You have the order. The client wants 500 units delivered in 60 days. Your workshop can do it — but you need ₹15 lakhs for raw materials, machinery, and labour upfront.

Or maybe it is simpler: cash flow is tight this quarter, and you need a working capital cushion to pay suppliers on time while waiting for customer payments to clear.

Either way, you are about to make one of the most consequential financial decisions a business owner makes: how much debt should your business actually take on?

Too little, and you miss the opportunity. Too much, and a single slow month turns into a cash flow crisis that threatens the entire business. The business loan EMI calculator is the tool that removes the guesswork — showing you exactly what you can afford, before you sign anything.

Here is the complete 2025 guide for every small business owner, MSME, and entrepreneur across India and developing markets.

👉 Calculate your exact business loan EMI and affordability with our free Business Loan EMI Calculator →

How Business Loans Differ From Personal Loans

A business loan is fundamentally evaluated differently than a personal loan. While a personal loan looks primarily at your salary and credit score, a business loan evaluation centres on your business’s ability to generate cash flow that comfortably services the debt.

The Core Business Loan Formula:

Maximum Safe EMI = Net Operating Income × Safety Margin (typically 60–70%)

Where:

Net Operating Income = Revenue − Operating Expenses (before debt payments)

Safety Margin = Buffer to ensure EMI never consumes your entire cash surplus

Example:

Monthly Revenue: ₹8,00,000

Monthly Operating Expenses: ₹6,00,000

Net Operating Income: ₹2,00,000

Maximum Safe EMI (65%): ₹1,30,000This single calculation — rarely done by first-time business borrowers — prevents the single most common cause of small business failure: taking on debt that the business’s actual cash flow cannot support, regardless of how promising the underlying opportunity seems.

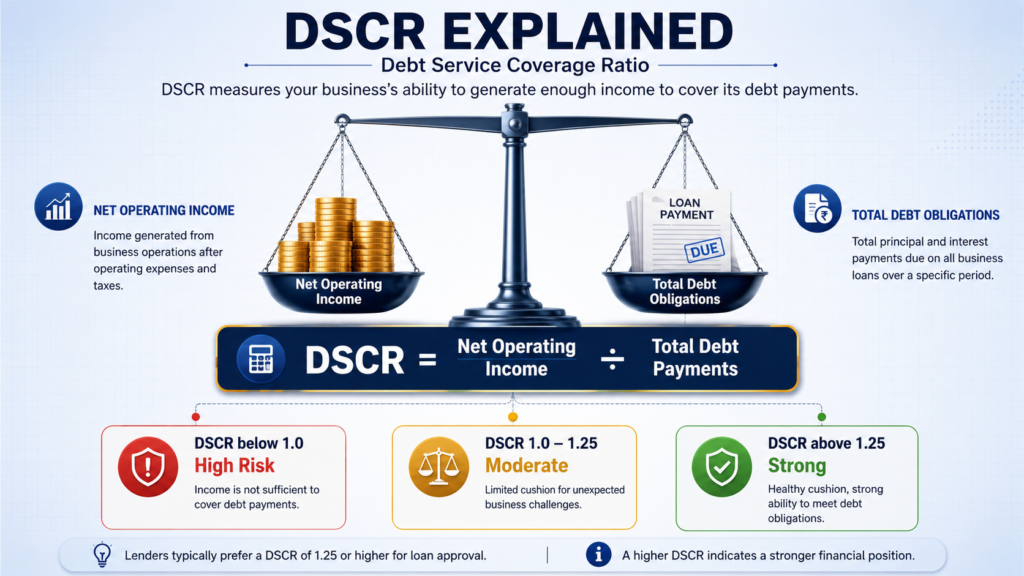

DSCR: The Number That Determines Your Loan Approval

Every bank and NBFC evaluating your business loan application calculates one ratio above all others: the Debt Service Coverage Ratio (DSCR).

DSCR = Net Operating Income ÷ Total Debt Obligations (including the new loan)

Example:

Net Operating Income (annual): ₹24,00,000

Existing Loan EMIs (annual): ₹6,00,000

New Loan EMI being applied for (annual): ₹9,60,000

Total Debt Obligations: ₹15,60,000

DSCR = ₹24,00,000 ÷ ₹15,60,000 = 1.54| DSCR Range | What It Means | Loan Approval Likelihood |

|---|---|---|

| Below 1.0 | Business income cannot cover debt obligations | Almost certain rejection |

| 1.0–1.15 | Income barely covers debt — zero buffer | High risk; likely rejected or heavily scrutinised |

| 1.15–1.25 | Acceptable but tight | Approved with caution; may need collateral |

| 1.25–1.50 | Healthy buffer | Strong approval likelihood |

| Above 1.50 | Comfortable cushion | Excellent approval; better rate negotiation power |

The lender’s logic: A DSCR of 1.25 means your business generates 25% more income than is needed to service all debt — providing a buffer for a slow month, an unexpected expense, or a delayed customer payment. Banks rarely approve loans that would push your DSCR below 1.15–1.20.

👉 Calculate your DSCR and maximum safe loan amount with our free Business Loan EMI Calculator →

Business Loan Interest Rates 2025: Complete Comparison

Interest rates vary significantly based on lender type, collateral, business vintage, and credit profile:

| Lender Type | Interest Rate Range | Processing Fee | Typical Tenure | Collateral |

|---|---|---|---|---|

| Public Sector Banks (SBI, BOB, PNB) | 9.50–13.50% | 0.5–1% | Up to 7 years | Required above ₹10L |

| Private Banks (HDFC, ICICI, Axis) | 11.00–18.00% | 1–2% | Up to 5 years | Required above ₹15L |

| NBFCs (Bajaj Finserv, Lendingkart) | 14.00–28.00% | 1–3% | 1–4 years | Often not required |

| Fintech Lenders (FlexiLoans, Indifi) | 15.00–30.00% | 2–4% | 6 months–3 years | Not required |

| Government Schemes (MUDRA) | 8.50–12.00% | Nil to minimal | Up to 5 years | Not required |

The speed-vs-cost trade-off: PSU banks offer the lowest rates but take 2–4 weeks for approval with extensive documentation. Fintech lenders disburse in 24–48 hours but at rates that can be 2–3x higher. For planned business needs, always start with bank applications. For genuine emergencies, fintech speed may justify the premium — but calculate the true cost first.

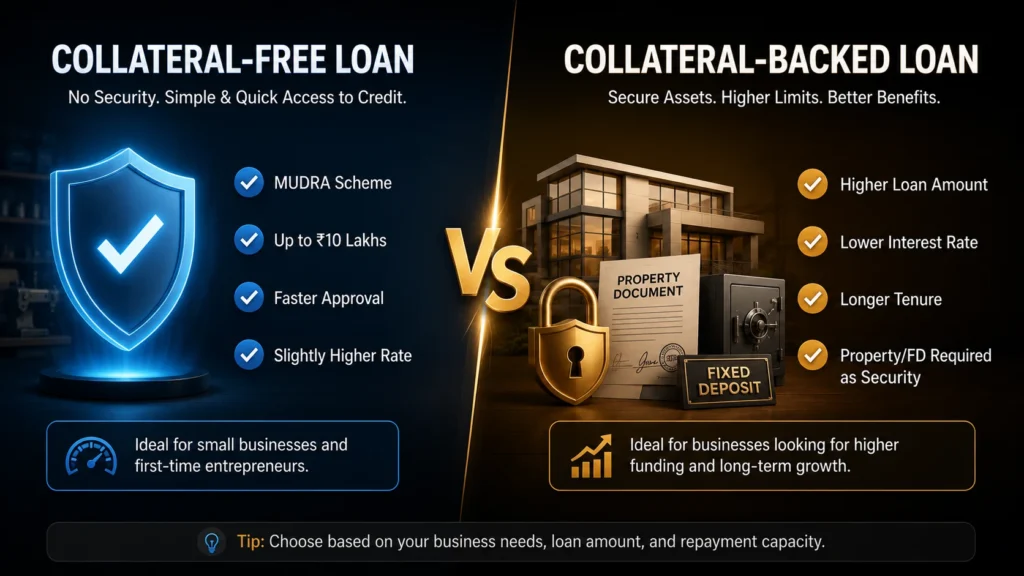

Collateral-Free vs Collateral-Backed: Which Should You Choose?

| Feature | Collateral-Free | Collateral-Backed |

|---|---|---|

| Maximum Amount | Typically up to ₹10–₹20 lakhs | Up to ₹5 crore+ |

| Interest Rate | 12–28% (higher risk premium) | 9–15% (lower risk premium) |

| Approval Speed | Faster (1–7 days) | Slower (2–4 weeks) |

| Documentation | Business proof, bank statements, ITR | Above + property/asset valuation |

| Risk to Owner | Personal guarantee may still apply | Asset can be seized on default |

| Best For | Working capital, small expansion | Equipment purchase, large expansion |

The government’s CGTMSE (Credit Guarantee Fund Trust for Micro and Small Enterprises) scheme allows banks to offer collateral-free loans up to ₹2 crore by providing a government guarantee to the lender — covering up to 85% of the loan in case of default. This has dramatically expanded collateral-free lending access for legitimate small businesses since its enhancement in 2023.

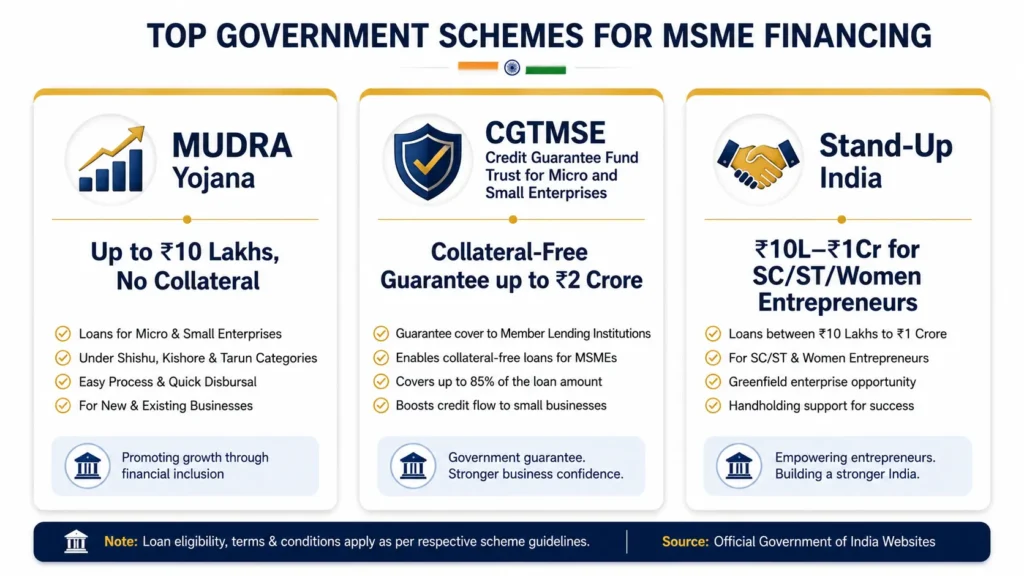

Government Business Loan Schemes: India 2025

| Scheme | Maximum Amount | Interest Rate | Eligibility |

|---|---|---|---|

| MUDRA Yojana (Shishu/Kishor/Tarun) | ₹50,000 / ₹5 lakh / ₹10 lakh | 8.5–12% | Any non-farm income-generating activity |

| CGTMSE | Up to ₹2 crore | Standard bank rate | Collateral-free guarantee for MSMEs |

| Stand-Up India | ₹10 lakh–₹1 crore | Base rate + 3% (max) | SC/ST and women entrepreneurs |

| PMEGP (Prime Minister’s Employment Generation Programme) | Up to ₹50 lakh (manufacturing) | Bank rate, with subsidy 15–35% | New manufacturing/service units |

| SIDBI Schemes | Varies by scheme | 8–13% | Direct and partner-channel MSME lending |

MUDRA Yojana has disbursed over ₹27 lakh crore since its 2015 launch — making it the single largest collateral-free lending program for India’s micro and small businesses. The three-tier structure (Shishu, Kishor, Tarun) allows businesses to graduate to larger loan amounts as they establish repayment history.

👉 Related Reading: GST Calculator — How GST Affects Your Business Profits → — understanding the complete financial picture of your business beyond just loans.

Real Business Loan EMI Calculations

Scenario 1: Small Manufacturing Unit — ₹10 Lakh MUDRA Loan

| Detail | Value |

|---|---|

| Loan Amount | ₹10,00,000 |

| Interest Rate | 10.5% (MUDRA Tarun) |

| Tenure | 5 years |

| Monthly EMI | ₹21,498 |

| Total Repayment | ₹12,89,880 |

| Total Interest | ₹2,89,880 |

| Required Net Monthly Income (DSCR 1.25) | ₹26,873 |

Scenario 2: Retail Expansion — ₹25 Lakh Bank Loan (with collateral)

| Detail | Value |

|---|---|

| Loan Amount | ₹25,00,000 |

| Interest Rate | 11.5% (Private Bank, secured) |

| Tenure | 7 years |

| Monthly EMI | ₹43,845 |

| Total Repayment | ₹36,82,980 |

| Total Interest | ₹11,82,980 |

| Required Net Monthly Income (DSCR 1.25) | ₹54,806 |

Scenario 3: Working Capital — ₹5 Lakh Fintech Loan (urgent, no collateral)

| Detail | Value |

|---|---|

| Loan Amount | ₹5,00,000 |

| Interest Rate | 22% (Fintech, unsecured) |

| Tenure | 18 months |

| Monthly EMI | ₹31,547 |

| Total Repayment | ₹5,67,846 |

| Total Interest | ₹67,846 |

| Required Net Monthly Income (DSCR 1.25) | ₹39,434 |

The fintech loan’s short tenure means the effective monthly EMI is significantly higher despite the smaller principal — this is precisely why fintech loans should be used only for short-term, high-confidence cash flow needs, not as ongoing working capital.

👉 Compare your exact business loan scenarios with our free Business Loan EMI Calculator →

Cash Flow vs Profit-Based Eligibility: The Critical Distinction

Many business owners mistakenly believe loan eligibility is based on annual profit shown in their books. In reality, most lenders evaluate cash flow — which can differ significantly from accounting profit.

Profit-Based View (from books):

Annual Revenue: ₹80,00,000

Annual Expenses (incl. depreciation): ₹65,00,000

Net Profit: ₹15,00,000

Cash Flow View (actual bank statement analysis):

Net Profit: ₹15,00,000

Add back: Depreciation (non-cash): ₹4,00,000

Less: Working capital tied up in inventory/receivables: ₹6,00,000

Actual Cash Available for Debt Service: ₹13,00,000Lenders increasingly use bank statement analysis (12 months of statements) rather than relying solely on ITR-reported profit — because many small businesses under-report profit for tax purposes, making bank statements a more reliable indicator of actual repayment capacity.

The practical implication: If you have been minimising reported profit for tax savings, you may find your loan eligibility lower than your business’s true cash-generating capacity suggests. Some lenders (especially fintech) specifically cater to this segment using GST returns and bank statement cash flow analysis rather than ITR profit alone.

The 5 Most Common Business Loan Mistakes

Mistake 1 — Borrowing the maximum approved amount

Just because a bank approves ₹30 lakhs does not mean you should borrow ₹30 lakhs. Borrow only what your specific business need requires, calculated against realistic cash flow projections — not optimistic ones.

Mistake 2 — Ignoring the DSCR cushion

A DSCR of exactly 1.0 means any revenue dip puts you in default territory. Always maintain DSCR above 1.25 even after accounting for the new loan — building in a genuine safety margin.

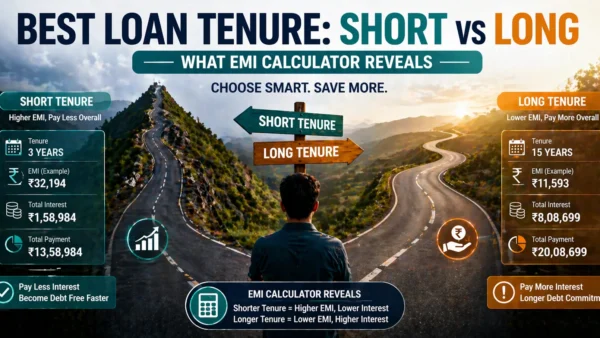

Mistake 3 — Choosing tenure based on lowest EMI alone

A longer tenure reduces monthly EMI but increases total interest paid significantly. Match tenure to the actual useful life of what you are financing — equipment with a 5-year life should not be financed over 10 years.

Mistake 4 — Mixing personal and business finances

Using a personal loan for business needs (or vice versa) creates accounting confusion and often results in losing legitimate tax deductions. Keep business borrowing structurally separate.

Mistake 5 — Not comparing government scheme eligibility first

Many eligible businesses go directly to private NBFCs at 20%+ rates without checking MUDRA, CGTMSE, or Stand-Up India eligibility — schemes that could offer the same capital at half the interest cost.

Business Loan Across Developing Markets

| Country | Typical Rate | Key Government Scheme | Notable Feature |

|---|---|---|---|

| 🇮🇳 India | 9.5–28% | MUDRA, CGTMSE, Stand-Up India | Most comprehensive MSME ecosystem |

| 🇵🇭 Philippines | 10–24% | SB Corp lending programs | Growing fintech SME lending sector |

| 🇳🇬 Nigeria | 15–35% | Bank of Industry (BOI) schemes | High rates reflect inflation environment |

| 🇧🇷 Brazil | 12–30% | BNDES financing | State development bank offers competitive rates |

| 🇰🇪 Kenya | 13–22% | Youth Enterprise Fund, Uwezo Fund | Strong SACCO-based business lending culture |

Frequently Asked Questions

Q: What credit score do I need for a business loan?

A: Most banks require a CIBIL score of 700+ for the business owner as a personal guarantor, alongside the business’s own credit history (CMR score for MSMEs). NBFCs and fintech lenders may approve with scores as low as 650, compensating with higher interest rates.

Q: Can a new business with no track record get a loan?

A: Yes — through MUDRA Shishu loans (up to ₹50,000) and PMEGP for new manufacturing units, which are specifically designed for startups without operating history. Beyond these schemes, most traditional lenders require at least 1–3 years of business vintage.

Q: Is business loan interest tax deductible?

A: Yes — the entire interest paid on a business loan is a fully deductible business expense, reducing your taxable profit. This is separate from and in addition to any personal tax deductions you claim.

Q: What is the difference between a term loan and working capital loan?

A: A term loan provides a lump sum for a specific purpose (equipment, expansion) repaid over a fixed tenure. A working capital loan (often a cash credit or overdraft facility) provides flexible, revolving access to funds for day-to-day operational needs, with interest charged only on the utilised amount.

Q: How much collateral do I need for a ₹50 lakh business loan?

A: Typically, lenders require collateral valued at 100–140% of the loan amount, depending on the asset type and lender risk policy. Property collateral often allows higher LTV (up to 70–75%) compared to other asset classes.

Conclusion

A business loan is not simply a number a bank approves — it is a commitment your business’s actual cash flow must honour every single month, regardless of how that month performs.

The DSCR calculation, the cash-flow-based eligibility check, and the government scheme comparison are not optional extras — they are the difference between debt that fuels growth and debt that threatens survival.

Calculate before you commit. Borrow what your cash flow can truly support — not what the bank is willing to lend. And always check government scheme eligibility before accepting a high-rate private loan.

👉 Calculate your exact business loan EMI and safe borrowing capacity with our free Business Loan EMI Calculator →

👉 Related Reading: GST Calculator — How GST Affects Your Business Profits →

👉 Related Reading: Debt-to-Income Ratio Calculator — Am I Borrowing Too Much? →

👉 Related Reading: How to Use a Financial Calculator to Escape the Debt Trap →

👉 Related Reading: Loan Against Property Calculator — Unlock Your Property’s Hidden Value →