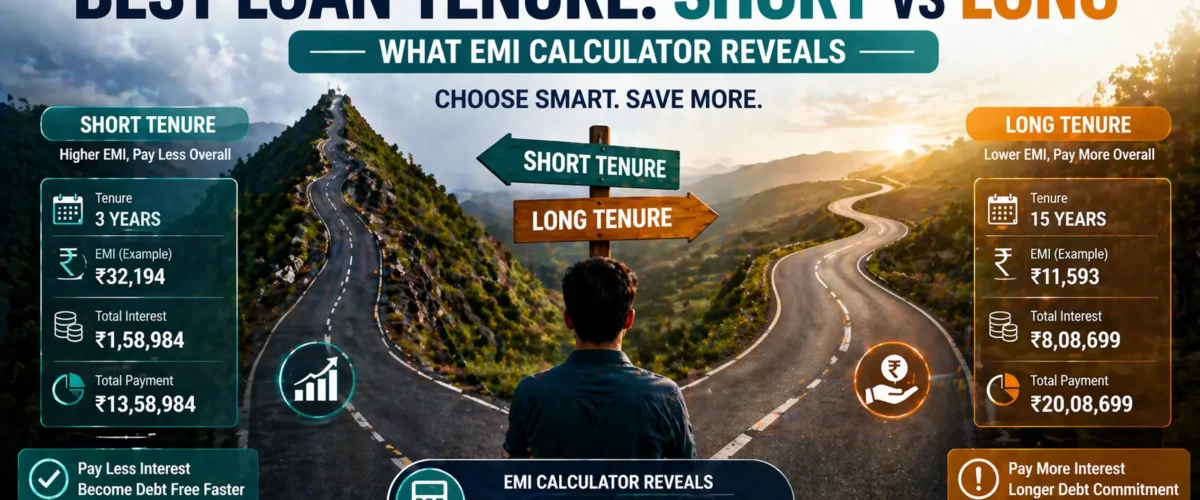

When you apply for a loan, the bank offers you a choice that most people make in 30 seconds without truly understanding the consequences — the loan tenure.

Choose too long and you quietly hand the bank lakhs of extra rupees in interest over the years. Choose too short and your monthly budget becomes dangerously tight, leaving you vulnerable to any financial emergency.

Get this one decision right and you can save ₹5 lakhs to ₹25 lakhs over the life of a home loan — without earning a single rupee more.

Here is exactly what the EMI calculator reveals about short vs long loan tenure — with real numbers for every loan type.

👉 Compare different tenures for your loan instantly with our free Loan EMI Calculator →

The Core Tradeoff: Nobody Explains This Clearly Enough

Every loan tenure decision comes down to one fundamental tradeoff:

Shorter tenure = Higher monthly EMI + Much less total interest paid Longer tenure = Lower monthly EMI + Much more total interest paid

Neither is automatically better. The right choice depends on your income, loan type, financial goals, and whether you plan to make prepayments. Let the numbers guide you — not the bank’s suggestion.

The EMI Calculator Reveals: ₹20 Lakh Loan at 9%

| Tenure | Monthly EMI | Total Amount Paid | Total Interest Paid | Interest as % of Loan |

|---|---|---|---|---|

| 5 years | ₹41,513 | ₹24,90,780 | ₹4,90,780 | 24.5% |

| 10 years | ₹25,335 | ₹30,40,200 | ₹10,40,200 | 52.0% |

| 15 years | ₹20,285 | ₹36,51,300 | ₹16,51,300 | 82.6% |

| 20 years | ₹17,995 | ₹43,18,800 | ₹23,18,800 | 115.9% |

| 25 years | ₹16,789 | ₹50,36,700 | ₹30,36,700 | 151.8% |

| 30 years | ₹16,092 | ₹57,93,120 | ₹37,93,120 | 189.7% |

Read that last row carefully: on a 30-year loan at 9%, you pay back nearly 3 times the original loan amount — ₹57.9 lakhs on a ₹20 lakh loan. The bank collects ₹37.9 lakhs in interest alone.

Choosing 10 years instead of 30 years on the same loan saves ₹27.5 lakhs in interest — but requires paying ₹9,243 more per month.

👉 Run this calculation for your exact loan amount with our Home Loan EMI Calculator →

Home Loan Tenure: The Right Choice by Income Level

The most important rule in home loan tenure selection: your total EMI payments should not exceed 40% of your monthly take-home salary.

| Monthly Take-Home | Home Loan Amount | Max Safe EMI (40%) | Recommended Tenure | Interest Rate |

|---|---|---|---|---|

| ₹30,000 | ₹15,00,000 | ₹12,000 | 20–25 years | 8.5% |

| ₹50,000 | ₹20,00,000 | ₹20,000 | 15–20 years | 8.5% |

| ₹75,000 | ₹30,00,000 | ₹30,000 | 12–15 years | 8.5% |

| ₹1,00,000 | ₹40,00,000 | ₹40,000 | 12–15 years | 8.5% |

| ₹1,50,000 | ₹55,00,000 | ₹60,000 | 10–12 years | 8.5% |

| ₹2,00,000 | ₹70,00,000 | ₹80,000 | 10 years | 8.5% |

Note: These are recommended ranges. If you plan to make regular prepayments, you can take a longer tenure initially and pay it off faster — which leads us to the smartest strategy of all.

👉 Related Reading: Mortgage Calculator — How Much Home Can You Afford? → — calculate your maximum safe loan amount before choosing tenure.

Personal Loan Tenure: Keep It As Short As Possible

Personal loans carry higher interest rates (10–26% p.a.) than home loans. This makes tenure choice even more critical — every extra year of personal loan tenure is significantly more expensive than the equivalent year on a home loan.

| Loan: ₹3 Lakh Personal Loan at 15% | Tenure | Monthly EMI | Total Interest | Total Paid |

|---|---|---|---|---|

| 1 year | ₹27,098 | ₹25,176 | ₹3,25,176 | |

| 2 years | ₹14,534 | ₹48,816 | ₹3,48,816 | |

| 3 years | ₹10,399 | ₹74,364 | ₹3,74,364 | |

| 5 years | ₹7,137 | ₹1,28,220 | ₹4,28,220 |

Choosing 5 years instead of 2 years on a ₹3 lakh personal loan at 15% costs you an extra ₹79,404 in interest — more than 26% of the original loan amount — just for the convenience of a lower monthly payment.

The personal loan tenure rule: Never exceed 3 years. Ideally repay in 1–2 years.

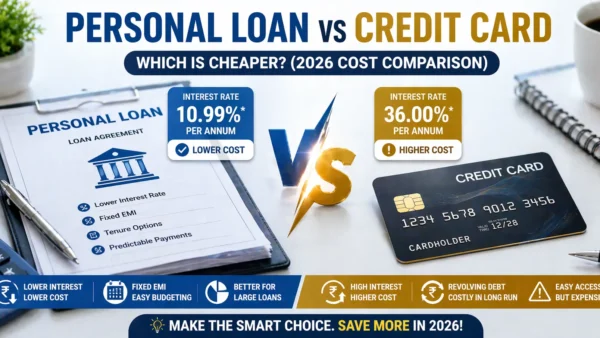

👉 Related Reading: Personal Loan vs Credit Card — Which Is Cheaper? → — if you’re choosing between these two, the tenure decision is critical to total cost.

Car Loan Tenure: The 5-Year Limit Rule

Cars depreciate fast. A new car loses 20–30% of its value in year one alone. Taking a 7-year car loan creates the dangerous “underwater” situation — where you owe the bank more than the car is actually worth.

| ₹6 Lakh Car Loan at 10% | 3 Years | 5 Years | 7 Years |

|---|---|---|---|

| Monthly EMI | ₹19,354 | ₹12,748 | ₹9,870 |

| Total Interest Paid | ₹96,744 | ₹1,64,880 | ₹2,29,080 |

| Car Market Value at End | ₹2,80,000 | ₹2,10,000 | ₹1,60,000 |

| Loan Fully Cleared? | ₹0 owed | ₹0 owed | ₹0 owed |

| Extra Interest vs 3yr | — | +₹68,136 | +₹1,32,336 |

A 7-year car loan costs ₹1,32,336 more in interest than a 3-year loan on the same ₹6 lakh. That is nearly 22% of the car’s original price — paid purely in extra interest for choosing a longer tenure.

The car loan rule: Maximum 5 years. Choose 3 years if your budget allows.

👉 Related Reading: Car Loan EMI Calculator — What Banks Don’t Tell You → — the full guide to hidden car loan costs.

When Short Tenure Wins Clearly

Choose a shorter loan tenure when:

- Your monthly income is stable and growing — you can comfortably afford a higher EMI today

- You are in the early years of a high-interest loan (personal, car) — shorten to minimise total interest

- Interest rates are high (above 10%) — the longer you borrow, the more you pay at high rates

- You are approaching retirement and want to be debt-free before income drops

- You have a windfall incoming (bonus, maturity) that will help you clear the loan faster

- You want to build wealth through investments sooner — being debt-free faster frees up capital

👉 Related Reading: EMI vs Lump Sum Repayment — Which Saves More Money? → — using windfalls smartly to cut your loan tenure.

When Long Tenure Makes Practical Sense

Choose a longer loan tenure when:

- The shorter tenure EMI would exceed 40% of your monthly income — financial safety first

- You are early in your career with current lower income but clear growth trajectory ahead

- The loan carries significant tax benefits (home loan interest deduction) that reduce effective rate

- You want to maintain investment liquidity — keeping EMI low means more cash for SIP

- You are taking a home loan and plan to make aggressive annual prepayments anyway

- You have multiple financial obligations — other loans, school fees, ageing parents — competing for income

The key insight: a long tenure with planned prepayments often outperforms a short tenure without them. Flexibility has genuine financial value.

👉 Related Reading: How to Reduce Your Home Loan EMI by 30% → — strategies to benefit from both low EMI and reduced interest cost.

The Smartest Strategy: Start Long, Prepay Hard

This is what financially savvy borrowers do — and it is the best of both worlds:

Step 1: Take a 20-year home loan (lower EMI, better monthly cash flow) Step 2: Invest the EMI difference (vs a 10-year loan) into a SIP every month Step 3: Every year, use SIP returns or salary bonus to make a lump sum prepayment Step 4: Watch your actual repayment timeline shrink toward 12–14 years organically Step 5: Enjoy low EMI pressure every month while still saving massively on total interest

| Scenario | Loan | Rate | Tenure | Monthly EMI | Total Interest | Actual Payoff |

|---|---|---|---|---|---|---|

| 10-year loan (rigid) | ₹40L | 8.5% | 10 years | ₹49,611 | ₹19,53,320 | 10 years |

| 20-year loan, no prepayment | ₹40L | 8.5% | 20 years | ₹34,874 | ₹43,69,760 | 20 years |

| 20-year loan + ₹1L/year prepayment | ₹40L | 8.5% | 20 years | ₹34,874 | ₹28,41,000 | ~14 years |

The third scenario gives you the low EMI of a 20-year loan (₹34,874 vs ₹49,611) while achieving a payoff in ~14 years and paying only ₹8.87 lakhs more in interest than the rigid 10-year option — with dramatically less monthly financial stress throughout.

👉 Model your prepayment strategy with our Home Loan Prepayment Calculator → 👉 Related Reading: EMI vs Lump Sum Repayment — Which Saves More? →

Tenure Change After Taking the Loan: Is It Possible?

Yes — and this is an underused option that many borrowers don’t know about.

| Situation | What You Can Do | Cost |

|---|---|---|

| Want to reduce tenure | Make regular prepayments and ask bank to keep EMI same | Usually free |

| Want to extend tenure (cash flow stress) | Request formal tenure extension from bank | Small processing fee |

| Refinancing to new lender | Choose any new tenure while transferring | Standard balance transfer costs |

| After prepayment | Ask bank to reduce tenure (keeping EMI same) rather than reduce EMI | Free — always choose this option |

The prepayment rule: After every prepayment, always instruct your bank to reduce tenure, not EMI. Reducing tenure saves far more total interest. Reducing EMI keeps you in debt longer. This one instruction, repeated consistently, can save lakhs over the loan life.

👉 Related Reading: How to Reduce Your Home Loan EMI by 30% → — full strategies for tenure and EMI optimisation.

Tenure Impact Across Different Loan Types: Summary

| Loan Type | Ideal Tenure | Maximum Sensible Tenure | Key Reason |

|---|---|---|---|

| Home Loan | 10–15 years | 20 years (with prepayments) | Large amount justifies longer tenure; tax benefits reduce effective rate |

| Car Loan | 3 years | 5 years (absolute max) | Car depreciates fast; long tenure risks underwater situation |

| Personal Loan | 1–2 years | 3 years (absolute max) | High rate makes every extra year very expensive |

| Education Loan | 5–7 years | 10 years | Moratorium period + time to establish income is reasonable |

| Gold Loan | 6–12 months | 24 months | Short-term liquidity tool — not a long-term debt product |

| Business Loan | 3–5 years | 7 years | Loan should be repaid from business profits within one business cycle |

Tenure Comparison Across Developing Markets

| Country | Typical Home Loan Tenure | Max Available | Culture/Norm |

|---|---|---|---|

| 🇮🇳 India | 15–20 years | 30 years | 20 years most common; prepayment culture growing |

| 🇵🇭 Philippines | 10–20 years | 25 years | 15 years typical for Pag-IBIG loans |

| 🇳🇬 Nigeria | 5–10 years | 15 years | Short tenures due to high interest rates (15–22%) |

| 🇧🇷 Brazil | 20–30 years | 35 years | Long tenures due to high prices relative to income |

| 🇰🇪 Kenya | 10–20 years | 25 years | 15 years typical; shorter due to high rates |

| 🇵🇰 Pakistan | 10–20 years | 25 years | Islamic finance (diminishing musharakah) common |

Frequently Asked Questions

Q: Can I change my loan tenure after taking the loan? A: Yes. You can request a tenure extension from your bank (subject to approval, usually with a small fee). You can effectively reduce tenure at any time by making prepayments and asking the bank to keep your EMI the same. You can also choose a new tenure when refinancing to a new lender.

Q: What is the maximum tenure for a home loan in India? A: Most banks in India offer home loans up to 30 years. However, the practical maximum is constrained by your age — the loan must typically be fully repaid by age 60–65 (retirement age). A 35-year-old can get a 25-year loan; a 45-year-old may only qualify for 15 years.

Q: Is a 30-year home loan ever a good idea? A: Only if a shorter tenure makes your EMI unaffordable (above 40% of income). A 30-year tenure means paying approximately 2.5–3x the original loan amount in total. Always pair a very long tenure with a committed plan for annual prepayments to reduce the total interest damage.

Q: What tenure should I choose for a personal loan? A: The shortest tenure you can comfortably afford — ideally 12–24 months, maximum 36 months. Personal loans carry 10–26% interest rates. Every extra year at these rates is unnecessarily expensive. Never take a personal loan for 5 years when 2 years is achievable.

Q: Should I reduce EMI or reduce tenure when making a prepayment? A: Always reduce tenure. Reducing EMI keeps you in debt longer and costs more in total interest. Reducing tenure gets you debt-free faster and saves significantly more money. This applies to every loan type — home, car, and personal. Every time you prepay, instruct your bank to reduce tenure.

Q: My bank is suggesting a 20-year loan but I can afford a 15-year EMI. Which should I choose? A: Choose what fits your income comfortably — not what the bank suggests. Banks earn more interest on longer tenures, so they naturally prefer you take the longest possible tenure. Calculate the total interest difference, ensure the higher EMI leaves you with 20–25% of income as monthly savings buffer, and choose accordingly.

Conclusion

The loan tenure decision is one of the most financially consequential choices you make — yet most people spend less than 5 minutes on it.

The EMI calculator reveals the full truth: every extra year of loan tenure costs you real money — not a small amount, but often lakhs of rupees that could have funded your investments, your children’s education, or your own early retirement.

The optimal strategy for most borrowers: choose the shortest tenure your budget comfortably supports, with a 20–25% income buffer for savings and emergencies. If you have a home loan, pair any tenure with a plan for annual prepayments to close it faster.

Your future self — debt-free years earlier and lakhs richer — will thank you.

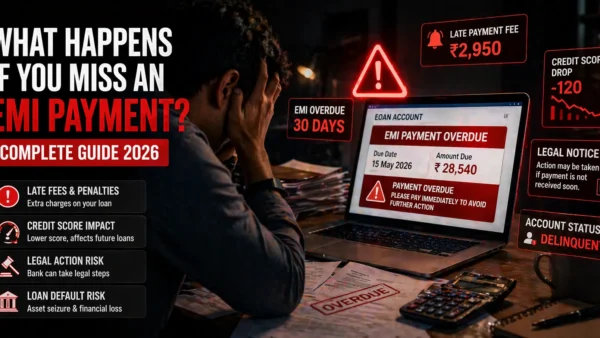

👉 Use our free Loan Tenure Calculator → to compare every tenure option for your loan amount and rate — see your total cost difference in seconds. 👉 Related Reading: How to Calculate EMI for Personal Loan → 👉 Related Reading: EMI vs Lump Sum Repayment — Which Saves More? → 👉 Related Reading: How to Reduce Your Home Loan EMI by 30% → 👉 Related Reading: What Happens If You Miss an EMI Payment? →