You received your annual bonus — ₹50,000 sitting in your savings account earning 3.5% interest.

Your home loan outstanding balance is ₹35 lakhs at 8.5% — still 16 years remaining.

The question your financial advisor, your parents, and your gut are all asking simultaneously: should you put that ₹50,000 into your loan?

The loan prepayment calculator answers this with ruthless mathematical clarity — showing you exactly how many months disappear from your loan tenure, precisely how many lakhs of interest you save, and how that same money performs if invested instead.

For most home loan borrowers in the early-to-mid phase of their repayment journey, the answer will surprise them. A single ₹50,000 prepayment can save ₹3–₹4 lakhs in total interest and close the loan 6–18 months early. Not because of magic — because of the compound interest mathematics working powerfully in the lender’s favour and now being redirected back toward you.

Here is everything you need to know about loan prepayment — with precise calculations, the timing truth nobody tells you, and the strategic framework that maximises every extra rupee you put toward your loan.

👉 Calculate your exact prepayment savings in seconds with our free Loan Prepayment Calculator →

How Loan Prepayment Works: The Mathematics

Every loan EMI is split between interest on the outstanding balance and principal reduction. In the early years of any loan — especially home loans — this split is heavily skewed toward interest:

Standard Home Loan Example:

Loan: ₹35,00,000 at 8.5% for 20 years

Monthly EMI: ₹30,430

Year 1 — EMI Breakdown (Month 1):

Interest Component: ₹24,792 (81.4% of EMI)

Principal Component: ₹5,638 (18.6% of EMI)

Year 10 — EMI Breakdown (Month 121):

Interest Component: ₹19,104 (62.8% of EMI)

Principal Component: ₹11,326 (37.2% of EMI)

Year 18 — EMI Breakdown (Month 216):

Interest Component: ₹5,834 (19.2% of EMI)

Principal Component: ₹24,596 (80.8% of EMI)This amortisation structure — front-loaded with interest — is why prepayment is so extraordinarily powerful in the early years. Every rupee you prepay in Year 1 reduces the principal that generates interest for all 19 remaining years. Every rupee you prepay in Year 18 only saves the small interest remaining on a nearly cleared balance.

When you make a prepayment:

The entire prepayment amount goes directly to reducing the outstanding principal — not split between interest and principal like a regular EMI. This principal reduction then reduces the interest calculated on all future months.

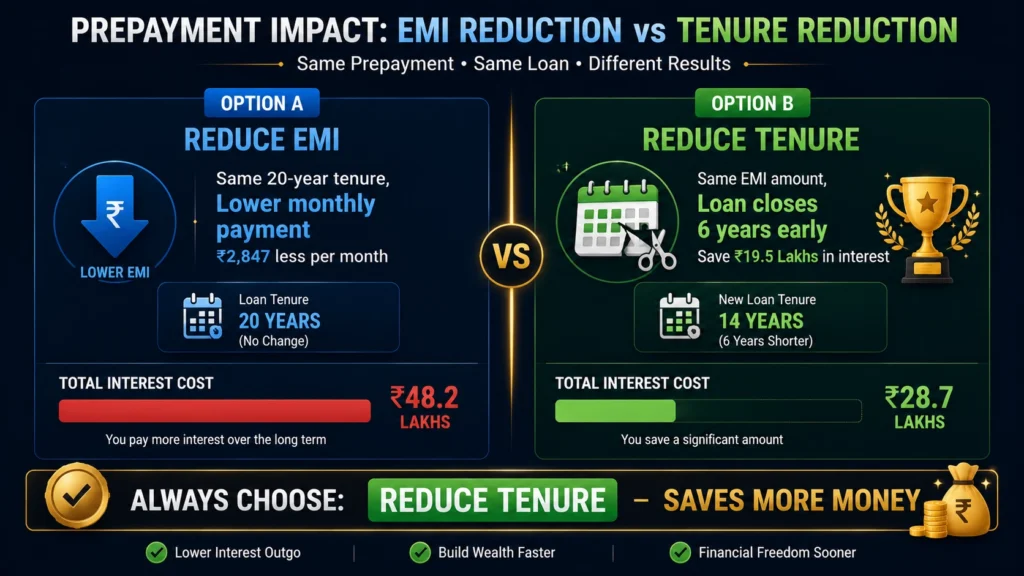

The Two Prepayment Choices: Which Maximises Your Savings?

When you make a prepayment, your lender typically gives you a choice. This is one of the most important decisions in home loan management:

Option A: Reduce Your Monthly EMI

Keep the same loan tenure. Your monthly EMI drops to reflect the reduced outstanding balance.

Option B: Reduce Your Loan Tenure

Keep the same monthly EMI. The loan closes earlier than the original schedule.

The Mathematical Verdict

| Prepayment: ₹3,00,000 on ₹35L Loan (8.5%, 16 years remaining) | Option A: Reduce EMI | Option B: Reduce Tenure |

|---|---|---|

| New EMI | ₹27,694 (reduced from ₹30,430) | ₹30,430 (unchanged) |

| Tenure | 16 years (unchanged) | 13 years 2 months |

| Months Saved | 0 | 34 months |

| Total Interest Remaining | ₹29,62,000 | ₹22,17,000 |

| Interest Saved vs No Prepayment | ₹4,51,000 | ₹11,96,000 |

| Winner | Option B by ₹7,45,000 |

Option B saves ₹7.45 lakhs MORE than Option A on the same ₹3 lakh prepayment — simply by maintaining the same monthly payment and letting the savings accumulate in reduced interest over a shorter tenure.

The rule is universal: Unless your monthly cash flow is genuinely strained and you need the EMI relief — always choose tenure reduction over EMI reduction. The total interest saved is dramatically larger and you become debt-free years sooner.

Prepayment Savings Calculator: Real Scenarios

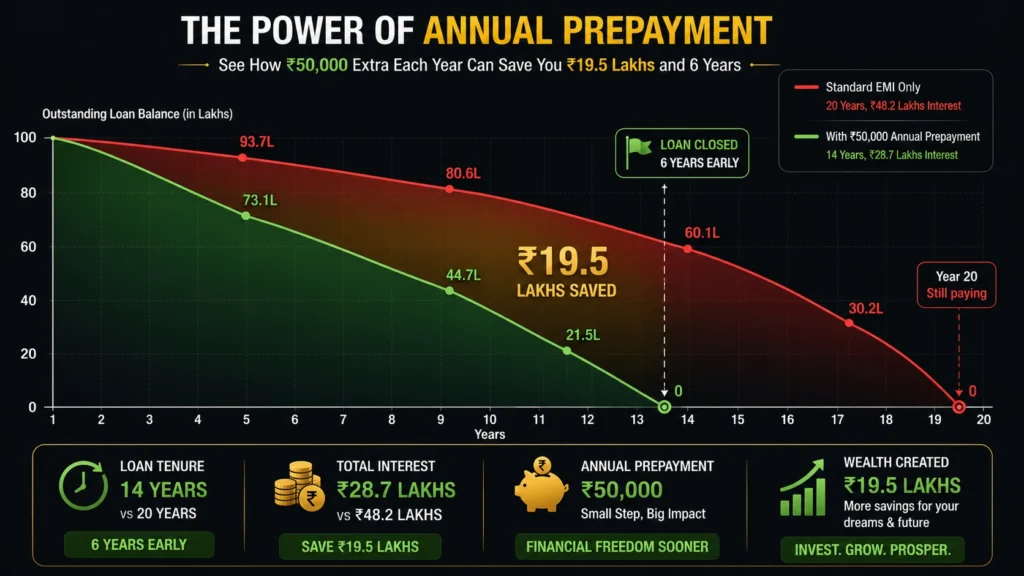

Scenario 1: Home Loan — Annual ₹50,000 Bonus Prepayment

| Detail | Without Prepayment | With ₹50,000 Annual Prepayment |

|---|---|---|

| Loan Amount | ₹35,00,000 | ₹35,00,000 |

| Interest Rate | 8.5% | 8.5% |

| Original Tenure | 20 years | 20 years |

| Monthly EMI | ₹30,430 | ₹30,430 (unchanged) |

| Actual Loan Closure | Month 240 (Year 20) | Month 168 (Year 14) |

| Months Saved | — | 72 months (6 years) |

| Total Interest Paid | ₹37,83,200 | ₹23,14,600 |

| Total Interest Saved | — | ₹14,68,600 |

A disciplined ₹50,000 annual prepayment — just one bonus each year — saves ₹14.68 lakhs in interest and closes the loan 6 full years early. The total prepayment made is ₹7,00,000 (14 prepayments × ₹50,000) generating ₹14.68 lakhs in savings — a 2.1x return on every prepaid rupee in the form of interest not paid.

Scenario 2: Personal Loan — ₹20,000 One-Time Prepayment

| Detail | Without Prepayment | With ₹20,000 Prepayment (Month 6) |

|---|---|---|

| Loan Amount | ₹5,00,000 | ₹5,00,000 |

| Interest Rate | 15% | 15% |

| Original Tenure | 48 months | 48 months |

| Monthly EMI | ₹13,916 | ₹13,916 |

| Outstanding at Month 6 | ₹4,28,000 | ₹4,08,000 |

| Months Saved | — | 4 months |

| Total Interest Saved | — | ₹55,664 |

Even a single ₹20,000 prepayment on a ₹5 lakh personal loan at Month 6 saves ₹55,664 in interest — a 2.78x return on the prepaid amount.

Scenario 3: Car Loan — ₹1 Lakh Prepayment (Year 2 vs Year 4)

This scenario demonstrates the critical importance of timing your prepayment early:

| Prepayment: ₹1,00,000 on ₹6L Car Loan (9%, 5 Years) | Year 2 Prepayment | Year 4 Prepayment |

|---|---|---|

| Outstanding Balance at Prepayment | ₹4,52,000 | ₹2,18,000 |

| Months Remaining at Prepayment | 36 months | 12 months |

| Interest Saved | ₹32,640 | ₹8,730 |

| Months Loan Shortened By | 7 months | 3 months |

| Return on ₹1L Prepayment | 32.6% | 8.7% |

The same ₹1 lakh prepayment generates 3.7x more interest savings when made in Year 2 versus Year 4 — purely because of the additional time for the reduced principal to avoid generating interest.

👉 Model your exact prepayment scenario with our free Loan Prepayment Calculator →

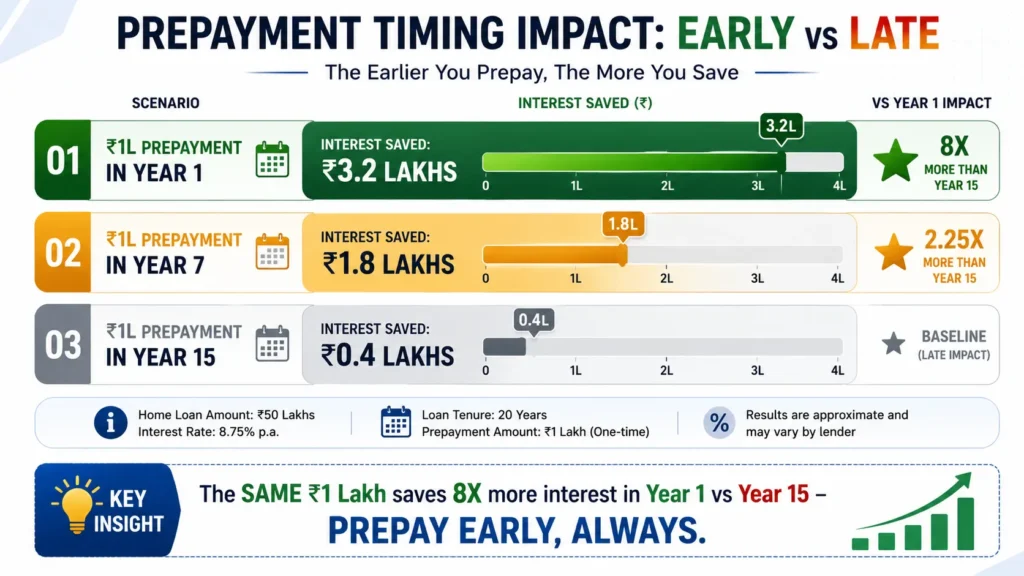

The Timing Truth: Why Early Prepayment Is Exponentially More Valuable

This is the single most important concept in loan prepayment strategy — and the one most borrowers never quantify:

₹1,00,000 Prepayment on ₹35L Home Loan (8.5%, 20 Years):

Made in Year 1:

Interest Saved: ₹3,18,400

Months Shortened: 11 months

Made in Year 5:

Interest Saved: ₹2,14,200

Months Shortened: 8 months

Made in Year 10:

Interest Saved: ₹1,26,800

Months Shortened: 6 months

Made in Year 15:

Interest Saved: ₹42,600

Months Shortened: 2 months

Made in Year 18:

Interest Saved: ₹9,200

Months Shortened: 0.4 monthsThe same ₹1 lakh prepayment generates 34x more interest saving in Year 1 than in Year 18. Not 34% more – 34 times more.

This mathematical reality has a profound strategic implication: the most valuable use of any windfall, bonus, or surplus in the early years of a home loan is prepayment. In the later years, investing the same amount in equity may generate better returns than the diminishing prepayment benefit.

The Prepayment vs Investment Dilemma: A Framework

The most common question in personal finance for home loan borrowers: “Should I prepay my loan or invest the money in equity?”

The answer depends on four variables – your loan interest rate, expected investment return, remaining tenure, and your tax situation:

| Condition | Prepay or Invest? | Reason |

|---|---|---|

| Loan rate above 9%, early tenure | Prepay | Guaranteed 9%+ return; hard to beat risk-adjusted |

| Loan rate below 8%, long tenure | Invest in equity | 12% equity return likely exceeds 8% guaranteed saving |

| Tax bracket 30%, home loan interest deductible | Invest (marginally) | Effective loan cost at 30% = 5.95% (8.5% × 70%) |

| High-interest debt (CC, personal loan) outstanding | Prepay high-interest debt first | Always eliminate 18%+ debt before any investment |

| Less than 7 years remaining | Invest | Small balance = small prepayment benefit |

| No emergency fund yet | Build emergency fund first | Liquidity safety before loan optimisation |

The nuanced framework for home loan specifically:

After the Section 24(b) tax deduction — a 30% bracket taxpayer’s effective home loan interest rate is:

Effective Rate = Nominal Rate × (1 − Tax Rate)

= 8.5% × (1 − 0.30) = 5.95%At 5.95% effective cost — a well-chosen equity SIP averaging 12% annually clearly outperforms prepayment mathematically. However, this framework assumes disciplined investment of every rupee not prepaid — which requires strong investment discipline that not everyone maintains.

The practical recommendation:

- If you have strong investment discipline → Invest above 8% effective loan rate

- If you tend to spend rather than invest → Prepay always — it is forced savings at a guaranteed rate

- Best of both → Split the bonus (50% prepay, 50% invest) — eliminates the decision paralysis

The Amortisation Schedule: Your Prepayment Roadmap

Every home loan borrower should request and study their complete amortisation schedule — the month-by-month breakdown of every EMI between interest and principal for the full tenure. This document makes the prepayment benefit visible in a way that transforms motivation.

Here is a partial amortisation schedule for a ₹35 lakh loan at 8.5% for 20 years:

| Month | EMI | Interest Paid | Principal Paid | Outstanding Balance |

|---|---|---|---|---|

| 1 | ₹30,430 | ₹24,792 | ₹5,638 | ₹34,94,362 |

| 12 | ₹30,430 | ₹24,393 | ₹6,037 | ₹34,28,000 |

| 24 | ₹30,430 | ₹23,968 | ₹6,462 | ₹33,49,000 |

| 60 | ₹30,430 | ₹22,829 | ₹7,601 | ₹31,65,000 |

| 120 | ₹30,430 | ₹19,843 | ₹10,587 | ₹27,53,000 |

| 180 | ₹30,430 | ₹14,822 | ₹15,608 | ₹20,66,000 |

| 200 | ₹30,430 | ₹9,640 | ₹20,790 | ₹12,81,000 |

| 240 | ₹30,430 | ₹214 | ₹30,216 | ₹0 |

Looking at this schedule — the first 5 years (60 months) pay ₹13.70 lakhs in interest while reducing principal by only ₹3.35 lakhs. Every prepayment made in these early months directly attacks this front-loaded interest burden.

Prepayment Rules by Loan Type: What You Need to Know

Not all loans treat prepayment equally. Understanding the rules — and costs — before prepaying is essential:

| Loan Type | Prepayment Penalty | RBI Rule | Notes |

|---|---|---|---|

| Floating Rate Home Loan (Individual) | NIL | RBI prohibits any penalty | Most common home loan type — fully flexible |

| Fixed Rate Home Loan (Individual) | 2–4% of prepaid amount | Allowed | Calculate penalty vs interest saving before prepaying |

| Personal Loan (Floating) | NIL | RBI prohibits | Check if your loan is truly floating |

| Personal Loan (Fixed — most are) | 2–5% of prepaid amount | Allowed | Penalty often erodes prepayment benefit |

| Car Loan (Fixed) | 2–6% of prepaid amount | Allowed | Verify terms before prepaying |

| Education Loan | Usually NIL | Encouraged | Banks support early closure |

| Business Loan (Individual) | NIL (floating) | RBI prohibits | Fixed rate business loans may carry penalty |

| Gold Loan | Usually NIL | Generally free | Confirm with specific lender |

The floating rate advantage is enormously valuable: If your home loan is on a floating rate — which 90%+ of Indian home loans are — you can prepay any amount at any time with absolutely zero penalty. This flexibility has enormous financial value that is often unappreciated.

👉 Related Reading: Fixed vs Floating Rate Mortgage — 10-Year Cost Comparison → — understanding why floating rate loans provide superior prepayment flexibility.

Lump Sum vs Regular Small Prepayments: Which Works Better?

Many borrowers wait to accumulate a large prepayment amount. Is this the right strategy?

Comparison: ₹1,20,000 Total Prepayment

Option A: One Lump Sum of ₹1,20,000 in Month 13

Interest Saved: ₹3,69,840

Months Shortened: 13

Option B: ₹10,000 Monthly Prepayment for 12 Months (starting Month 2)

Interest Saved: ₹4,12,200

Months Shortened: 15

Difference: Monthly prepayments save ₹42,360 MORE than lump sum

at year-end — purely because each ₹10,000 starts saving earlier.Monthly small prepayments — even ₹2,000–₹5,000 above your standard EMI — consistently outperform equivalent annual lump sums because each additional payment starts reducing interest accrual immediately.

The practical approach: Set up a standing instruction at your bank for ₹3,000–₹10,000 additional EMI payment every month. This removes the decision friction of “should I prepay now?” and creates automatic, consistent debt reduction.

The Step-by-Step Prepayment Process

Step 1 — Check Your Loan Terms

Confirm whether your loan is floating rate (typically no penalty) or fixed rate (verify penalty percentage). Log in to your lender’s net banking portal or call customer service.

Step 2 — Calculate the Benefit First

Use our Loan Prepayment Calculator to enter your outstanding balance, current rate, remaining tenure, and prepayment amount. See exactly how many months you save and how much interest you preserve.

Step 3 — Choose Tenure Reduction (Not EMI Reduction)

Explicitly inform your lender in writing or through their portal: “I wish to maintain the same EMI and reduce the outstanding tenure.” This maximises your interest saving.

Step 4 — Make the Payment

Most banks accept prepayment via: net banking transfer to the loan account, NEFT/IMPS with the loan account number, cheque at the branch, or their dedicated prepayment portal.

Step 5 — Obtain Updated Schedule

After prepayment, request an updated amortisation schedule from your lender. Verify the new tenure end date reflects the prepayment correctly. Errors in prepayment crediting — while rare — do occur and must be caught immediately.

Step 6 — Track and Repeat

Calendar-mark your next prepayment date. Consistent annual prepayments — aligned with bonus cycles, tax refunds, or salary increments — build a systematic debt reduction plan.

Prepayment for Different Loan Types: Priority Order

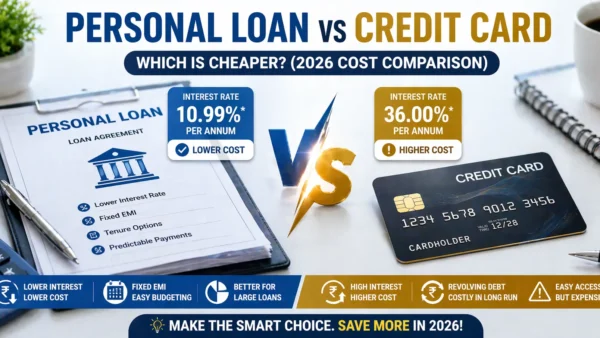

If you have multiple loans outstanding and limited surplus for prepayment — always attack in this order:

| Priority | Loan Type | Reason |

|---|---|---|

| 1st | Credit Card revolving balance (36–42%) | Highest rate — guaranteed 36%+ saving |

| 2nd | App/digital loans (24–60%) | Extremely high rates — clear immediately |

| 3rd | Personal loans (12–22%) | High rate with minimal tax benefit |

| 4th | Gold loans (12–28%) | Frees pledged jewellery; often high rate |

| 5th | Education loan (8–14%) | Section 80E reduces effective cost |

| 6th | Car loan (9–11%) | Moderate rate; fixed asset depreciating |

| 7th | Home loan (8.5–10%) | Lowest rate; Section 24b reduces further |

The counterintuitive bottom position of home loan: Despite being the largest loan, the home loan often has the lowest effective rate after tax deductions — particularly in the old tax regime where Section 24(b) reduces the effective rate to 5.95–7% for taxpayers in the 20–30% bracket. All higher-rate debts should be cleared first.

Prepayment Across Developing Markets

| Country | Prepayment Rules | Typical Penalty | Best Practice |

|---|---|---|---|

| 🇮🇳 India | RBI: No penalty on floating rate individual home loans | Nil (floating); 2–4% (fixed) | Always take floating rate for flexibility |

| 🇵🇭 Philippines | Varies by lender — BSP has no blanket rule | 1–3% common | Verify at loan origination |

| 🇳🇬 Nigeria | Generally penalised — 1–3% | 1–3% | Negotiate penalty waiver at origination |

| 🇧🇷 Brazil | Law prohibits excessive prepayment penalties; standardised | Typically 0.5–1% | Portability law helps — switch if needed |

| 🇰🇪 Kenya | Varies widely — limited consumer protection | 1–5% possible | Negotiate explicitly at origination |

India’s floating rate prepayment policy is one of the most consumer-friendly in any developing market — the complete absence of prepayment penalties gives Indian home loan borrowers a financial flexibility that borrowers in most other markets do not enjoy. This advantage should be actively exploited through regular prepayments.

Frequently Asked Questions

Q: Is there a minimum prepayment amount for home loans in India?

A: Most banks have a minimum prepayment amount — typically equivalent to one or two standard EMIs (₹15,000–₹60,000 depending on loan size). Some banks and NBFCs accept prepayments as low as ₹5,000. Check your specific lender’s policy — some digital lenders allow very small regular prepayments through their apps with no minimum restriction.

Q: Should I prepay my home loan or invest in mutual funds?

A: This depends primarily on your effective home loan interest rate after tax deductions. If you are in the 30% tax bracket with Section 24(b) — your effective home loan rate is approximately 5.95–7.35% (after deduction). A well-chosen equity SIP targeting 12% returns likely beats this. If your loan has no tax deduction benefit (new tax regime), or if you lack investment discipline, prepayment provides a guaranteed saving. Many advisors recommend a 50-50 split — prepay and invest simultaneously — as the optimal behavioural solution.

Q: How do I make a prepayment on my SBI/HDFC/ICICI home loan?

A: Most major banks allow prepayment through net banking — look for “Loan Prepayment” or “Part Payment” option under your loan account. Alternatively, visit the branch with a written prepayment request and the prepayment amount by DD or cheque payable to the lender. Always explicitly state you want “tenure reduction with EMI unchanged” in your request. Obtain an acknowledgement and updated schedule post-payment.

Q: Will prepayment affect my home loan tax benefit?

A: Yes — as you prepay and reduce your outstanding balance, the annual interest component of your EMI reduces over time. This means the Section 24(b) deduction (up to ₹2 lakhs on interest) may reduce in later years as interest falls below ₹2 lakhs. This is a benefit reducing another benefit — the interest savings almost always outweigh the marginal tax deduction loss. Always model the net benefit considering both.

Q: What is the difference between part payment and foreclosure?

A: Part payment (partial prepayment) is paying an additional amount over your regular EMI to reduce the outstanding balance — while the loan continues. Foreclosure is paying the entire outstanding balance in a single payment, completely closing the loan. Both have similar rules — no penalty for floating rate individual home loans. Foreclosure requires obtaining a foreclosure statement from the lender showing the exact payoff amount on a specific date (interest accrues daily on outstanding balance).

Q: Does prepayment improve my credit score?

A: Prepayment itself does not directly improve your CIBIL score. However, faster loan closure (from tenure reduction) results in a “closed/settled” loan account appearing on your credit report earlier — which is generally positive for your credit history. The reduced outstanding balance also improves your credit utilisation ratio over time. The most important credit impact of prepayment is that you exit the loan’s repayment risk period sooner — eliminating the possibility of future defaults on that loan.

Conclusion

The loan prepayment calculator reveals one of the most powerful — and most underused — financial levers available to any borrower.

A single ₹50,000 prepayment in Year 3 of a home loan saves ₹3–₹4 lakhs in interest. Done annually over 7 years, that same discipline saves over ₹14 lakhs and closes your loan 6 years early. The mathematics are not complicated. The discipline is simply knowing the numbers clearly enough to act on them.

Three actions worth taking today:

Action 1: Run our prepayment calculator with your current outstanding balance. See your exact interest saving from a single prepayment this month.

Action 2: Check whether your loan is on a floating rate — if yes, you have complete, penalty-free prepayment flexibility right now.

Action 3: Set up a standing instruction for even ₹2,000–₹5,000 extra above your standard EMI. The automation removes decision friction and makes consistent debt reduction effortless.

The interest you do not pay is the most guaranteed return available in personal finance. Use the calculator. Make the prepayment. Keep the money.

👉 Calculate your exact prepayment savings with our free Loan Prepayment Calculator →

👉 Related Reading: Fixed vs Floating Rate Mortgage — 10-Year Cost Comparison →

👉 Related Reading: How to Reduce Your Home Loan EMI by 30% →

👉 Related Reading: Mortgage Refinancing Calculator — When Does It Make Sense? →

👉 Related Reading: EMI vs Lump Sum Repayment — Which Saves More Money? →

👉 Related Reading: Best Loan Tenure — Short vs Long EMI Calculator →

👉 Related Reading: Tax-Saving Investment Calculator — 5 Best Options →

👉 Related Reading: How to Use a Financial Calculator to Escape the Debt Trap →