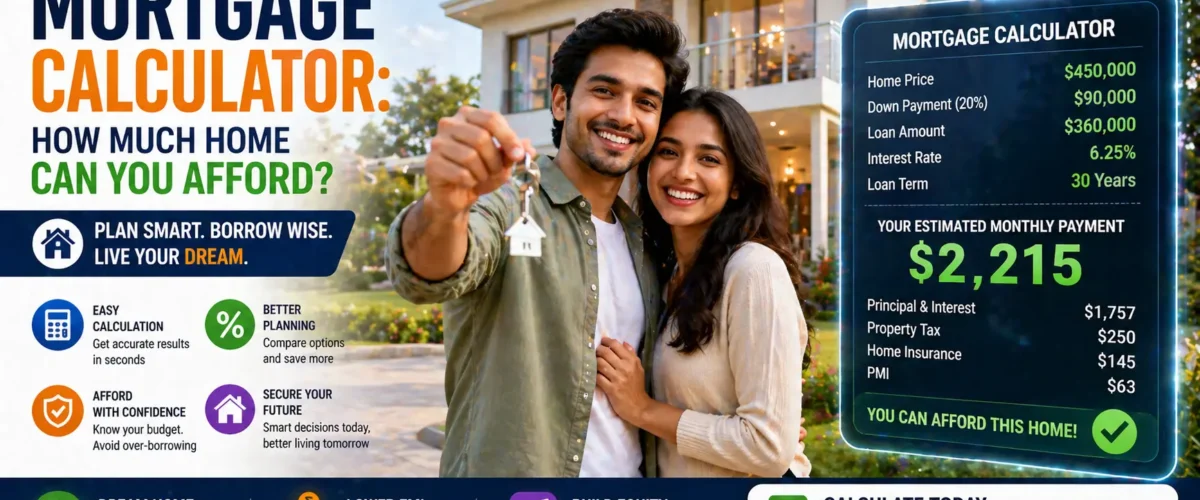

Buying a home is the single biggest financial decision most people ever make.

Yet the overwhelming majority of first-time buyers skip the single most important step before starting their property search: knowing exactly what they can afford.

They fall in love with a property first. They calculate affordability second. And thousands of families are spending the next 20 years financially stressed — because the monthly mortgage payment that looked manageable at the signing table is now suffocating their budget every single month.

You do not have to be one of them.

The mortgage calculator answers the most important question in home buying before you ever walk into a showroom, visit a property site, or talk to a bank: exactly how much home can you afford — based on your real income, real debts, and real financial situation?

Here is everything you need to know — with real numbers for every income level across developing markets.

👉 Find your exact home affordability number right now with our free Mortgage Calculator →

The Question Banks Ask — and the One You Should Ask First

When you approach a bank for a home loan, they ask one question: “How much can we safely lend you?”

The question you should be asking first is different: “How much can I comfortably repay — every month — for the next 15–20 years — without compromising my savings, investments, emergency fund, and quality of life?”

These two questions often produce very different numbers.

Banks approve loans based on their risk — your ability to repay as assessed by income, credit score, and existing obligations. They will frequently approve amounts significantly higher than what is genuinely comfortable for your budget and financial goals.

The mortgage calculator answers your question — not the bank’s.

The 28% Golden Rule: Your Affordability Starting Point

Financial planners across every market agree on one foundational principle: your monthly mortgage payment should never exceed 28–30% of your gross monthly income.

This is called the front-end debt-to-income ratio — and it exists because it leaves adequate income for all other essential expenses, savings, investments, and life’s inevitable unexpected costs.

Maximum Comfortable Monthly EMI = Gross Monthly Income × 28%

Example:

Gross Monthly Income: ₹80,000

Maximum Monthly Mortgage EMI: ₹80,000 × 28% = ₹22,400/monthIf your mortgage payment exceeds 30% of gross income, you are technically house-poor — your home is consuming too large a share of your earnings, leaving insufficient room for everything else that matters in your financial life.

Home Affordability Table: By Monthly Income

| Gross Monthly Income | Max Comfortable EMI (28%) | Affordable Loan Amount (8.5%, 20yr) | Affordable Home Price (20% down) |

|---|---|---|---|

| ₹25,000 | ₹7,000 | ₹6,03,000 | ₹7,53,750 |

| ₹35,000 | ₹9,800 | ₹8,44,200 | ₹10,55,250 |

| ₹50,000 | ₹14,000 | ₹12,06,000 | ₹15,07,500 |

| ₹75,000 | ₹21,000 | ₹18,09,000 | ₹22,61,250 |

| ₹1,00,000 | ₹28,000 | ₹24,12,000 | ₹30,15,000 |

| ₹1,25,000 | ₹35,000 | ₹30,15,000 | ₹37,68,750 |

| ₹1,50,000 | ₹42,000 | ₹36,18,000 | ₹45,22,500 |

| ₹2,00,000 | ₹56,000 | ₹48,24,000 | ₹60,30,000 |

| ₹2,50,000 | ₹70,000 | ₹60,30,000 | ₹75,37,500 |

| ₹3,00,000 | ₹84,000 | ₹72,36,000 | ₹90,45,000 |

Note: Loan amount calculated based on 28% FOIR at 8.5% interest for 20-year tenure. Home price assumes 20% down payment. Actual bank eligibility varies by profile.

👉 Get your exact personalised affordability number with our free Mortgage Affordability Calculator →

The Three Affordability Rules Every Home Buyer Must Know

Different financial traditions have developed different affordability rules — each capturing a different dimension of what “affordable” truly means:

Rule 1: The 28% Monthly Payment Rule

Your mortgage EMI should not exceed 28% of gross monthly income.

This ensures your monthly cash flow remains healthy with adequate room for all other expenses, savings, and investments.

Rule 2: The 3X Annual Income Rule

Your home price should not exceed 3 times your gross annual income.

This is the long-term affordability check — ensuring you are not taking on debt so large that it dominates your financial life for decades.

Example:

Annual Income: ₹9,00,000 (₹75,000/month)

Maximum Home Price (3X Rule): ₹27,00,000Rule 3: The 20% Down Payment Rule

Save at least 20% of the home price as down payment before buying.

This reduces your loan amount, eliminates loan insurance requirements, gets you better interest rates, and protects you from going underwater if property values temporarily decline.

Example:

Home Price: ₹30,00,000

Minimum Down Payment (20%): ₹6,00,000

Loan Amount: ₹24,00,000| Affordability Rule | Formula | Example (₹75,000/month income) | Purpose |

|---|---|---|---|

| 28% Monthly Payment Rule | Max EMI = Income × 28% | Max EMI = ₹21,000 | Monthly cash flow protection |

| 3X Annual Income Rule | Max Price = Annual Income × 3 | Max Price = ₹27,00,000 | Long-term debt management |

| 20% Down Payment Rule | Down = Price × 20% | Down = ₹5,40,000 minimum | Equity protection |

When all three rules point to the same affordability range — you have found your true comfortable home buying budget.

👉 Related Reading: Down Payment Calculator — How to Buy a House Faster → — complete guide to saving your down payment faster.

The Mortgage Calculator Breakdown: What Your EMI Actually Contains

Every mortgage EMI payment contains multiple components — and understanding each one helps you see exactly where your money goes every month:

| Component | What It Is | Typical Amount on ₹30L Loan | Changes Over Time? |

|---|---|---|---|

| Principal Repayment | Actual reduction of your loan balance | ₹4,200 in Year 1 → ₹22,000 in Year 20 | Increases each year |

| Interest Payment | Cost of borrowing the outstanding balance | ₹21,250 in Year 1 → ₹3,450 in Year 20 | Decreases each year |

| Property Tax (if escrowed) | Annual property tax divided into monthly payments | ₹1,000–₹3,000/month | Increases with property value |

| Home Insurance | Annual insurance premium divided monthly | ₹500–₹1,500/month | Relatively stable |

| Total Monthly Payment | ₹26,950–₹47,750 | Varies by inclusion |

The most important insight: in the early years of your mortgage, the vast majority of your EMI goes toward interest — not principal. On a ₹30 lakh loan at 8.5% in Year 1, only ₹4,200 of your ₹25,450 EMI reduces the actual loan balance. The rest (₹21,250) is interest.

This is why making prepayments in the early years saves so much more money than the same prepayment later — you are cutting into the years with the heaviest interest loading.

👉 Related Reading: EMI vs Lump Sum Repayment — Which Saves More Money? → — the complete guide to using prepayments to slash your total interest cost.

How Interest Rate Affects What You Can Afford: The Rate Sensitivity Table

A 1% change in interest rate has a far larger impact on what you can afford than most buyers realise:

| Interest Rate | Monthly EMI on ₹30L (20yr) | Monthly EMI on ₹40L (20yr) | Monthly EMI on ₹50L (20yr) | Total Interest on ₹30L |

|---|---|---|---|---|

| 7.5% | ₹24,168 | ₹32,224 | ₹40,280 | ₹28,00,320 |

| 8.0% | ₹25,093 | ₹33,457 | ₹41,821 | ₹30,22,320 |

| 8.5% | ₹26,036 | ₹34,715 | ₹43,394 | ₹32,48,640 |

| 9.0% | ₹26,992 | ₹35,989 | ₹44,987 | ₹34,78,080 |

| 9.5% | ₹27,964 | ₹37,285 | ₹46,607 | ₹37,11,360 |

| 10.0% | ₹28,950 | ₹38,600 | ₹48,250 | ₹39,48,000 |

| 10.5% | ₹29,950 | ₹39,933 | ₹49,916 | ₹41,88,000 |

A 2% difference in interest rate (8.5% vs 10.5%) on a ₹30 lakh loan costs you ₹9,39,360 extra in total interest — almost a third of the loan amount — over 20 years. This is why comparing lenders before accepting any offer is not just advisable — it is financially critical.

👉 Related Reading: Fixed vs Floating Rate Mortgage — 10-Year Cost Comparison → — which rate type saves you more money over your loan life.

The Hidden Costs of Home Buying Nobody Warns You About

The mortgage EMI is only part of your true monthly cost of home ownership. Most first-time buyers are shocked by the additional costs that appear after they move in:

| Cost Category | Typical Annual Amount | Monthly Equivalent | Often Missed By Buyers? |

|---|---|---|---|

| Property Tax | ₹15,000–₹50,000 | ₹1,250–₹4,167 | Frequently |

| Home Insurance | ₹8,000–₹20,000 | ₹667–₹1,667 | Often |

| Society/HOA Maintenance | ₹24,000–₹72,000 | ₹2,000–₹6,000 | Usually |

| Repairs and Maintenance | ₹30,000–₹60,000 (1% of value) | ₹2,500–₹5,000 | Almost always |

| Sinking Fund Contributions | ₹6,000–₹24,000 | ₹500–₹2,000 | Always |

| Utility Connection Upgrades | ₹10,000–₹30,000 (one-time) | Amortised | Always |

| Stamp Duty and Registration | 5–7% of property value (one-time) | — | Underestimated |

| Total Additional Monthly Cost | ₹6,917–₹18,834 |

On a ₹50 lakh property, total additional ownership costs can add ₹7,000–₹19,000 per month on top of your mortgage EMI. This is the real reason many home buyers feel financially stretched — they budgeted for the EMI but not for the full cost of ownership.

The true monthly cost of home ownership = Mortgage EMI + Property Tax/12 + Insurance/12 + Maintenance/12 + Society Fees

Always calculate this full number before committing to any purchase.

Mortgage Affordability Across Developing Markets: 2025 Data

| Country | Avg Interest Rate | Income Level | Comfortable EMI (28%) | Affordable Loan | Affordable Home (20% down) |

|---|---|---|---|---|---|

| 🇮🇳 India | 8–9.5% | ₹75,000/month | ₹21,000 | ₹18,09,000 | ₹22,61,250 |

| 🇵🇭 Philippines | 6–8% | ₱30,000/month | ₱8,400 | ₱8,30,000 | ₱10,37,500 |

| 🇳🇬 Nigeria | 15–22% | ₦300,000/month | ₦84,000 | ₦3,90,000 | ₦4,87,500 |

| 🇧🇷 Brazil | 10–13% | R$5,000/month | R$1,400 | R$1,28,520 | R$1,60,650 |

| 🇰🇪 Kenya | 13–17% | KSh 80,000/month | KSh 22,400 | KSh 15,20,000 | KSh 19,00,000 |

| 🇵🇰 Pakistan | 18–22% | PKR 80,000/month | PKR 22,400 | PKR 9,80,000 | PKR 12,25,000 |

The Nigeria and Pakistan challenge: With interest rates at 18–22%, the affordable loan amount is dramatically constrained relative to income — making home ownership financially very difficult on average incomes. In these markets, government housing schemes (Nigeria’s Federal Mortgage Bank, Pakistan’s Mera Pakistan Mera Ghar) offer subsidised rates that significantly improve affordability for first-time buyers.

The 5 Factors That Determine Your Actual Mortgage Eligibility

The affordability calculator tells you what is comfortable. The bank’s eligibility calculation tells you what they will actually approve. Here are the five factors that determine both:

Factor 1: Monthly Income — The Primary Driver

Banks calculate your maximum EMI as 40–55% of your gross monthly income (this is higher than the comfortable 28% because banks include all existing EMIs in this calculation, not just the home loan).

Bank Formula: New Home Loan EMI = (Gross Income × 50%) − All Existing EMIs

Example:

Gross Income: ₹1,00,000/month

Existing EMIs (car + personal loan): ₹15,000/month

Maximum Home Loan EMI approved: (₹1,00,000 × 50%) − ₹15,000 = ₹35,000/month

At 8.5% for 20 years: Eligible loan = ₹35,000 × 172 = ₹60,20,000Factor 2: Credit Score — The Rate Determiner

Your credit score determines both whether you are approved and what interest rate you receive. A 780+ score can get you a rate 1–1.5% lower than a 650 score — saving lakhs over the loan life.

| Credit Score | Typical Rate Offered | Monthly EMI Difference on ₹30L (20yr) | 20-Year Total Cost Difference |

|---|---|---|---|

| 800+ | 8.25% | ₹25,704 | Baseline |

| 750–799 | 8.75% | ₹26,520 | +₹1,95,840 |

| 700–749 | 9.25% | ₹27,348 | +₹3,93,360 |

| 650–699 | 10.00% | ₹28,950 | +₹7,77,600 |

| Below 650 | Rejection or 11%+ | ₹30,930+ | +₹12,54,240+ |

Factor 3: Existing Debt — The Eligibility Reducer

Every existing EMI (car loan, personal loan, credit card minimum due) directly reduces your home loan eligibility. Clearing small debts before applying can increase your eligible home loan amount by ₹5–₹15 lakhs.

Factor 4: Employment Stability — The Approval Factor

Banks strongly prefer salaried applicants with 2+ years at their current employer. Self-employed applicants need 3+ years of consistent IT returns. Job changes within 6 months of application frequently result in rejection.

Factor 5: Down Payment — The LTV Ratio

The higher your down payment as a percentage of property value, the lower the Loan-to-Value (LTV) ratio — meaning the bank lends against a smaller portion of the property’s value, reducing their risk and often resulting in better rates.

| Down Payment | LTV Ratio | Typical Interest Rate Impact |

|---|---|---|

| 10% (minimum) | 90% LTV | Standard rate |

| 20% | 80% LTV | 0.1–0.25% rate improvement possible |

| 30% | 70% LTV | 0.25–0.5% rate improvement possible |

| 40%+ | 60% LTV | Best available rates |

👉 Related Reading: How Banks Calculate Your Home Loan Eligibility → — the complete inside guide to exactly how bank eligibility formulas work.

First-Time Buyer Mistakes That Cost Lakhs

Mistake 1 — Borrowing the maximum the bank approves. Bank approval ≠ affordable amount. Banks will approve up to 55% FOIR — leaving you just enough to eat and pay bills with nothing for savings, investments, or emergencies. Use the 28% rule, not the bank’s maximum.

Mistake 2 — Ignoring the total cost of ownership. Buying a home for a ₹30,000 EMI when the true monthly cost (EMI + maintenance + property tax + society fees) is ₹38,000 destroys the budget immediately after moving in.

Mistake 3 — Not comparing lenders. Most first-time buyers accept the first loan offer they receive. Shopping just 3 lenders can save 0.5–1% on the rate — worth ₹5–₹12 lakhs over 20 years on a ₹40 lakh loan.

Mistake 4 — Buying before the credit score is optimised. Buying with a 680 credit score when 6 months of disciplined credit management could push it to 760 costs you 0.75–1% higher interest rate for the entire 20-year loan life.

Mistake 5 — Using the entire down payment savings for the purchase. Leaving zero financial buffer after buying is the fastest route to financial stress. Always retain 3–6 months of all expenses (including new EMI) as emergency fund after the purchase is complete.

👉 Related Reading: Home Loan vs Rent — Which is Cheaper in 2025? → — should you even buy, or does renting make better financial sense right now?

The Mortgage Calculator: 5 Scenarios Solved

Scenario 1: First-Time Buyer, ₹60,000/month Salary

- Gross income: ₹60,000/month

- Existing EMIs: ₹5,000 (car loan)

- Available for home loan EMI (28% rule): ₹16,800 − ₹5,000 = ₹11,800/month

- Affordable loan at 8.5%, 20 years: ₹10,17,600 approx

- Required down payment (20%): ₹2,54,400

- Affordable home price: ₹12,72,000

Scenario 2: Dual Income Couple, Combined ₹1,50,000/month

- Combined gross income: ₹1,50,000/month

- Existing EMIs: ₹0

- Available for home loan EMI (28% rule): ₹42,000/month

- Affordable loan at 8.5%, 20 years: ₹36,18,000 approx

- Required down payment (20%): ₹9,04,500

- Affordable home price: ₹45,22,500

Scenario 3: Mid-Career Professional, ₹1,20,000/month

- Gross income: ₹1,20,000/month

- Existing EMIs: ₹18,000 (personal + car loan)

- Available for home loan EMI (28% rule): ₹33,600 − ₹18,000 = ₹15,600/month

- Affordable loan at 8.5%, 20 years: ₹13,45,200 approx

- Key insight: Existing debts dramatically reduce affordability — clearing the personal loan first would increase home loan eligibility by ₹5–₹8 lakhs

Scenario 4: Senior Professional, ₹2,50,000/month, Age 45

- Gross income: ₹2,50,000/month

- Existing EMIs: ₹0

- Maximum tenure: 15 years (retire at 60)

- Affordable EMI at 28%: ₹70,000/month

- Affordable loan at 8.5%, 15 years: ₹71,40,000 approx

- Required down payment (20%): ₹17,85,000

- Affordable home price: ₹89,25,000

Scenario 5: NRI Buyer, Remittance Income ₹2,00,000/month

- Income: ₹2,00,000/month equivalent

- Existing EMIs: ₹0

- Available for home loan EMI (28%): ₹56,000/month

- NRI home loan rates: 8.5–9.5% (slightly higher than resident rates)

- Affordable loan at 9%, 20 years: ₹46,75,200 approx

- Affordable home price with 20% down: ₹58,44,000

Step-by-Step: Using the Mortgage Calculator for Your Home Purchase

Step 1 — Calculate your maximum comfortable EMI Multiply your gross monthly income by 28%. Subtract all existing monthly EMIs. The result is your maximum home loan EMI.

Step 2 — Enter this EMI into the calculator Set the EMI amount, choose a realistic interest rate (use current market rates + 0.5% buffer for safety), and select your desired tenure (15–20 years recommended).

Step 3 — Note the loan amount This is your maximum mortgage loan. Add your down payment savings to find your maximum affordable home price.

Step 4 — Calculate total cost of ownership Add estimated monthly property tax, insurance, maintenance, and society fees to your EMI. Ensure the total is below 35% of gross income.

Step 5 — Apply the 3X annual income sanity check Multiply your annual gross income by 3. Your home price should not significantly exceed this number. If it does, you are stretching beyond comfortable affordability.

Step 6 — Add 10–15% buffer for emergencies Your affordability calculation should never assume perfect conditions. Rates may rise, income may fluctuate. Build in a conservative buffer.

👉 Run all 6 steps in under 60 seconds with our free Mortgage Calculator →

Government Home Loan Schemes for First-Time Buyers: 2025 Update

Many developing market governments offer subsidised home loan programs for first-time buyers — significantly improving affordability for middle-income families:

| Country | Scheme | Benefit | Income Eligibility |

|---|---|---|---|

| 🇮🇳 India | PMAY — Pradhan Mantri Awas Yojana | 3–6.5% interest subsidy on home loan | Up to ₹18 lakhs annual income |

| 🇵🇭 Philippines | Pag-IBIG Housing Loan | Below-market rates from 5.75% | Pag-IBIG members |

| 🇳🇬 Nigeria | FMBN National Housing Fund | Subsidised rates from 9–11% | NHF contributors |

| 🇧🇷 Brazil | Minha Casa Minha Vida | Subsidised rates 4–8.16% | Up to R$8,000 family income |

| 🇰🇪 Kenya | KMRC Affordable Housing | Below-market mortgage rates | Kenya citizen, first-time buyer |

In India specifically, the PMAY subsidy can reduce effective interest cost by ₹2.67 lakhs to ₹2.35 lakhs on eligible loans — making it one of the most valuable benefits available to first-time middle-income buyers. Always check eligibility before applying for any home loan.

Frequently Asked Questions

Q: How much home loan can I get on a ₹50,000 salary? A: With a ₹50,000 gross monthly salary and no existing EMIs, most banks will approve a home loan where EMI ≤ 50% of income (₹25,000/month). At 8.5% for 20 years, this translates to an eligible loan of approximately ₹21,55,000. However, your comfortable budget using the 28% rule is ₹14,000/month EMI — equivalent to approximately ₹12,07,000 loan. The difference represents the gap between what a bank approves and what is genuinely comfortable.

Q: Should I take a home loan for 20 years or 30 years? A: 20 years is recommended for most buyers — it balances a manageable EMI with significantly less total interest than a 30-year loan. A 30-year tenure on ₹30 lakhs at 8.5% costs approximately ₹21 lakhs more in interest than a 20-year tenure, while saving only ₹6,000/month in EMI. Take 30 years only if the 20-year EMI genuinely exceeds 35–40% of your income.

Q: What credit score do I need for the best home loan rate? A: A credit score of 750+ gets you the best advertised rates from most banks. Between 700–750 you typically qualify for standard rates. Below 700, you may face higher rates or require a co-applicant. A 6-month credit improvement effort before applying (paying all dues on time, reducing credit card utilisation below 30%) can push a 700 score to 750+ and save lakhs in interest.

Q: Is it better to buy a ready-to-move home or an under-construction property? A: Ready-to-move properties offer immediate possession and tax benefits from day one — Section 24(b) interest deduction applies immediately. Under-construction properties are often cheaper but carry delivery risk, and interest paid during construction can only be claimed in 5 equal instalments after possession. For first-time buyers without alternative accommodation, ready-to-move significantly reduces financial and timing risk.

Q: How much should my emergency fund be before buying a home? A: Maintain a minimum of 6 months of ALL post-purchase expenses as emergency fund — this means 6 months of (new mortgage EMI + property tax + maintenance + society fees + all other living expenses). Do not use your emergency fund as part of the down payment. Buying a home while depleting your emergency fund is one of the highest-risk financial decisions you can make.

Q: Can I afford a home if I already have a car loan? A: Yes, but your home loan eligibility will be reduced by your car loan EMI. Banks subtract all existing EMIs from your available home loan capacity. If your car loan EMI is ₹10,000/month and your 28% rule budget is ₹28,000/month total, you have only ₹18,000 available for home loan EMI. Use our Mortgage Calculator to see exactly how your car loan affects your home affordability.

Conclusion

The mortgage calculator is not just a tool for calculating EMI. It is a financial compass that tells you exactly where you stand before you make the most consequential financial commitment of your life.

Used correctly — with real income numbers, real existing debt obligations, real interest rate assumptions, and the full cost of ownership — it prevents the single most common and most costly mistake in personal finance: buying more home than you can truly afford.

The 28% rule, the 3X income rule, and the 20% down payment rule together create a simple, powerful framework that has protected homeowners from financial stress across generations and continents.

Know your number before you fall in love with a property. Because once you have seen the home, felt the excitement, and imagined your future there — rational financial analysis becomes very difficult.

Use the calculator first. View properties second.

👉 Find your exact affordable home price with our free Mortgage Calculator → 👉 Related Reading: How Banks Calculate Your Home Loan Eligibility → 👉 Related Reading: Home Loan vs Rent — Which is Cheaper in 2025? → 👉 Related Reading: Down Payment Calculator — How to Buy a House Faster → 👉 Related Reading: Fixed vs Floating Rate Mortgage — 10-Year Cost Comparison → 👉 Related Reading: Mortgage Refinancing Calculator — When Does It Make Sense? → 👉 Related Reading: EMI vs Lump Sum Repayment — Which Saves More Money? →