You applied for a home loan. Your income is good, your credit score is decent, and the property is perfectly priced.

The bank said no.

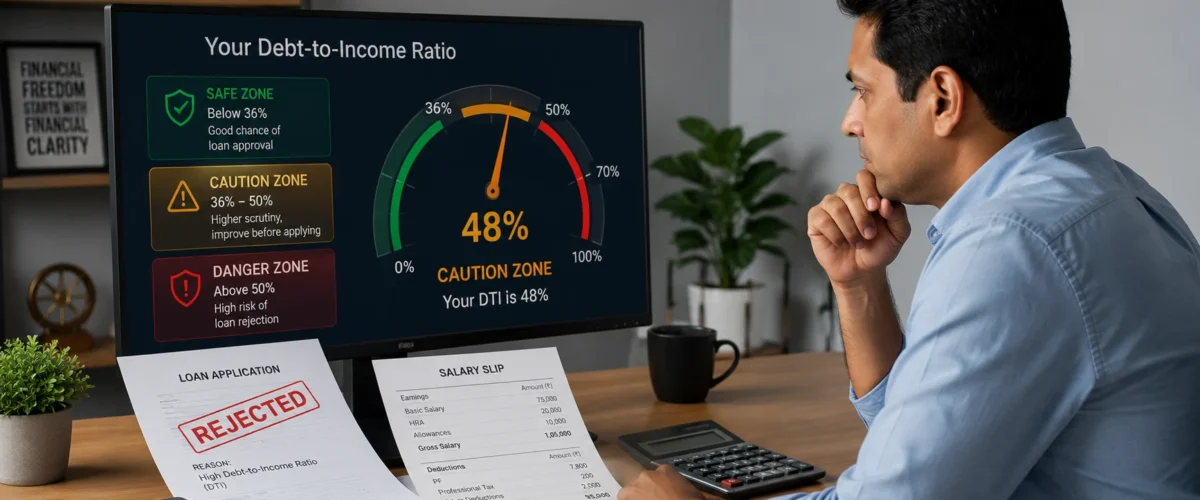

Or worse — the bank said yes, but the EMI is consuming 52% of your monthly take-home, leaving you perpetually anxious about the next salary credit.

In both scenarios, the answer to understanding what went wrong — or what is going wrong — is a single number: your Debt-to-Income Ratio (DTI).

This one ratio determines more about your financial health, your loan eligibility, and your long-term wealth-building capacity than almost any other metric. It is what banks calculate before approving or rejecting every loan application. And yet most borrowers have never heard of it — let alone calculated their own.

Here is everything you need to know about DTI — including how to calculate it precisely, what number you should be targeting, and exactly how to improve it if you are in the danger zone.

👉 Calculate your DTI ratio instantly with our free Debt-to-Income Ratio Calculator →

What Is the Debt-to-Income Ratio?

The Debt-to-Income (DTI) ratio — called FOIR (Fixed Obligation to Income Ratio) in India — measures the percentage of your gross monthly income that goes toward servicing all debt obligations.

DTI Formula:

DTI = (Total Monthly Debt Obligations ÷ Gross Monthly Income) × 100

Where Total Monthly Debt Obligations includes:

- All existing loan EMIs (home loan, car loan, personal loan, education loan)

- Minimum credit card due payments

- Any proposed new loan EMI you are applying for

Example:

Home Loan EMI: ₹18,000

Car Loan EMI: ₹8,500

Personal Loan EMI: ₹5,000

Credit Card Minimum Due: ₹2,000

New Loan EMI Requested: ₹12,000

Total Monthly Obligations: ₹45,500

Gross Monthly Income: ₹1,00,000

DTI = (₹45,500 ÷ ₹1,00,000) × 100 = 45.5%This borrower is in the high-risk zone — 45.5% of every rupee earned is pre-committed to debt before a single rupee goes to food, rent, savings, or investment.

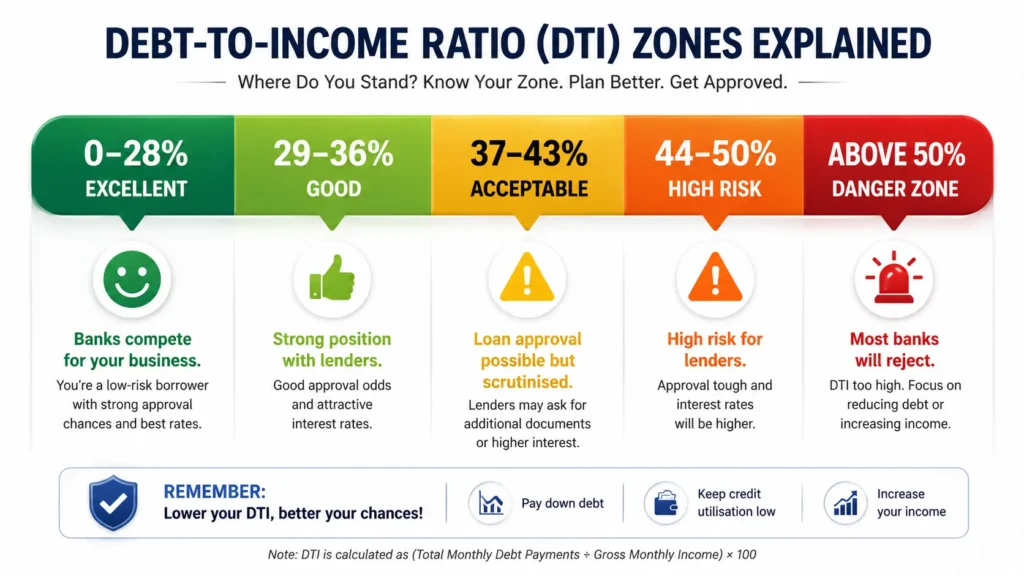

The DTI Safety Zones: Where Do You Stand?

| DTI Range | Classification | What It Means | Bank Response |

|---|---|---|---|

| Below 28% | Excellent | Healthy — significant capacity for new debt | Best rates; multiple lenders compete |

| 28–36% | Good | Comfortable — new borrowing manageable | Strong approval likelihood; good rates |

| 37–43% | Acceptable | Caution zone — some capacity remaining | Approval possible; scrutinised more carefully |

| 44–50% | High Risk | Stretched — very limited new debt capacity | Many banks will decline or reduce loan amount |

| Above 50% | Danger Zone | Over-leveraged — income cannot safely support more debt | Most banks reject; debt trap risk is real |

The 36% threshold is the globally accepted benchmark for healthy debt-to-income — used by financial institutions from India’s RBI-regulated banks to mortgage lenders in the United States, Europe, and across developing markets.

Above 50% — you are in territory where a single income disruption (job loss, medical emergency, business downturn) can trigger a debt spiral. The monthly obligations leave insufficient buffer for savings, emergencies, or unexpected costs.

DTI vs FOIR: Understanding the Indian Context

In India, banks do not use the term DTI — they use FOIR (Fixed Obligation to Income Ratio). While conceptually identical, FOIR is applied slightly differently:

| Aspect | DTI (International) | FOIR (India) |

|---|---|---|

| Definition | Debt payments ÷ Gross income | Fixed obligations ÷ Gross income |

| What is included | All debt EMIs + minimum credit card dues | All EMIs + credit card minimum dues + any fixed rental obligations |

| Maximum threshold used by most banks | 36–43% | 40–55% (varies by lender) |

| Used primarily for | Mortgage underwriting globally | All loan types in India |

| Impact of credit score | High score allows higher DTI threshold | High score allows higher FOIR threshold |

The key Indian nuance: Different lender types apply different FOIR limits:

| Lender Type | Maximum FOIR Applied | Impact |

|---|---|---|

| PSU Banks (SBI, PNB, BOB) | 40–50% | Conservative — lower eligible loan amount |

| Private Banks (HDFC, ICICI, Axis) | 50–55% | Moderate — higher eligible amount |

| HFCs (LIC HFL, PNB Housing) | 55–60% | Flexible — highest eligible amount |

| NBFCs (Bajaj, IIFL) | 55–65% | Most flexible — often higher rates |

The practical implication: If a PSU bank rejects your loan citing high FOIR — an HFC or NBFC may approve the same amount using their higher threshold. However, the higher threshold comes with higher rates — always model the total interest cost before choosing a more flexible lender.

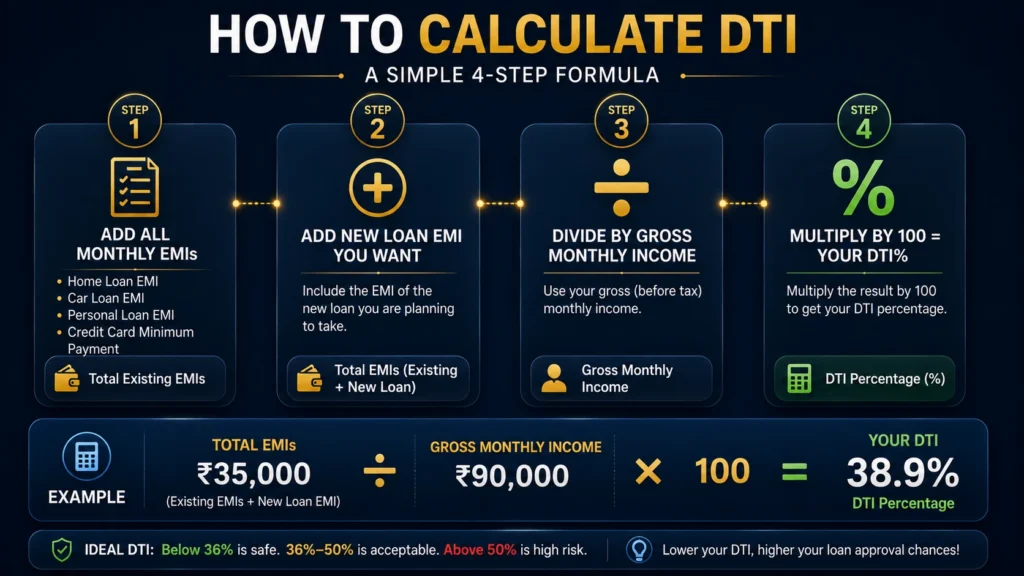

How to Calculate Your DTI: Step-by-Step

Step 1 — List Every Monthly Debt Obligation

Be exhaustive and honest. Include everything:

| Debt Type | Monthly Amount |

|---|---|

| Home Loan EMI | ₹ |

| Car Loan EMI | ₹ |

| Personal Loan EMI | ₹ |

| Education Loan EMI | ₹ |

| Business Loan EMI | ₹ |

| Credit Card 1 — Minimum Due | ₹ |

| Credit Card 2 — Minimum Due | ₹ |

| App/Digital Loan EMI | ₹ |

| Buy Now Pay Later Installments | ₹ |

| Family Loan (if structured repayment) | ₹ |

| TOTAL EXISTING MONTHLY OBLIGATIONS | ₹ |

Step 2 — Add the Proposed New Loan EMI

If you are calculating DTI to check whether you can take a new loan — add the estimated EMI of that new loan to your total obligations. Our calculator can compute the EMI for any loan amount, rate, and tenure.

Step 3 — Identify Your Gross Monthly Income

Use gross income — before any tax deductions — for the DTI calculation. This is your CTC divided by 12 (for salaried employees), or average monthly income from your last 2 years’ ITR (for self-employed).

Gross Monthly Income Examples:

₹8 LPA CTC → ₹66,667/month gross

₹12 LPA CTC → ₹1,00,000/month gross

₹18 LPA CTC → ₹1,50,000/month gross

Business profit ₹15L/year → ₹1,25,000/month grossStep 4 — Calculate

DTI = (Total Monthly Obligations ÷ Gross Monthly Income) × 100

If DTI < 36%: You are in good financial health

If DTI 36–50%: Exercise caution before new borrowing

If DTI > 50%: Prioritise debt reduction before any new loans👉 Let our calculator do all four steps automatically — enter your income and debts in our free DTI Calculator →

How DTI Affects Your Loan Eligibility: The Exact Calculation

Banks use your DTI/FOIR to determine the maximum EMI they will approve — which directly determines the maximum loan amount you qualify for:

Bank's Calculation:

Maximum Approved EMI = Gross Income × FOIR Limit

Less: All Existing EMIs

= Available EMI for New Loan

Then:

Maximum Loan Amount = Available EMI × Loan Multiplier

Example (50% FOIR limit, 8.5%, 20yr):

Gross Income: ₹1,00,000

Maximum EMI (50%): ₹50,000

Existing EMIs: ₹20,000

Available for New Home Loan: ₹30,000

Loan Multiplier (8.5%, 20yr): 172

Maximum Eligible Home Loan: ₹30,000 × 172 = ₹51,60,000DTI Impact Table: How Each ₹5,000 of Existing EMI Reduces Your Home Loan Eligibility

| Existing Monthly EMIs | Available for Home Loan (50% FOIR, ₹1L income) | Maximum Home Loan (8.5%, 20yr) |

|---|---|---|

| ₹0 | ₹50,000 | ₹86,00,000 |

| ₹5,000 | ₹45,000 | ₹77,40,000 |

| ₹10,000 | ₹40,000 | ₹68,80,000 |

| ₹15,000 | ₹35,000 | ₹60,20,000 |

| ₹20,000 | ₹30,000 | ₹51,60,000 |

| ₹25,000 | ₹25,000 | ₹43,00,000 |

| ₹30,000 | ₹20,000 | ₹34,40,000 |

| ₹40,000 | ₹10,000 | ₹17,20,000 |

| ₹50,000 | ₹0 | Not eligible |

Every ₹5,000 of existing monthly EMI costs you approximately ₹8,60,000 in home loan eligibility on a ₹1 lakh gross income. This is the clearest mathematical argument for clearing small debts before applying for a home loan.

👉 Related Reading: How Banks Calculate Your Home Loan Eligibility → — the complete inside guide to lender eligibility formulas.

👉 Related Reading: Mortgage Calculator — How Much Home Can You Afford? → — using DTI correctly in home affordability planning.

Country-Specific DTI Benchmarks: Global Comparison

Debt-to-income thresholds differ across developing markets based on lending culture, regulatory framework, and typical household financial structure:

| Country | Recommended DTI | Maximum Bank FOIR/DTI | Regulatory Body | Key Note |

|---|---|---|---|---|

| 🇮🇳 India | Below 40% | 40–60% (varies) | RBI | FOIR-based; includes all fixed obligations |

| 🇵🇭 Philippines | Below 35% | 30–40% | Bangko Sentral | Conservative by regulation; housing DBR capped |

| 🇳🇬 Nigeria | Below 33% | 33% | CBN guideline | Debt Burden Ratio (DBR) strictly enforced |

| 🇧🇷 Brazil | Below 30% | 30% (legal cap) | Banco Central | Renda Comprometida legally capped at 30% |

| 🇰🇪 Kenya | Below 40% | 40–50% | CBK guideline | Net income methodology; NHIF/NSSF excluded |

| 🇵🇰 Pakistan | Below 40% | 40% guideline | SBP | Net income basis after statutory deductions |

Brazil’s 30% legal cap is the strictest in the world — no lender can approve a loan where the total monthly obligations exceed 30% of gross income. This explains why Brazilian household debt levels are relatively contained compared to other large emerging markets, despite extremely high consumer interest rates.

Nigeria’s 33% DBR is also strictly applied — reflecting CBN’s conservative approach to managing household debt levels in an economy with high inflation and currency volatility.

5 Proven Ways to Improve Your DTI

Method 1: Clear Small High-Interest Debts First

The most impactful single action: identify your smallest outstanding loan balances and clear them completely before applying for any new major loan.

Example:

Personal Loan Outstanding: ₹1,20,000 (remaining 6 months, ₹21,000 EMI)

Credit Card Balance: ₹80,000 (minimum due ₹2,400/month)

Paying off both: ₹2,00,000 cash outlay

EMI reduction: ₹23,400/month

Home Loan Eligibility Increase: ₹23,400 × 172 = ₹40,24,800

You spend ₹2 lakhs and unlock ₹40+ lakhs in home loan eligibility.

This is a 20:1 return on capital from a DTI improvement perspective.Method 2: Increase Your Documented Income

Higher gross income directly reduces your DTI ratio on the same debt level. Strategies to legitimately increase documented income before a loan application:

- Negotiate a salary revision — even a 10% hike meaningfully improves FOIR

- Declare all income sources — rental income (with registered agreement), freelance earnings (with ITR), interest income

- Add a co-applicant — a working spouse or earning family member’s income is fully considered in joint applications

- Ensure your last ITR reflects full income — under-declaration for tax purposes directly reduces loan eligibility

Method 3: Avoid Any New EMI Commitments for 6 Months Before Applying

Every new EMI — car loan, consumer electronics financing, phone EMI — reduces your available FOIR capacity. In the 6 months before a major loan application: pay cash or delay all purchases that would create new EMI obligations.

Impact of a ₹50,000 phone on EMI (12 months, 0% but still counted):

Monthly EMI: ₹4,167

Home Loan Eligibility Reduction: ₹4,167 × 172 = ₹7,16,724

A ₹50,000 phone purchase costs you ₹7.16 lakhs in home loan eligibility.Method 4: Choose Longer Tenure on Existing Loans

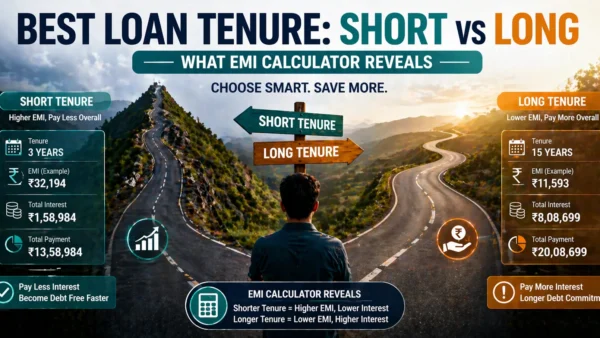

If you have existing loans with high monthly EMIs — contact your lender and request a tenure extension (loan restructuring). Stretching an existing personal loan from 2 remaining years to 4 years reduces its monthly EMI, improving your FOIR for the new loan application.

Caveat: This increases total interest paid on the existing loan. Calculate the trade-off — is the new loan eligibility gain worth the additional interest cost on the restructured loan?

Method 5: Refinance High-Rate Loans at Lower Rates

A high-interest personal loan at 20% carries a larger EMI than the same outstanding balance at 13%. Refinancing existing high-rate loans to lower rates directly reduces your monthly obligations and improves DTI.

Outstanding Personal Loan: ₹3,00,000 at 20%, 24 remaining months

Current EMI: ₹15,254

Refinanced at 13%, 24 months:

New EMI: ₹14,266

Monthly DTI improvement: ₹988/month

Home Loan Eligibility Gain: ₹988 × 172 = ₹1,69,936

A quick refinance unlocks ₹1.7 lakhs in additional home loan eligibility

at zero additional cash outlay.👉 Related Reading: Mortgage Refinancing Calculator — When Does It Make Sense? → — leveraging refinancing to improve DTI and reduce total interest.

The Lifestyle DTI: Beyond Loan Eligibility

Financial health goes beyond what banks use DTI for. Your personal DTI — including commitments banks do not count but which consume your income — is equally important for genuine financial wellbeing:

| Commitment | Banks Count It? | You Should Count It |

|---|---|---|

| Loan EMIs | ✅ Yes | ✅ Yes |

| Credit card minimum due | ✅ Yes | ✅ Yes |

| Monthly rent (as tenant) | ❌ No | ✅ Yes |

| Insurance premiums | ❌ No | ✅ Yes |

| Children’s school fees (monthly) | ❌ No | ✅ Yes |

| SIP / investment commitments | ❌ No | ✅ Yes |

| Subscriptions (OTT, gym, etc.) | ❌ No | ✅ Yes |

Your True Financial Obligation Ratio:

True Obligation Ratio = (All Fixed Monthly Commitments ÷ Net Take-Home) × 100

All Fixed Commitments = EMIs + Rent + Insurance + School Fees + SIP + Subscriptions

Healthy target: Below 70% of net take-home

(leaving 30% for variable expenses and genuine discretionary spending)Many people who appear financially healthy by bank standards (40% FOIR) are actually over-committed when rent, school fees, and insurance are added — leaving only 15–20% of take-home for food, transport, and variable expenses. This is a financial stress situation waiting to become a crisis.

DTI Red Flags: When to Stop Borrowing

These are the clear signals that your DTI has reached a level requiring action — not additional borrowing:

Red Flag 1 — You are borrowing to meet regular monthly expenses

Using a credit card or app loan to pay for groceries, utilities, or fuel is the clearest sign that your debt obligations have exceeded your income capacity. This is the definition of a debt trap beginning.

Red Flag 2 — Your savings rate has dropped to zero

If you cannot save anything after EMIs and essential expenses — your DTI is effectively above your income’s capacity. The appropriate response is debt reduction, not income hope.

Red Flag 3 — You are taking new loans to repay old ones

If any new borrowing is used to meet existing EMI obligations — this is debt cycling and it accelerates toward default. Stop all new borrowing immediately and seek debt restructuring.

Red Flag 4 — Your DTI exceeds 50% of gross income

Above 50%, the mathematical probability of maintaining all obligations through any income disruption drops sharply. A single month’s salary delay or a ₹30,000 emergency expense can cascade into missed EMIs and a damaged credit score.

Red Flag 5 — Multiple lenders have rejected your applications recently

Loan rejection itself signals that your DTI is above lender comfort levels. Each rejection triggers a hard credit inquiry that further reduces your score — stop applying and focus on reducing existing obligations first.

👉 Related Reading: How to Use a Financial Calculator to Escape the Debt Trap → — the complete step-by-step guide for anyone in debt stress.

DTI and Credit Score: The Relationship

DTI and credit score are the two pillars of loan eligibility — but they are different things that interact:

| Factor | Credit Score | DTI / FOIR |

|---|---|---|

| What it measures | Past payment behaviour | Current income vs current debt load |

| Reflects | How reliably you have repaid | How much capacity you have to repay |

| Improves by | Paying all dues on time | Reducing existing EMIs or increasing income |

| Bank’s use | Determines approval and rate | Determines maximum loan amount |

| Time to improve | 6–18 months minimum | 1–3 months (if debts cleared) |

A high credit score with high DTI: bank may approve but at a lower amount than desired.

A low credit score with low DTI: bank may hesitate on approval despite available capacity.

High credit score + low DTI: the optimal combination — best rates, maximum eligibility, multiple competing offers.

The fastest path to the ideal combination: clear existing small loans (improves DTI immediately + demonstrates responsible debt management for credit score over 3–6 months).

Frequently Asked Questions

Q: What DTI ratio do banks in India typically require for a home loan?

A: Most Indian banks and HFCs apply a FOIR (Fixed Obligation to Income Ratio) limit of 40–55% — meaning the total of all EMIs including the new home loan EMI should not exceed this percentage of your gross monthly income. PSU banks are typically more conservative at 40–50%; private banks and HFCs allow 50–60%. The ideal target for the borrower — as opposed to the bank’s maximum — is keeping FOIR below 40% for genuine financial comfort.

Q: Does rent count in my DTI when applying for a loan?

A: For bank FOIR calculation — monthly rent paid as a tenant is generally NOT included in the obligations calculation. Banks focus on formal EMI obligations. However, for your own financial planning, rent absolutely counts in your personal DTI — it is a fixed monthly outflow that competes with debt service for your income.

Q: How quickly can I improve my DTI ratio?

A: DTI can improve very quickly if you have cash available to clear existing debts. Paying off a loan completely eliminates its EMI immediately — same-month improvement. If you need to save up to clear debts, a realistic improvement timeline is 3–12 months depending on the amount to be cleared and your monthly surplus. Income increases can improve DTI in the same month the increase takes effect if properly documented.

Q: If my DTI is 55%, should I still apply for a home loan?

A: At 55%, most PSU banks will decline. Some HFCs and NBFCs with 60% FOIR limits may approve — but at higher rates. A more financially sound approach: spend 6–12 months reducing existing EMIs through prepayment, then apply when DTI is below 45%. The rate saving from applying at a better DTI typically far exceeds the cost of waiting.

Q: Does my spouse’s income improve my DTI?

A: Yes — significantly. A joint application combines both incomes in the denominator while only counting obligations against that combined income. If your individual DTI is 52% but your spouse earns ₹60,000/month with no debt — your joint DTI on the same obligations drops to under 30%. Always evaluate joint application benefits before deciding to apply alone.

Q: Are credit card balances included in DTI even if I pay the full amount each month?

A: If you pay the full credit card balance every month — banks typically use 5% of the outstanding balance or the minimum due (whichever is higher) as the monthly obligation in FOIR calculation. If you consistently pay in full and have zero outstanding, the impact is minimal. Revolving credit card debt (only paying minimum) is counted in full and significantly damages your FOIR — another strong reason to never carry a credit card balance.

Conclusion

The Debt-to-Income Ratio is the single most honest number in personal finance. It does not care about your job title, your aspirations, or your optimistic income projections. It simply measures reality: what percentage of your income is already spoken for before you decide how to live your life.

A DTI below 36% means financial freedom — the ability to save, invest, respond to opportunities, and absorb shocks. A DTI above 50% means financial fragility — one bad month away from missed payments and a damaged credit score.

The DTI calculator gives you this number in seconds. What you do with it is the most important financial decision you can make.

If your number is good — protect it. If your number is concerning — the improvement strategies in this guide are specific, actionable, and effective within months.

Because financial health is not about how much you earn. It is about how much of what you earn you actually control.

👉 Calculate your exact DTI ratio with our free Debt-to-Income Ratio Calculator →

👉 Related Reading: How Banks Calculate Your Home Loan Eligibility →

👉 Related Reading: Mortgage Calculator — How Much Home Can You Afford? →

👉 Related Reading: Loan Against Property Calculator — Unlock Your Property’s Hidden Value →

👉 Related Reading: How to Use a Financial Calculator to Escape the Debt Trap →

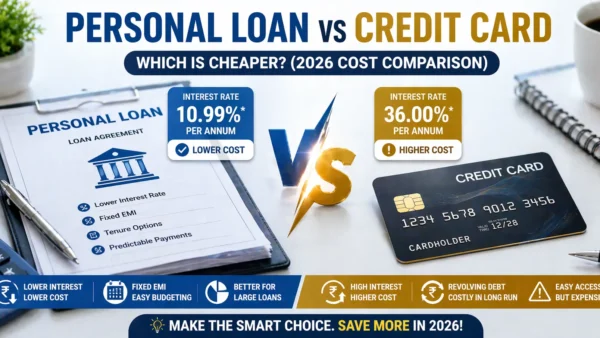

👉 Related Reading: Personal Loan vs Credit Card — Which Is Cheaper? →

👉 Related Reading: Mortgage Refinancing Calculator — When Does It Make Sense? →

👉 Related Reading: Salary After Tax Calculator — What’s Your Real Take-Home Pay? →