You need ₹1 lakh urgently.

Your credit card has the limit available. Your bank is offering a pre-approved personal loan. Both feel like easy options.

But here is the truth most people discover too late: choosing the wrong option can cost you ₹30,000–₹80,000 more in interest on the exact same amount of money.

This complete 2025 comparison shows you exactly which option is cheaper — with real numbers — so you never make an expensive mistake out of convenience again.

👉 Calculate your personal loan EMI instantly with our free Personal Loan EMI Calculator →

The Core Difference Nobody Talks About

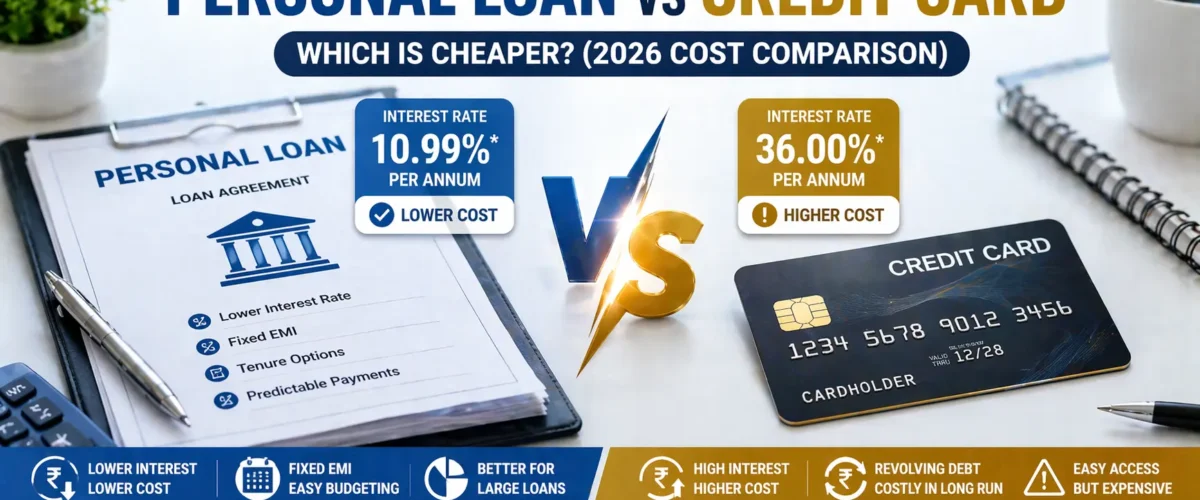

Both personal loans and credit cards are unsecured debt — meaning no collateral required. But their interest rate structures are completely different, and that difference is enormous.

| Feature | Personal Loan | Credit Card (Revolving) | Credit Card (EMI) |

|---|---|---|---|

| Interest Rate | 10–26% p.a. | 36–42% p.a. | 12–18% p.a. |

| Interest Calculation | Reducing balance | Daily compounding on outstanding | Reducing balance |

| Repayment Structure | Fixed EMI, fixed end date | Flexible minimum due (dangerous) | Fixed EMI, fixed tenure |

| Processing Time | 1–3 days (pre-approved: instant) | Instant (card already active) | Instant (conversion) |

| Pre-closure Charges | 1–5% | None | 1–3% |

| Effect on Credit Score | Hard inquiry on application | High utilisation hurts score | Moderate impact |

The critical number: credit card revolving interest at 36–42% p.a. is 2–3 times more expensive than a personal loan at 14%. This is not a small difference — it is the difference between manageable debt and a debt trap.

Interest Rate Comparison: The Real Numbers

| Product | Typical Annual Rate | Monthly Rate | Interest on ₹1 Lakh for 12 months |

|---|---|---|---|

| Personal Loan (Top Bank) | 10–13% p.a. | 0.83–1.08% | ₹5,499–₹7,029 |

| Personal Loan (NBFC) | 15–22% p.a. | 1.25–1.83% | ₹8,665–₹12,868 |

| Credit Card EMI Conversion | 12–18% p.a. | 1–1.5% | ₹6,620–₹9,783 |

| Credit Card Revolving Balance | 36–42% p.a. | 3–3.5% | ₹21,232–₹25,271 |

| Buy Now Pay Later (BNPL) | 24–36% p.a. | 2–3% | ₹14,054–₹21,232 |

| Informal/App Loans | 60–120%+ p.a. | 5–10%+ | ₹34,000–₹1,20,000+ |

The difference between a personal loan at 13% and revolving credit card debt at 40% on ₹1 lakh over one year is ₹15,733 in extra interest — roughly the cost of a weekend holiday or two months of groceries, simply thrown away.

Real Cost Comparison: ₹1 Lakh Debt — Side by Side

| Option | Rate | Monthly Payment | Months to Pay Off | Total Paid | Total Interest |

|---|---|---|---|---|---|

| Personal Loan | 14% p.a. | ₹9,621/month | 12 months | ₹1,15,452 | ₹15,452 |

| Credit Card EMI (12 months) | 15% p.a. | ₹9,026/month | 12 months | ₹1,08,312 | ₹8,312 |

| Credit Card — Pay ₹10,000/month | 40% p.a. | ₹10,000/month | 14 months | ₹1,32,800 | ₹32,800 |

| Credit Card — Pay ₹5,000/month | 40% p.a. | ₹5,000/month | 28 months | ₹1,52,400 | ₹52,400 |

| Credit Card — Pay minimum due only | 40% p.a. | ~₹2,500/month | 72+ months | ₹1,80,000+ | ₹80,000+ |

The minimum due trap is devastating. Paying only the minimum on ₹1 lakh of credit card debt can take 6+ years to clear and cost ₹80,000 in interest alone — 80% of the original amount.

A personal loan clears the same debt in 12 months for just ₹15,452 in interest.

👉 See the exact cost of your debt with our free Loan Repayment Calculator →

When a Personal Loan is Clearly the Better Choice

Choose a personal loan when:

- You need more than ₹50,000 and cannot repay it within 1–2 months

- You want a structured repayment plan with a guaranteed end date

- You are planning a large expense — home renovation, medical treatment, wedding, education

- You already carry a revolving credit card balance at 36–42% interest

- You need more than 6 months to comfortably repay

- Your credit score is strong enough (700+) to get a competitive rate

👉 Related Reading: How to Calculate EMI for Personal Loan → — understand exactly what your monthly payment will be before you borrow.

When a Credit Card is the Better Choice

Use your credit card (responsibly) when:

- You can pay the full outstanding amount before the due date — this uses the 30–45 day interest-free period, making it literally free money

- The purchase qualifies for a genuine 0% EMI offer from the merchant (verify no hidden processing fees)

- The amount is small (under ₹20,000) and your salary hits within 2–3 weeks

- You earn significant reward points or cashback that meaningfully offset the cost

- You need instant access to funds and a personal loan cannot be processed in time

The golden rule of credit cards: they are free if paid in full every month, and extremely expensive if not.

The Credit Card EMI Option: Middle Ground

Most banks offer a credit card EMI conversion — turning your outstanding balance or a new purchase into fixed monthly instalments at 12–18% p.a. This is significantly cheaper than revolving credit (36–42%) but slightly more expensive than a good personal loan (10–14%).

| Option | Rate | Total Interest on ₹1 Lakh (12 months) | Verdict |

|---|---|---|---|

| Personal Loan (good credit) | 11% | ₹6,043 | Cheapest |

| Credit Card EMI Conversion | 15% | ₹8,241 | Middle |

| CC Revolving (paying ₹10K/month) | 40% | ₹32,800 | Expensive |

When to choose CC EMI over personal loan:

- When the personal loan processing takes too long

- When your bank offers 0% or very low-rate CC EMI on specific merchants

- When your personal loan rate would be high due to lower credit score

The Debt Consolidation Play: Use Personal Loan to Wipe Out Credit Card Debt

If you currently have revolving credit card debt at 36–42% interest, taking a personal loan at 14–18% to clear it completely is one of the best financial moves you can make.

| Scenario | CC Debt | CC Interest Rate | Personal Loan Rate | Annual Interest Saving |

|---|---|---|---|---|

| Example 1 | ₹1,00,000 | 40% (₹40,000/yr) | 15% (₹15,000/yr) | ₹25,000/year |

| Example 2 | ₹3,00,000 | 40% (₹1,20,000/yr) | 15% (₹45,000/yr) | ₹75,000/year |

| Example 3 | ₹5,00,000 | 40% (₹2,00,000/yr) | 15% (₹75,000/yr) | ₹1,25,000/year |

Consolidating ₹5 lakh of credit card debt into a personal loan saves ₹1.25 lakhs every year — money that used to go straight to the bank now stays in your pocket.

The consolidation rules:

- Take a personal loan for the exact outstanding credit card amount

- Immediately pay off all credit card balances — completely

- Cut up or freeze the credit cards to prevent re-accumulation

- Pay your personal loan EMI faithfully every month

- Do not use the freed-up credit card limit as an excuse to spend again — this is where most people fail

👉 Calculate your debt consolidation EMI with our Personal Loan EMI Calculator → 👉 Related Reading: How to Use a Financial Calculator to Escape the Debt Trap →

Impact on Credit Score: Which is Safer?

Both personal loans and credit cards affect your credit score — but in different ways.

| Action | Credit Score Impact |

|---|---|

| Applying for personal loan | Hard inquiry: -5 to -10 points temporarily |

| Taking personal loan and repaying on time | Positive: +15 to +40 points over 12 months |

| Credit card utilisation above 30% | Negative: -20 to -50 points (ongoing) |

| Credit card utilisation above 70% | Negative: -50 to -100 points (severe) |

| Missing personal loan EMI | -50 to -100 points per miss |

| Missing credit card minimum due | -50 to -100 points per miss |

| Clearing credit card debt with personal loan | Positive: score often improves as utilisation drops |

One hidden advantage of the personal loan consolidation strategy: your credit utilisation ratio drops immediately when you pay off credit card balances with a personal loan. A lower utilisation ratio directly improves your credit score — often by 40–80 points within 30 days.

👉 Related Reading: What Happens If You Miss an EMI Payment? → — understand the full consequences before committing to any repayment plan.

Comparing Processing Time: When Speed Matters

| Option | Processing Time | Documents Required |

|---|---|---|

| Pre-approved Personal Loan | Instant to 2 hours | None (pre-approved) |

| Regular Personal Loan | 1–3 working days | ID, income proof, bank statements |

| Credit Card (already active) | Instant | None |

| Credit Card EMI Conversion | Instant (via app/call) | None |

| Credit Card Balance Transfer | 3–7 working days | Minimal |

For genuine emergencies where money is needed within hours, a pre-approved personal loan or credit card is your fastest option. Check your banking app right now — most banks display pre-approved loan offers with a single click.

Country-Specific Rates 2025

| Country | Personal Loan Rate | Credit Card Rate | Cost Difference on ₹1L equiv. (12 months) |

|---|---|---|---|

| 🇮🇳 India | 10–18% p.a. | 36–42% p.a. | ₹15,000–₹25,000 more with CC |

| 🇵🇭 Philippines | 15–30% p.a. | 36–48% p.a. | ₱12,000–₱20,000 more with CC |

| 🇳🇬 Nigeria | 20–30% p.a. | 24–36% p.a. | Smaller gap — compare carefully |

| 🇧🇷 Brazil | 30–50% p.a. | 200–300%+ p.a. | R$15,000–₹20,000+ more with CC |

| 🇰🇪 Kenya | 15–25% p.a. | 24–42% p.a. | KSh 8,000–₹18,000 more with CC |

Brazil deserves special mention — credit card revolving interest in Brazil can exceed 300% per year, one of the highest in the world. A personal loan in Brazil, despite its own high rates, is dramatically cheaper than carrying any credit card balance.

The ₹2,000 Rule: Your Credit Card Decision Test

Before using a credit card for any purchase, ask yourself one question:

“Can I pay this entire amount on my next statement due date?”

- Yes → Use the credit card. Earn rewards. Pay zero interest.

- No → Use a personal loan or wait until you have the cash.

That single question, applied consistently, prevents virtually every credit card debt disaster.

Frequently Asked Questions

Q: Is a credit card better than a personal loan for small amounts? A: Only if you can repay the full amount before the statement due date — using the 30–45 day interest-free grace period. If you will carry any balance month to month, a personal loan is almost always cheaper, even for small amounts.

Q: Can I convert my credit card balance to a personal loan? A: Yes — many banks offer a balance transfer to personal loan program at 12–16% p.a. This is significantly cheaper than revolving credit card interest of 36–42%. Call your bank and ask specifically for a “credit card balance transfer to personal loan” option.

Q: What is the difference between credit card EMI and personal loan EMI? A: Credit card EMI is a conversion of your card balance into instalments — rates are typically 12–18% with minimal processing. A personal loan is a separate credit product requiring fresh application and assessment, with rates from 10–26% depending on your profile. For larger amounts and good credit profiles, personal loans often beat CC EMI rates.

Q: Which damages my credit score more — missing a personal loan EMI or a credit card payment? A: Both are equally damaging to your credit score — a missed payment is a missed payment regardless of product type. However, high credit card utilisation (using more than 30–40% of your credit limit) also independently reduces your score even without missing any payment — an additional risk that personal loans do not carry.

Q: Should I close my credit card after consolidating debt into a personal loan? A: Do not close it — closing a card reduces your total available credit limit, which increases your utilisation ratio and can hurt your score. Instead, keep the card active with a small recurring charge (like a subscription) that you pay in full each month. This builds positive history without any risk of revolving debt.

Conclusion

The choice between a personal loan and a credit card is not about which one is more convenient — it is about which one costs you less over time.

For any amount you cannot fully repay within 30 days, a personal loan at 10–18% is almost always cheaper than revolving credit card debt at 36–42%. The numbers prove it every time.

Use the credit card for its genuine superpower — the 30–45 day interest-free period on purchases you pay in full. Use a personal loan for everything else that needs financing.

👉 Calculate your exact personal loan cost with our free Personal Loan EMI Calculator → 👉 Compare debt consolidation options with our Loan Repayment Calculator → 👉 Related Reading: How to Calculate EMI for Personal Loan → 👉 Related Reading: Best Loan Tenure — Short vs Long EMI Explained → 👉 Related Reading: How to Use a Financial Calculator to Escape the Debt Trap →