Your home loan EMI is eating 40–50% of your salary every single month. Bills are tight. Savings feel impossible. And the financial stress keeps rising.

You are not alone.

Millions of homeowners across India, Philippines, Nigeria, Kenya, and Brazil are trapped in the same high-EMI cycle — often because nobody told them these simple strategies exist.

Here are 7 proven ways to reduce your home loan EMI by up to 30% — starting this month.

👉 See how much you can save using our free Home Loan EMI Calculator →

What is EMI and Why is it So High?

EMI (Equated Monthly Installment) is the fixed amount you pay to the bank every month. It includes both interest and principal repayment.

The reason your EMI feels so heavy is simple: home loans are large and long. A ₹40 lakh loan at 9% for 20 years generates ₹43+ lakhs in interest alone — almost equal to the loan itself.

The good news? Every strategy below directly attacks one or more of these three drivers:

- Interest rate — lower rate = lower EMI

- Outstanding principal — less principal = less interest

- Remaining tenure — restructuring gives you flexibility

Strategy 1: Refinance to a Lower Interest Rate

This is the single most powerful way to reduce your EMI. If you took your home loan 3–5 years ago at a high interest rate, today’s market rates may be significantly lower. Switching to a new lender — or renegotiating with your current one — at a lower rate can reduce your EMI dramatically.

| Current Rate | New Rate After Refinance | Loan Balance | Monthly EMI Saving | Annual Saving |

|---|---|---|---|---|

| 9.5% | 8.5% | ₹30,00,000 | ₹1,854/month | ₹22,248/year |

| 10% | 8.5% | ₹30,00,000 | ₹2,763/month | ₹33,156/year |

| 11% | 8.75% | ₹40,00,000 | ₹4,890/month | ₹58,680/year |

A 1.5% rate reduction on a ₹40 lakh loan saves you over ₹58,000 per year — that’s real money back in your pocket.

👉 Use our Mortgage Refinance Calculator → to see exactly how much you save by switching your home loan rate.

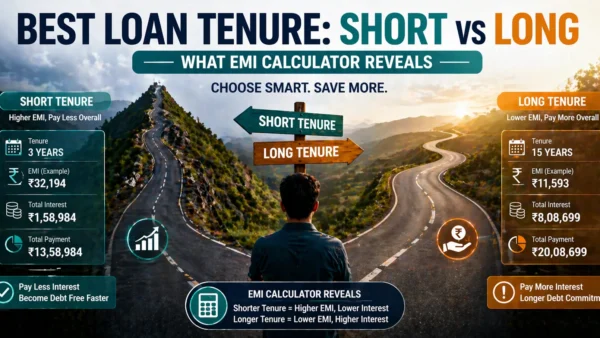

Strategy 2: Extend the Loan Tenure

If you originally took a 10 or 15-year loan and are struggling with the monthly payments, ask your bank to extend the tenure to 20 or 25 years. This immediately reduces your monthly payment.

The trade-off: you pay more total interest over time. But if you’re cash-flow stressed today, this breathing room can be life-changing.

| Loan Amount | Interest Rate | Current Tenure | Extended Tenure | Old EMI | New EMI | Monthly Saving |

|---|---|---|---|---|---|---|

| ₹35,00,000 | 8.5% | 10 years | 20 years | ₹43,437 | ₹30,406 | ₹13,031 |

| ₹50,00,000 | 8.5% | 15 years | 25 years | ₹49,268 | ₹40,260 | ₹9,008 |

Pro tip: If you extend tenure, combine it with Strategy 3 (regular prepayments) to keep total interest under control.

Strategy 3: Make Regular Partial Prepayments

Even small extra payments made consistently can dramatically reduce your outstanding principal. A lower principal means lower future interest — and you can request your bank to recalculate your EMI downward.

Making a prepayment of just ₹50,000 per year on a ₹40 lakh home loan at 8.5% can:

- Save over ₹14 lakhs in total interest

- Reduce your loan tenure by more than 4 years

- Reduce your EMI significantly on recalculation

The earlier you make prepayments, the bigger the impact. Interest is front-loaded — every prepayment in year 1–3 saves far more than the same amount in year 12.

| Year of Prepayment | Prepayment Amount | Total Interest Saved | Months Reduced |

|---|---|---|---|

| Year 1 | ₹2,00,000 | ₹3,84,000 | 28 months |

| Year 3 | ₹2,00,000 | ₹2,95,000 | 21 months |

| Year 7 | ₹2,00,000 | ₹1,52,000 | 12 months |

| Year 12 | ₹2,00,000 | ₹64,000 | 5 months |

👉 Calculate your prepayment savings with our Home Loan Prepayment Calculator →

Strategy 4: Negotiate With Your Existing Bank

Many borrowers don’t realise they can simply walk into their bank and ask for a lower rate — especially if:

- You have made consistent repayments for 2–3+ years

- Your credit score has improved since you took the loan

- Market interest rates have dropped significantly

- You can show competitor banks are offering lower rates

Banks genuinely prefer retaining good customers over losing them to a balance transfer competitor. Use this leverage.

What to say to your bank:

- “I have been offered X% by [Bank Name]. Can you match or beat this rate?”

- “My credit score has improved to 780. I’d like a rate review.”

- “I’ve been your customer for 5 years with zero defaults. I’d like to discuss my current rate.”

Most banks will offer at least a 0.25–0.50% reduction to retain a good borrower — which translates to thousands in annual savings.

Strategy 5: Increase Your Down Payment (For Future Buyers)

If you haven’t taken the loan yet, this is the most impactful strategy. Every extra rupee in down payment is a rupee less of loan — which directly and permanently reduces your monthly EMI.

| Home Price | Down Payment % | Loan Amount | Monthly EMI (8.5%, 20 yr) |

|---|---|---|---|

| ₹50,00,000 | 10% (₹5L) | ₹45,00,000 | ₹39,234 |

| ₹50,00,000 | 20% (₹10L) | ₹40,00,000 | ₹34,874 |

| ₹50,00,000 | 30% (₹15L) | ₹35,00,000 | ₹30,515 |

| ₹50,00,000 | 40% (₹20L) | ₹30,00,000 | ₹26,155 |

Increasing the down payment from 10% to 30% reduces your monthly EMI by ₹8,719 per month — a 22% reduction on the same property at the same rate.

Strategy 6: Transfer the Balance to a Lower-Rate Lender

A home loan balance transfer means moving your outstanding loan amount from your current bank to a new lender offering a lower interest rate. This is one of the most effective tools available to existing borrowers.

How to do it step-by-step:

- Check your current outstanding balance and remaining tenure

- Compare balance transfer rates from at least 3 banks

- Calculate the break-even point — how many months until savings exceed switching cost

- Apply to the new lender with all loan documents

- New lender pays off old bank; you start paying at the lower rate

Key costs to check before transferring:

- Processing fee from new lender: 0.5–1% of loan

- Pre-closure charge from current lender: 0% (floating rate, as per RBI rules in India) to 2% (fixed rate)

- Legal and valuation fees: ₹8,000–₹20,000

👉 Check if balance transfer makes sense for you with our Mortgage Refinance Calculator →

Strategy 7: Opt for a Step-Down EMI Structure

Some banks offer step-down EMI products where you pay higher EMIs in early years (when income is at its peak) and lower EMIs as you approach retirement. This structure lets you:

- Repay more principal in your high-earning years

- Reduce EMI burden as you near retirement

- Pay significantly less total interest over the loan life

This is ideal for borrowers who are currently in their 40s with peak earning years, but want lower obligations in their 50s and 60s.

Bonus: How Much Can You Actually Save?

Let’s combine Strategy 1 (refinancing) + Strategy 3 (annual prepayments) and see the impact:

| Scenario | Loan | Rate | Tenure | Total Interest | Monthly EMI |

|---|---|---|---|---|---|

| Original loan | ₹40,00,000 | 10% | 20 years | ₹55,75,160 | ₹38,601 |

| After refinancing to 8.5% | ₹40,00,000 | 8.5% | 20 years | ₹43,69,760 | ₹34,874 |

| After refinancing + ₹1L/yr prepayment | ₹40,00,000 | 8.5% | ~14 years | ₹27,84,000 | ₹34,874 |

| Total Saving | 6 fewer years | ₹27,91,160 saved | ₹3,727/month less |

That is nearly ₹28 lakhs saved — from two strategies combined.

👉 Model your own savings scenario with our Home Loan EMI Calculator →

Frequently Asked Questions

Q: How much can I realistically reduce my EMI? A: With a combination of refinancing and one prepayment, most borrowers can reduce their effective EMI burden by 15–30%. The exact amount depends on your current rate versus market rate and outstanding balance.

Q: Is home loan balance transfer worth it? A: Generally yes, if the rate difference is more than 0.5% and you have more than 10 years remaining on your loan. Use our calculator to find your exact break-even point.

Q: Will extending tenure hurt my credit score? A: No. Extending loan tenure through a formal bank process does not negatively impact your credit score. However, it means staying in debt longer and paying more total interest — always pair it with prepayments.

Q: Can I reduce EMI without refinancing? A: Yes. Making even small prepayments regularly can allow you to request an EMI reduction from your bank. Your bank recalculates your EMI on the reduced principal balance at any time.

Q: What is the best time to refinance a home loan? A: The best time is when the rate difference exceeds 0.75–1%, you have 10+ years remaining, and your credit score is 750+. Don’t wait for the “perfect” moment — every month of delay costs you in interest.

Conclusion

Reducing your home loan EMI is not complicated — it just requires knowing your options and taking action. Start with Strategy 1 (refinancing) and Strategy 3 (prepayments) — these two alone can transform your financial situation.

The money you save each month doesn’t disappear. It can go into a SIP, build your emergency fund, or simply give you the financial breathing room you’ve been missing.

Use our free Home Loan EMI Calculator → to model each strategy and find your best path forward — today.