You are sitting across from the bank officer. The loan is approved. One final question before you sign:

“Sir, would you like a fixed rate or a floating rate?”

Most first-time home buyers pause here — uncertain, slightly embarrassed, and ultimately defaulting to whatever the bank recommends. Which is almost always the product that is more profitable for the bank.

This decision — made in 30 seconds of awkward silence — can cost you ₹5 lakhs to ₹15 lakhs over the life of your home loan if you choose incorrectly for your specific market situation.

Here is everything you need to make this decision with complete confidence — backed by 10 years of real data and a side-by-side comparison that shows exactly what each rate type costs under every realistic market scenario.

👉 Compare fixed vs floating rates for your loan with our free Mortgage Rate Calculator →

Fixed vs Floating Rate: The Fundamental Difference

Before the numbers, understand what each option actually means:

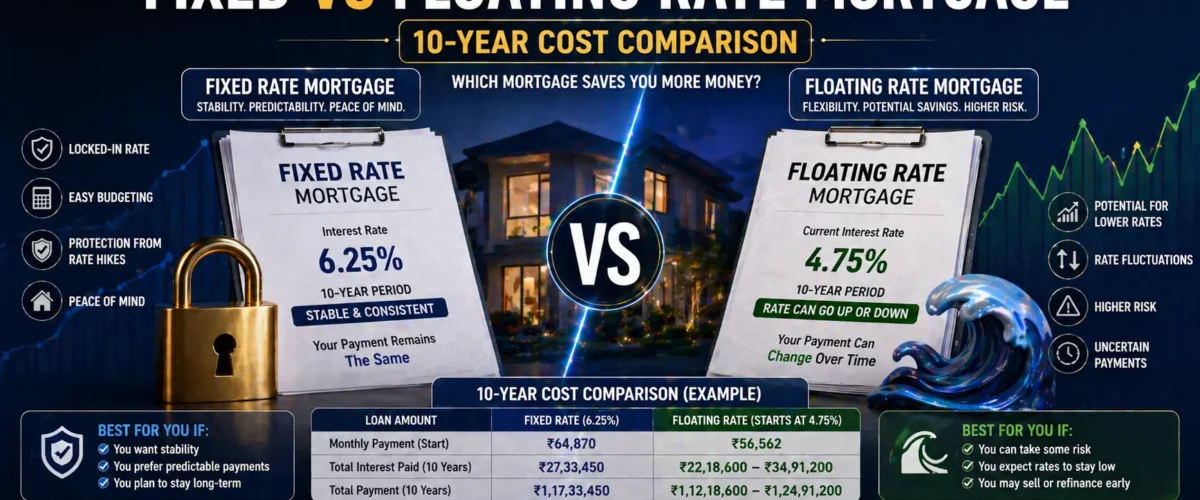

Fixed Rate Mortgage: Your interest rate is locked at a predetermined level for a fixed period — either the entire loan tenure or an initial period (typically 2–5 years) after which it converts to floating. Your EMI amount is completely predictable — it does not change regardless of what happens to market interest rates.

Floating Rate Mortgage: Your interest rate moves up and down with a benchmark rate — typically the RBI repo rate (for repo-linked loans) or MCLR (Marginal Cost of Funds Based Lending Rate). When the benchmark falls, your rate falls and your EMI decreases. When it rises, your rate rises and your EMI increases.

The core philosophical difference: fixed rate buys certainty at a price premium; floating rate offers potential savings with market uncertainty.

Side-by-Side Comparison: All Key Factors

| Feature | Fixed Rate Mortgage | Floating Rate Mortgage |

|---|---|---|

| Interest Rate | Locked — unchanging | Moves with RBI/benchmark rate |

| EMI Stability | 100% predictable | Can increase or decrease |

| Starting Rate | Typically 0.5–1% higher than floating | Lower starting rate |

| Protection from Rate Rise | Full — you are insulated | None — EMI rises with rates |

| Benefit of Rate Cut | None — you miss the reduction | Full — EMI falls automatically |

| Pre-closure Penalty | 2–4% (individual borrowers) | NIL (RBI rule for individuals) |

| Conversion to Other Type | Possible with fee | Possible with fee |

| Best Market Timing | When rates are low and rising | When rates are high and falling |

| Psychological Comfort | High — budget certainty | Lower — EMI uncertainty |

| Most Common in India | Rare — less than 10% of loans | Dominant — 90%+ of home loans |

| Best For | Risk-averse borrowers, tight budgets | Financially flexible borrowers |

The Interest Rate History Lesson: What Happened Over the Last 15 Years

Understanding history is essential to making the right choice in 2026. Here is what happened to RBI repo rates — and therefore floating home loan rates — since 2010:

| Year | RBI Repo Rate | Typical Home Loan Rate (Floating) | What Fixed Rate Borrowers Experienced |

|---|---|---|---|

| 2010 | 5.25% | 8.5–9.0% | Fixed at 10–11% — missed rate cuts |

| 2012 | 8.0% | 10.5–11.0% | Floating hurt borrowers this year |

| 2014 | 8.0% | 10.0–10.5% | Floating and fixed roughly equal |

| 2016 | 6.25% | 9.0–9.5% | Floating borrowers benefited significantly |

| 2018 | 6.5% | 8.5–9.0% | Floating competitive |

| 2020 (COVID) | 4.0% | 6.65–7.0% | Floating borrowers hit historic lows |

| 2022 | 6.5% (rapid rise) | 8.5–9.0% | Floating borrowers felt pain of rapid hike |

| 2023 | 6.5% | 8.5–9.0% | Rates stabilised at higher level |

| 2024–25 | 6.25–6.5% | 8.25–8.75% | Modest cuts began |

The 15-year lesson: Over long periods, floating rate borrowers in India have generally benefited from the overall declining interest rate trend since the early 2000s — though the 2022–23 rapid rate hike cycle caused temporary pain. Borrowers who took floating rate loans in 2019–2020 enjoyed rates as low as 6.65% during COVID — a level no fixed rate product offered.

The 10-Year Cost Comparison: Four Real Market Scenarios

Let us run the actual numbers on a ₹40 lakh home loan with 20 years remaining — comparing fixed at 9% vs floating starting at 8.5% across four distinct market scenarios:

Scenario 1: Rates Fall Steadily (Rate Cut Cycle)

Situation: RBI cuts rates 1.5% over 3 years, then stabilises

| Year | Fixed Rate | Fixed EMI | Floating Rate | Floating EMI |

|---|---|---|---|---|

| Year 1–3 | 9.0% | ₹35,989 | 8.5% → 7.5% | ₹34,874 → ₹32,214 |

| Year 4–7 | 9.0% | ₹35,989 | 7.5% | ₹32,214 |

| Year 8–10 | 9.0% | ₹35,989 | 7.5% | ₹32,214 |

| 10-Year Total Paid | ₹43,18,680 | ₹38,11,920 | ||

| Difference | Floating saves ₹5,06,760 |

In a rate-cut cycle, floating rate borrowers save over ₹5 lakhs in just the first 10 years. Over a 20-year loan, this saving compounds to ₹10–₹12 lakhs.

Scenario 2: Rates Rise Sharply (Rate Hike Cycle)

Situation: RBI hikes rates 2% over 2 years due to inflation, then stabilises

| Year | Fixed Rate | Fixed EMI | Floating Rate | Floating EMI |

|---|---|---|---|---|

| Year 1–2 | 9.0% | ₹35,989 | 8.5% → 10.5% | ₹34,874 → ₹40,021 |

| Year 3–7 | 9.0% | ₹35,989 | 10.5% | ₹40,021 |

| Year 8–10 | 9.0% | ₹35,989 | 10.5% | ₹40,021 |

| 10-Year Total Paid | ₹43,18,680 | ₹46,69,380 | ||

| Difference | Fixed saves ₹3,50,700 |

In a sharp rate-hike cycle, fixed rate borrowers save over ₹3.5 lakhs in 10 years — and their monthly budget is never disrupted by unexpected EMI increases.

Scenario 3: Rates Volatile (Rise then Fall)

Situation: Rates rise 1.5% then fall 2% over 10 years — net lower than start

| Period | Fixed Rate | Fixed EMI | Floating Rate | Floating EMI |

|---|---|---|---|---|

| Year 1–3 (rise) | 9.0% | ₹35,989 | 8.5% → 10.0% | ₹34,874 → ₹38,601 |

| Year 4–6 (peak) | 9.0% | ₹35,989 | 10.0% | ₹38,601 |

| Year 7–10 (fall) | 9.0% | ₹35,989 | 10.0% → 8.0% | ₹38,601 → ₹33,457 |

| 10-Year Total Paid | ₹43,18,680 | ₹43,84,560 | ||

| Difference | Fixed saves ₹65,880 | Near tie |

In a volatile market that rises then falls, fixed and floating rates deliver nearly identical total costs over 10 years — with fixed providing better peace of mind during the hike period.

Scenario 4: Rates Stable (No Significant Movement)

Situation: Rates move less than 0.5% in either direction for 10 years

| Rate Type | EMI | 10-Year Total | Difference |

|---|---|---|---|

| Fixed (9.0%) | ₹35,989 | ₹43,18,680 | More expensive by ₹60,480 |

| Floating (8.5%, stable) | ₹34,874 | ₹41,84,880 | Less expensive |

In a completely stable rate environment, the fixed rate borrower pays more simply because fixed rates are priced 0.5% higher than floating at the outset — reflecting the certainty premium.

Scenario Summary

| Market Scenario | Better Rate Type | 10-Year Saving |

|---|---|---|

| Rates fall 1.5% over 3 years | Floating | ₹5,06,760 |

| Rates rise 2% sharply | Fixed | ₹3,50,700 |

| Volatile (rise then fall) | Near tie | ₹65,880 (Fixed) |

| Stable rates | Floating | ₹1,33,800 |

The historical verdict: Over most 10-year periods in India, floating rate has performed better — because the overall rate trend has been declining and because floating rates start lower. Fixed rate wins when rates rise sharply — as they did in 2022–23.

👉 Run these scenarios for your exact loan amount with our free Mortgage Rate Calculator →

The Rate Premium: Why Fixed Always Starts Higher

Fixed rate mortgages are always priced higher than floating rates at any given moment — typically 0.5–1.5% higher. This premium exists because:

The bank’s perspective: By offering you a fixed rate, the bank takes on the risk that market rates will rise (leaving them stuck lending to you cheaply). To compensate for accepting this risk, they charge you a premium — essentially pricing the insurance into the fixed rate.

Your perspective: You are paying an insurance premium for rate certainty. The question is whether that insurance premium is worth paying given current market conditions and your personal situation.

| Scenario | Should You Pay the Fixed Rate Premium? |

|---|---|

| Rates at historical lows, clearly rising | Yes — lock in before rates increase further |

| Rates at historical highs, clearly falling | No — floating will benefit from cuts |

| Rates uncertain, market volatile | Consider hybrid — fixed for 3 years then float |

| Your budget is extremely tight | Yes — EMI certainty is worth the premium |

| You plan to sell in 5 years | Consider floating — more flexible, lower initial cost |

The Indian Market Reality: Why 90% of Home Loans Are Floating

In India, over 90% of all outstanding home loans are on floating rates. This is not accidental — it reflects both RBI policy and borrower experience:

Reason 1 — RBI Protection for Floating Borrowers: RBI mandates that floating rate home loans cannot carry pre-closure penalties for individual borrowers — making balance transfers easy and keeping banks competitive on rates.

Reason 2 — Fixed Rates Are Rarely Truly Fixed: Most “fixed rate” home loans in India are fixed for 2–5 years and then convert to floating — meaning you pay the fixed rate premium only to end up on floating rate anyway after a few years. Pure 20-year fixed mortgages are rare in India.

Reason 3 — Long-Term Rate Trend Has Favoured Floating: RBI repo rate fell from 9% in 2011 to a historic low of 4% in 2020. Floating rate borrowers benefited from this 9-year declining rate cycle far more than any fixed rate product could have offered.

Reason 4 — MCLR and Repo-Linked Transparency: Since 2019, RBI mandated repo-linked lending rates for home loans — making floating rate transmission faster and more transparent. Rate cuts now reach borrowers within 1–3 months rather than the 6–12 months it used to take.

MCLR vs Repo-Linked Rate: The Floating Rate Within Floating Rates

Not all floating rate loans are equal. Within the floating rate category, there are two distinct types:

MCLR (Marginal Cost of Funds Based Lending Rate) Loans: Your rate is linked to the bank’s internal benchmark — which changes based on the bank’s own cost of funds. Rate transmission is slower — typically 6–12 month reset periods. Banks have more discretion in how they pass on RBI cuts.

Repo-Linked Lending Rate (RLLR) Loans: Your rate is directly linked to RBI’s repo rate — with a fixed spread above it. Rate transmission is faster — rate changes within 1–3 months of any RBI action. More transparent and customer-friendly.

| Feature | MCLR Loan | Repo-Linked Loan |

|---|---|---|

| Benchmark | Bank’s internal MCLR | RBI Repo Rate (external) |

| Rate Reset Period | 6–12 months typically | Monthly (as per RBI mandate) |

| Transmission Speed | Slow — bank has discretion | Fast — automatic |

| Transparency | Lower | Higher |

| Which Is Better? | Neutral in stable rates | Better in rate cut cycles |

| Available Since | 2016 | 2019 (RBI mandate) |

Recommendation for new home loan borrowers in 2026: Always choose a Repo-Linked Rate loan over MCLR. The faster rate transmission means you benefit from RBI cuts immediately — and the greater transparency protects you from banks delaying cut pass-throughs.

The Hybrid Mortgage: The Best of Both Worlds

Several major Indian banks and HFCs offer hybrid mortgages — sometimes called Dual Rate or Tranche-Based loans:

How it works:

- Fixed rate for the first 2–5 years (certainty during initial repayment period)

- Converts to floating rate for the remaining tenure (benefits from long-term rate trends)

Who it is ideal for:

- Borrowers who want budget certainty in the early years when EMI burden is highest

- Those who believe rates may be volatile for 2–3 years then stabilise

- First-time buyers adjusting to a new financial commitment who want time before dealing with rate fluctuations

| Hybrid Loan Structure | Years 1–3 | Years 4–20 | Total Interest (₹40L, 8.5% float scenario) |

|---|---|---|---|

| Fixed then floating | 9.0% (fixed) | 8.0% (floating, rates fell) | ₹41,12,000 |

| Pure floating | 8.5% throughout → 8.0% | — | ₹38,11,920 |

| Pure fixed | 9.0% throughout | — | ₹50,38,760 |

The hybrid sits between pure floating and pure fixed — offering moderate certainty at moderate total cost.

How to Switch Between Fixed and Floating: The Conversion Option

If you have already taken a loan and market conditions change, you are not permanently locked in. Most banks allow conversion between rate types:

| Conversion | Process | Typical Fee | When to Consider |

|---|---|---|---|

| Floating → Fixed | Request in writing; bank resets at current fixed rate | ₹5,000–₹15,000 | When rates appear to be near bottom and likely to rise significantly |

| Fixed → Floating | Request in writing; bank resets at current floating rate | ₹5,000–₹15,000 | When fixed rate significantly exceeds current floating rate |

| MCLR → Repo-Linked | Most banks allow one-time conversion | ₹0–₹5,000 | Almost always beneficial — repo-linked is more transparent |

| Balance Transfer (any type) | Full refinancing to new lender | ₹30,000–₹60,000 | When rate difference exceeds 0.75% and break-even is under 24 months |

The conversion fee of ₹5,000–₹15,000 is trivial compared to the potential savings from switching at the right time. Do not let a small fee prevent you from optimising your home loan rate.

👉 Related Reading: Mortgage Refinancing Calculator — When Does It Make Sense? → — the complete guide to switching lenders for better rates.

The 2026 Rate Outlook: What Should You Choose Right Now?

Note: This represents the rate environment as of early 2026. Always verify current RBI policy and market forecasts before making any decision.

Current situation (2026):

- RBI repo rate: 6.25–6.5% (after modest cuts from the 6.5% peak)

- Typical floating home loan rate: 8.25–8.75%

- Typical fixed home loan rate: 9.0–9.5% (where available)

- Rate direction: Cautious easing cycle beginning — further modest cuts expected

Implication for the fixed vs floating decision in 2026:

| Borrower Profile | Recommended Choice | Reasoning |

|---|---|---|

| New borrower, first home loan | Floating (Repo-Linked) | Rates in easing cycle — likely to benefit from cuts |

| Budget is extremely tight (EMI is 35%+ of income) | Fixed (if available) or hybrid | Cannot afford EMI increases |

| Expecting job change or income uncertainty | Floating | Easier to refinance if needed; lower initial EMI |

| Planning to foreclose in 5–7 years | Floating | No pre-closure penalty; lower initial cost |

| Existing floating borrower at 9.5%+ | Refinance to lower floating | Market rates have moved down |

| Existing fixed borrower at 8.5% or below | Stay fixed | Rate is competitive; switching cost not justified |

The general 2026 recommendation for most new borrowers: floating rate, repo-linked, with a lender offering the lowest spread above the repo rate. The modest easing cycle means floating borrowers are likely to see further rate reductions over the next 12–24 months.

Fixed vs Floating Across Developing Markets

The fixed vs floating dynamics differ significantly across developing markets:

| Country | Dominant Loan Type | Fixed Rate Premium | Special Considerations |

|---|---|---|---|

| 🇮🇳 India | Floating (90%+ of loans) | 0.5–1.0% | RBI ban on floating pre-closure penalty; RLLR transparency |

| 🇵🇭 Philippines | Both common | 0.5–1.0% | Pag-IBIG offers fixed rates; commercial banks mostly floating |

| 🇳🇬 Nigeria | Fixed dominant | N/A — high rates | 15–22% environment makes tenure-matched fixed rates critical |

| 🇧🇷 Brazil | Both common | 1.0–2.0% | Portabilidade makes switching easy; IPCA-linked products popular |

| 🇰🇪 Kenya | Floating dominant | 1.5–2.0% | CBK rate linkage; limited fixed rate products |

| 🇵🇰 Pakistan | Both, Islamic finance growing | 1.0–2.0% | Diminishing musharakah (Islamic) often effectively fixed |

Nigeria’s special case: With benchmark rates at 15–22%, the fixed vs floating decision is particularly critical. A Nigerian borrower who locked in a fixed rate in 2020 at 15% during a rate peak — only to see rates rise further — is in a difficult position. In very high-rate environments, floating rates offer the possibility of relief when rates eventually fall, but expose borrowers to severe short-term stress.

The EMI Impact of Rate Changes: A Sensitivity Table

Understanding exactly how much your EMI changes with rate movements helps you plan for worst and best case scenarios:

Loan: ₹40 Lakhs, 20 Years Remaining

| Rate | Monthly EMI | Annual EMI | Change vs 8.5% Baseline |

|---|---|---|---|

| 7.0% | ₹31,017 | ₹3,72,204 | −₹47,124/year (saving) |

| 7.5% | ₹32,224 | ₹3,86,688 | −₹32,640/year |

| 8.0% | ₹33,457 | ₹4,01,484 | −₹17,844/year |

| 8.5% (Baseline) | ₹34,874 | ₹4,18,488 | Baseline |

| 9.0% | ₹35,989 | ₹4,31,868 | +₹13,380/year |

| 9.5% | ₹37,285 | ₹4,47,420 | +₹28,932/year |

| 10.0% | ₹38,601 | ₹4,63,212 | +₹44,724/year |

| 10.5% | ₹39,933 | ₹4,79,196 | +₹60,708/year |

| 11.0% | ₹41,283 | ₹4,95,396 | +₹76,908/year |

A 2% rate rise on ₹40 lakhs adds ₹44,724 per year to your home loan cost. For a household with tight margins, this is a serious financial stress. For a household with comfortable buffers, it is manageable — which is why your financial resilience matters as much as market direction when choosing between fixed and floating.

The Practical Decision Framework: Your Personal Answer

Use this framework to determine what is right for your specific situation:

Step 1 — Assess your budget flexibility

Current EMI as % of take-home income:

Below 25%: High flexibility — floating rate comfortable

25–35%: Moderate flexibility — floating manageable with small buffer

35–40%: Low flexibility — consider fixed or hybrid

Above 40%: Dangerously stretched — do not take the loan yetStep 2 — Assess your rate view

Current rates vs 5-year historical average:

Well below average: Rates likely to rise → Fixed favoured

Near average: Uncertain → Hybrid reasonable

Well above average: Rates likely to fall → Floating strongly favouredStep 3 — Assess your tenure and plan

Planning to sell/close in under 7 years: Floating (no penalty, lower cost)

Planning to stay 15+ years: Floating if current rates above average, hybrid if below

Absolute budget certainty required (very tight income): Fixed or hybridStep 4 — Choose based on your profile:

| Profile | Recommended Choice |

|---|---|

| First-time buyer, moderate income, 2026 rates | Floating — repo-linked |

| Senior professional, tight post-retirement budget | Fixed or hybrid |

| Young professional, growing income, career upside | Floating — benefit from future easing |

| Self-employed, variable income | Fixed — EMI certainty is essential |

| Investor property, planning exit in 5–7 years | Floating — lower cost, no penalty |

The Pre-Closure Penalty Trap: Why It Matters for Fixed Rates

The most financially dangerous aspect of fixed rate home loans in India is the pre-closure penalty:

Most fixed rate loans charge 2–4% of outstanding principal if you repay early — whether through a lump sum prepayment, balance transfer, or full foreclosure.

What this means in practice:

₹35 lakh outstanding balance

Pre-closure penalty at 3% = ₹1,05,000

If you want to refinance to a lower floating rate:

₹1,05,000 penalty + ₹40,000 processing fees = ₹1,45,000 switching cost

Break-even on ₹2,000/month saving = 72 months (6 years)A fixed rate loan with a pre-closure penalty can trap you into a sub-optimal rate for years — unable to refinance without paying a penalty that extends your break-even well beyond your planning horizon.

The floating rate advantage: RBI’s prohibition on pre-closure penalties for floating rate individual home loans means you can always refinance, prepay, or foreclose without penalty — maintaining complete flexibility throughout your loan life.

This flexibility has enormous financial value — and it is one of the strongest arguments for choosing floating over fixed for most individual borrowers.

👉 Related Reading: EMI vs Lump Sum Repayment — Which Saves More Money? → — how pre-closure flexibility enables smart prepayment strategies. 👉 Related Reading: How to Reduce Your Home Loan EMI by 30% → — leveraging flexible prepayment to dramatically reduce total interest.

Frequently Asked Questions

Q: Is fixed or floating rate better for a home loan in India in 2026? A: For most new borrowers in 2026, floating rate (repo-linked) is recommended. The RBI is in a cautious easing cycle with further modest cuts expected — meaning floating borrowers are likely to benefit from rate reductions over the next 12–24 months. The floating rate also starts 0.5–1% lower than fixed and carries no pre-closure penalty — giving you full flexibility. Choose fixed only if your budget is very tight and you genuinely cannot absorb any EMI increase.

Q: What happens to my floating rate EMI when RBI cuts rates? A: For repo-linked loans, your rate decreases by exactly the RBI cut amount within 1–3 months of the RBI action. Your bank must notify you of the new rate and revised EMI schedule. You can choose to reduce EMI (keeping tenure same) or reduce tenure (keeping EMI same — always choose this for maximum interest saving).

Q: Can I switch from floating to fixed rate on my existing home loan? A: Yes — most banks allow conversion with a processing fee of ₹5,000–₹15,000. However, the fixed rate offered at conversion will be the current market fixed rate — which may be significantly higher than your current floating rate. Calculate carefully before converting. Switching from floating to fixed typically only makes sense if you expect rates to rise by 2%+ from current levels.

Q: Is there such a thing as a truly fixed rate home loan for 20 years in India? A: Pure 20-year fixed rate home loans are very rare in India. Most products marketed as “fixed” are fixed for 2–5 years and then automatically convert to floating. Always read the fine print — ask specifically: “Is this rate fixed for the entire 20-year tenure or for an initial period only?” A product that is fixed for only 2 years and then converts to floating provides very limited protection.

Q: My floating rate has gone up to 9.5% but I see new loans being offered at 8.5%. What should I do? A: This is a common situation — existing floating rate borrowers can be at higher rates than new borrowers due to base rate legacy issues (old MCLR vs new repo-linked). First, call your bank and ask for a rate revision. If they refuse or offer an inadequate reduction, calculate the break-even on a balance transfer to a new lender. A 1% rate difference on a large outstanding balance with 12+ years remaining almost certainly justifies switching. Use our refinancing calculator to confirm.

Q: Should I choose fixed or floating if I am self-employed with variable income? A: Fixed rate is strongly recommended for self-employed borrowers with variable income. The EMI certainty of a fixed rate means you always know exactly what your mortgage commitment is — regardless of how your income fluctuates month to month. The floating rate uncertainty is much more stressful when income is variable. The premium you pay for certainty is genuinely worth it for the financial stability it provides.

Conclusion

The fixed vs floating decision is not purely mathematical — it sits at the intersection of market economics, personal psychology, and individual financial resilience.

The mathematics generally favour floating rates in India over long periods — because rates have trended downward over decades and floating rates start lower. But the mathematics of a specific year can favour fixed — as 2022–23’s rapid rate hike cycle demonstrated painfully for unprepared floating rate borrowers.

The framework for your decision is clear:

- Start with your budget flexibility — can you genuinely absorb a 2% rate rise without financial stress?

- Assess the current rate environment — are rates near historical highs (floating favoured) or historical lows (fixed worth considering)?

- Value the pre-closure flexibility — floating rate’s zero penalty gives you permanent refinancing freedom that fixed rate takes away

- Consider your tenure and plans — longer horizon and plan to stay favours optimising for total cost; shorter horizon favours flexibility

For most Indian borrowers in 2026 — on a repo-linked floating rate with a competitive spread, the flexibility of zero pre-closure penalty, and the potential benefit of continued rate easing — floating is the stronger default choice.

But if your budget is tight, your income is variable, or the thought of an unexpected EMI increase keeps you awake at night — the certainty of a fixed rate premium is not financial weakness. It is rational risk management.

Know your situation. Choose accordingly. And use our calculator to see the 10-year cost difference before you sign anything.

👉 Compare fixed vs floating for your exact loan with our free Mortgage Rate Calculator → 👉 Related Reading: Mortgage Refinancing Calculator — When Does It Make Sense? → 👉 Related Reading: Mortgage Calculator — How Much Home Can You Afford? → 👉 Related Reading: How Banks Calculate Your Home Loan Eligibility → 👉 Related Reading: How to Reduce Your Home Loan EMI by 30% → 👉 Related Reading: EMI vs Lump Sum Repayment — Which Saves More Money? → 👉 Related Reading: Home Loan vs Rent — Which is Cheaper in 2026? → 👉 Related Reading: Real Estate ROI Calculator — Is Property a Good Investment? →