (Week 2–3)

Lender’s legal team verifies property title chain — ensuring no disputes, existing mortgages, or encumbrances. Clean titles with 15+ years of traceable chain move quickly; older or complex properties take longer.

Stage 5 — Sanction and Disbursement (Week 3–4)

Upon successful valuation and legal verification — loan is sanctioned. Post-signing, lender registers a charge (mortgage) on the property at the sub-registrar’s office. Disbursement follows within 3–5 working days.

Total typical timeline: 3–6 weeks for a well-documented application at a bank; 1–2 weeks at an NBFC (at higher rates).

LAP and Income Tax: What Is Deductible?

Unlike home loans with their structured Section 24(b) and Section 80C deductions — LAP has no standard personal tax deduction on interest. However, two important deductibility situations exist:

| LAP End Use | Interest Deductibility |

|---|---|

| Business purposes | Fully deductible as business expense against business income |

| Purchase/construction of another property (let-out) | Deductible against income from that property (no cap for let-out) |

| Purchase of another property (self-occupied) | Section 24(b) — up to ₹2 lakhs p.a. |

| Education, medical, personal use | No deduction available |

| Debt consolidation | No direct deduction |

The most tax-efficient LAP use case is business expansion — where the entire interest over the loan tenure is deductible against business income, reducing your effective borrowing cost significantly.

A self-employed professional in the 30% bracket taking a ₹40 lakh LAP at 10% for business use pays ₹4,00,000 in interest in Year 1 — saving ₹1,24,800 in income tax from the full deduction. Their effective post-tax interest rate is just 6.8% — one of the cheapest forms of business financing available.

👉 Related Reading: Income Tax Calculator 2025 — Save Maximum Tax Legally → — understanding the full tax landscape around LAP.

👉 Related Reading: How to Save Tax Using Home Loan — Complete Guide → — comparing home loan vs LAP tax benefits.

The Risks of LAP: What You Must Understand Before Pledging

A LAP is a powerful tool — but it comes with one consequence that no personal loan carries: if you default, you lose your property.

This is not a theoretical risk. Banks and NBFCs do initiate recovery proceedings under the SARFAESI Act for defaulted secured loans — and they do sell pledged properties at auction to recover outstanding amounts.

Situations That Put Your Property at Risk

Income shock: Losing your job, a major business downturn, or a health crisis that disrupts income — with a 15-year LAP commitment and a large monthly EMI, an income shock becomes a property risk.

Over-leveraging: Borrowing the maximum LTV on a property that is also your primary residence means a market value decline could technically make you underwater — owing more than the property is worth.

Misusing proceeds: Taking a 15-year LAP for a 1-year need (speculative investment, luxury purchase) and then struggling to service the long-term EMI from a purpose that generated no ongoing return.

Risk Mitigation Strategy

- Maintain DSCR of at least 1.5 when adding the LAP EMI to your existing obligations

- Never pledge your only property if alternatives exist — if possible, pledge a secondary or investment property

- Borrow below your maximum eligibility — the bank’s maximum approved amount is not your optimal borrowing amount

- Maintain an EMI buffer of 3–6 months of EMI in a liquid fund at all times

- Buy term life insurance for the outstanding LAP amount — if you pass away, the property should not become a burden on your family

LAP Across Developing Markets

| Country | Product Name | Typical Rate | LTV | Notable Feature |

|---|---|---|---|---|

| 🇮🇳 India | Loan Against Property | 9–14% | 50–75% | Most developed market; SARFAESI recovery |

| 🇵🇭 Philippines | Real Estate Loan | 10–18% | 60–70% | Requires clear title (TCT/CCT); slower processing |

| 🇳🇬 Nigeria | Mortgage-backed business loan | 18–28% | 40–60% | Limited market; requires Certificate of Occupancy |

| 🇧🇷 Brazil | Crédito com Garantia de Imóvel (CGI) | 10–16% | 60–70% | Growing rapidly; Caixa Econômica leading lender |

| 🇰🇪 Kenya | Property-backed loan | 15–20% | 50–65% | Requires clear title; growing commercial segment |

Brazil’s CGI (Crédito com Garantia de Imóvel) is experiencing explosive growth — with major banks reporting 3–4x volume increases since 2022 as borrowers discover they can access mortgage-secured financing at half the rate of unsecured personal credit. The Brazilian experience closely mirrors India’s LAP market development trajectory.

Frequently Asked Questions

Q: Can I take a loan against a property that already has a home loan running?

A: Yes — this is called a second charge or top-up loan. The existing home loan lender (first charge holder) must consent, or you can approach the same lender for a top-up. The combined outstanding of both loans should not exceed the LTV limit on the property. Most major banks and HFCs offer top-up loans at competitive rates to existing home loan customers.

Q: Can I get LAP against a jointly owned property?

A: Yes — all co-owners must be co-applicants in the LAP application. If one co-owner objects to pledging the property, the LAP cannot proceed. Ensure all co-owners are aligned before starting the application process.

Q: How is the property value determined for LAP purposes?

A: The lender appoints an independent empanelled valuer who physically visits the property and assesses its fair market value based on recent comparable transactions in the area, the property’s age, condition, location, and applicable FSI/development potential. The valuation is typically 10–25% lower than the owner’s optimistic estimate. The lender then applies their LTV ratio to this independently assessed value.

Q: Can I prepay my LAP early without penalty?

A: For floating-rate LAP taken by individuals — RBI prohibits prepayment penalties (same rule as floating-rate home loans). For fixed-rate LAP or company borrowers — a prepayment penalty of 2–4% of outstanding may apply. Always confirm this with your specific lender before taking the loan.

Q: What happens to my LAP if property values fall significantly?

A: If property values fall, the lender may technically be under-secured — but they cannot demand immediate repayment or sell the property as long as you are making regular EMI payments. The lender’s security concern is only activated upon default. As long as you service the EMI regularly, declining property values do not trigger any immediate action from the lender.

Q: Is rented-out commercial property eligible for LAP?

A: Yes — and in some cases, the rental income from the property itself can be considered part of your income for LAP eligibility. A shop generating ₹40,000/month in rental income that is formally documented (registered lease agreement, bank deposits) can significantly boost your eligible loan amount.

Conclusion

Your property is the largest financial asset most people will ever own. And yet, millions of property owners across India and developing markets treat it as entirely illiquid — useful only when sold.

A Loan Against Property changes this equation fundamentally. It activates the wealth locked in your property — at rates 40–60% lower than personal loans, with tenures that make EMIs genuinely manageable, and without requiring you to move, sell, or surrender control of an asset you have spent years building.

Used wisely — for business growth, education, debt consolidation, or genuine emergencies — LAP is one of the most powerful financial tools available to the property-owning middle class.

Used carelessly — as a source of speculative capital or lifestyle spending — it converts your most valuable asset into collateral for a debt that could ultimately take that asset away.

Calculate first. Borrow what your cash flow supports — not the maximum the bank approves. Ensure your end use generates returns or savings that comfortably exceed your LAP cost.

Then activate the financial power that has been sitting in your property all along.

👉 Calculate your exact LAP amount and EMI with our free Loan Against Property Calculator →

👉 Related Reading: Mortgage Calculator — How Much Home Can You Afford? →

👉 Related Reading: Mortgage Refinancing Calculator — When Does It Make Sense? →

👉 Related Reading: Real Estate ROI Calculator — Is Property a Good Investment? →

👉 Related Reading: Income Tax Calculator 2025 — Save Maximum Tax Legally →

👉 Related Reading: Business Loan EMI Calculator — How Much Can Your Business Afford? →

👉 Related Reading: How to Use a Financial Calculator to Escape the Debt Trap →

👉 Related Reading: How Banks Calculate Your Home Loan Eligibility →