You work hard for your money every single month.

The very least your money can do is work hard back for you.

But millions of people across India, Philippines, Nigeria, Kenya, and Brazil are quietly losing the wealth-building race — not because they are not saving, but because they are saving in the wrong place.

SIP, Fixed Deposit, or Recurring Deposit — which one actually builds the most wealth in 2025?

We ran the actual numbers. The results are more dramatic than most people realise.

👉 See exactly how your money grows with our free Investment Returns Calculator →

The Quick Answer (Before the Deep Dive)

| Investment | Best For | Returns | Risk | Inflation Beating? |

|---|---|---|---|---|

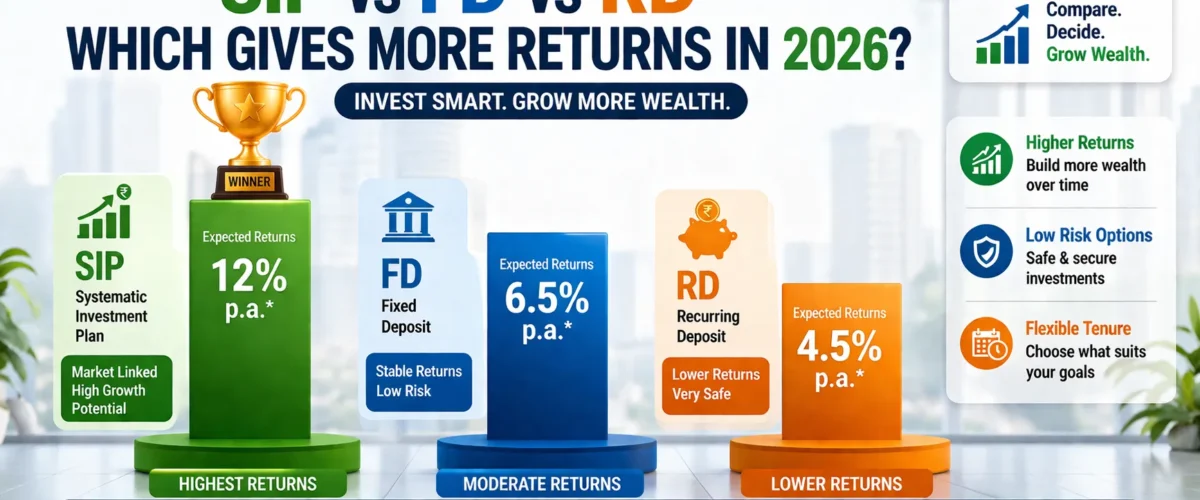

| SIP (Equity) | Long-term wealth building (7+ years) | 10–14% p.a. | Medium-High | Strongly Yes |

| Fixed Deposit | Short-term safety (1–3 years) | 6–7.5% p.a. | Zero | Barely |

| Recurring Deposit | Disciplined short-term saving | 5.5–7% p.a. | Zero | No |

If you have more than 7 years before you need the money — SIP wins. Every single time. By a large margin.

If you need the money within 1–3 years and cannot afford any risk — FD wins. Safety and certainty matter more than returns over short horizons.

Now let us prove it with data.

Understanding Each Investment: What You Are Actually Buying

SIP (Systematic Investment Plan) A monthly investment into equity mutual funds — which are diversified portfolios of stocks professionally managed or index-tracked. Returns are market-linked, meaning they fluctuate year to year but have historically averaged 10–14% over long periods. You are buying ownership in India’s (or your country’s) top businesses.

Fixed Deposit (FD) A lump sum deposited with a bank for a fixed period at a guaranteed interest rate. The bank lends your money to borrowers at higher rates and keeps the difference. Completely safe, completely predictable — but the guaranteed rate is almost always lower than inflation over the long term.

Recurring Deposit (RD) Essentially a monthly version of an FD — you deposit a fixed amount every month and receive interest on the growing balance. Same safety and predictability as FD, with slightly lower rates. Designed for people who save regularly rather than having a lump sum to deploy.

Head-to-Head Comparison: Every Key Factor

| Feature | SIP (Equity) | Fixed Deposit | Recurring Deposit |

|---|---|---|---|

| Average Returns | 10–14% p.a. | 6–7.5% p.a. | 5.5–7% p.a. |

| Risk Level | Medium-High (market fluctuation) | Zero | Zero |

| Minimum Investment | ₹100–₹500/month | ₹1,000 lump sum | ₹100/month |

| Lock-in Period | None (most funds) | 7 days to 10 years | 6 months to 10 years |

| Premature Withdrawal | Anytime (exit load may apply for < 1 year) | Penalty of 0.5–1% | Penalty varies |

| Liquidity | High — redeemable in 1–3 working days | Low during tenure | Low during tenure |

| Tax on Returns | LTCG 12.5% above ₹1.25L (equity) | Added to income, taxed at slab rate | Added to income, taxed at slab rate |

| Inflation Beating? | Yes — strongly over long term | Barely (1% real return) | No (negative real return) |

| Government Protection | SEBI regulated | DICGC insured up to ₹5 lakhs | DICGC insured up to ₹5 lakhs |

| Best Tenure | 7–30+ years | 1 month–5 years | 6 months–5 years |

The Numbers That Change Everything: ₹5,000/Month for 20 Years

Same person. Same monthly discipline. Same ₹5,000. Different vehicle. Vastly different outcome.

| Investment | Monthly Amount | Annual Return | Total Invested | Maturity Value | Total Profit |

|---|---|---|---|---|---|

| SIP (Equity MF) | ₹5,000 | 12% | ₹12,00,000 | ₹49,95,740 | ₹37,95,740 |

| Fixed Deposit (monthly) | ₹5,000 | 7% | ₹12,00,000 | ₹26,20,100 | ₹14,20,100 |

| Recurring Deposit | ₹5,000 | 6.5% | ₹12,00,000 | ₹24,52,130 | ₹12,52,130 |

| Savings Account | ₹5,000 | 3.5% | ₹12,00,000 | ₹17,30,295 | ₹5,30,295 |

After 20 years of the same ₹5,000 monthly discipline:

- SIP investor: ₹49.96 lakhs

- FD investor: ₹26.20 lakhs

- RD investor: ₹24.52 lakhs

- Savings account: ₹17.30 lakhs

The SIP investor ends up with ₹23.76 lakhs more than the FD investor — on the exact same monthly investment. That gap represents a second home down payment, full funding for a child’s education abroad, or 5+ years of comfortable retirement income.

👉 Compare all three options for your exact monthly investment with our SIP vs FD Calculator →

Extending the Horizon: 30-Year Comparison

The true power of SIP only reveals itself over longer time horizons. Let us extend the comparison to 30 years:

| Investment | Monthly | Return | 10-Year Value | 20-Year Value | 30-Year Value |

|---|---|---|---|---|---|

| SIP (Equity) | ₹5,000 | 12% | ₹11,61,695 | ₹49,95,740 | ₹1,76,49,569 |

| Fixed Deposit | ₹5,000 | 7% | ₹8,65,296 | ₹26,20,100 | ₹60,93,435 |

| Recurring Deposit | ₹5,000 | 6.5% | ₹8,39,421 | ₹24,52,130 | ₹55,86,710 |

At 30 years, the SIP investor has ₹1,76,49,569 — nearly ₹1.16 crore more than the FD investor. The gap does not grow arithmetically. It grows exponentially. The longer the investment horizon, the more dramatically SIP outperforms.

👉 Related Reading: How to Become a Millionaire with SIP Calculator → — the complete guide to reaching ₹1 Crore through SIP.

The Inflation Reality Check: What Are You Actually Earning?

Nominal returns are what the bank or fund house advertises. Real returns are what you actually earn after inflation steals its share. This distinction is critical — and almost nobody explains it clearly.

| Investment | Nominal Return | Inflation (India avg 2024–25) | Real Return | What This Means |

|---|---|---|---|---|

| SIP (Equity) | 12% | 5–6% | +6 to +7% | Your wealth genuinely grows |

| Fixed Deposit | 7% | 5–6% | +1 to +2% | Barely keeping up |

| Recurring Deposit | 6.5% | 5–6% | +0.5 to +1.5% | Almost breaking even |

| Savings Account | 3.5% | 5–6% | -1.5 to -2.5% | Actively losing wealth |

| Cash at Home | 0% | 5–6% | -5 to -6% | Guaranteed wealth destruction |

The savings account is not a safe investment. It is a guaranteed, slow-motion wealth destruction machine. Every year your money sits in a savings account, it loses 1.5–2.5% of its real purchasing power.

FD and RD are marginally better — but at 1% real return, they are barely keeping pace with inflation. You are running on a treadmill.

Only SIP is genuinely building wealth — earning 6–7% in real terms above inflation.

👉 Related Reading: How to Use an Investment Calculator to Beat Inflation → — the complete guide to inflation-proof investing.

Tax Impact: What You Actually Keep After Tax

The comparison changes further when you apply the real-world tax treatment of each investment. This is where FD and RD lose even more ground.

Fixed Deposit Tax: Interest earned is added to your income every year and taxed at your slab rate — 5%, 20%, or 30%. For anyone in the 30% bracket, FD’s 7% nominal return becomes just 4.9% after tax — barely above inflation.

Recurring Deposit Tax: Same as FD — interest is taxed at slab rate each year. Fully taxable, no exemption.

SIP (Equity Mutual Fund) Tax: Long-term capital gains (holding 12+ months) are taxed at 12.5% — but only on gains above ₹1.25 lakh per year. Gains below ₹1.25 lakh are completely tax-free. You also only pay tax when you actually sell — not every year like FD/RD.

| Scenario: ₹10,000/month for 20 years | FD (7%) | SIP (12%) |

|---|---|---|

| Maturity Value | ₹52,40,200 | ₹99,91,480 |

| Total Gain | ₹28,40,200 | ₹75,91,480 |

| Tax Rate | 30% (high earner) | 12.5% LTCG (on excess above ₹1.25L) |

| Approx Tax Payable | ₹8,52,060 | ₹9,28,310 (approx, on large gains) |

| After-Tax Wealth | ₹43,88,140 | ₹90,63,170 |

| After-Tax Difference | SIP wins by ₹46.75 lakhs |

Even after accounting for taxes, SIP generates over ₹46 lakhs more than FD over 20 years on the same ₹10,000 monthly investment.

When Should You Choose Each Investment?

This is the most practical question — and the answer is not always SIP.

Choose SIP When:

- Your investment horizon is 7 years or longer — time smooths out market volatility

- You are building wealth for retirement, child’s education, or a long-term goal

- You can psychologically handle seeing your portfolio value fluctuate month to month

- You want to beat inflation meaningfully over the long run

- You want tax efficiency — LTCG rate is significantly lower than income slab rates

Choose Fixed Deposit When:

- You need the money within 1–3 years — FD gives certainty that SIP cannot

- This is your emergency fund — guaranteed access and guaranteed returns matter more than growth

- You are a senior citizen benefiting from higher FD rates (typically 0.25–0.5% extra)

- You have just retired and cannot afford any portfolio volatility on this portion of wealth

- You are saving for a specific short-term goal — wedding, car down payment, vacation

Choose Recurring Deposit When:

- You are completely new to saving and need the discipline of a mandatory monthly deduction

- Your risk tolerance is genuinely zero — you cannot sleep with any uncertainty about the amount

- The savings goal is specific and short-term — school fees next year, appliance purchase, travel fund

- You want a simple, no-thinking-required savings product alongside other investments

👉 Related Reading: How Much SIP Per Month to Retire at 45? → — if your goal is early retirement, SIP is your primary vehicle.

The Intelligent Investor Strategy: Use All Three Together

The smartest investors do not choose between SIP, FD, and RD. They use each one for the specific purpose it is best suited for:

| Purpose | Best Vehicle | Amount |

|---|---|---|

| Emergency Fund (3–6 months expenses) | Fixed Deposit | Non-negotiable — keep this here |

| Short-term goals (1–3 years) | FD or Debt Mutual Fund | Specific goal amount |

| Medium-term goals (3–7 years) | Hybrid Mutual Fund SIP | Growing monthly |

| Long-term wealth building (7+ years) | Equity SIP | Maximise as income allows |

| Retirement corpus | Equity SIP + NPS | Largest allocation |

The allocation rule by age:

- Age 25–35: 70–80% SIP equity, 20–30% FD/debt

- Age 35–45: 60–70% SIP equity, 30–40% FD/debt

- Age 45–55: 50% SIP equity, 50% FD/debt

- Age 55+: 30–40% equity, 60–70% FD/debt/stable

👉 Related Reading: Tax-Saving Investment Calculator — 5 Best Options for 2025 → — how to combine tax-saving instruments with SIP and FD optimally.

SIP vs FD vs RD Across Developing Markets

Current 2025 rates vary significantly by country — affecting which vehicle makes the most sense locally.

| Country | Typical FD Rate | Typical RD Rate | Equity SIP Historical Return | SIP Advantage |

|---|---|---|---|---|

| 🇮🇳 India | 6.5–7.5% | 6–7% | 12–14% CAGR | +5 to +7% per year |

| 🇵🇭 Philippines | 3–5% | 3–4% | 8–12% (UITF equity) | +5 to +8% per year |

| 🇳🇬 Nigeria | 15–20% | 12–18% | 15–25% (equity funds) | Smaller gap — compare carefully |

| 🇧🇷 Brazil | 10–12% (Tesouro) | 10–12% | 12–18% (equity) | Moderate SIP advantage |

| 🇰🇪 Kenya | 10–14% | 9–13% | 12–18% (equity) | Moderate SIP advantage |

Important note for Nigeria and Kenya: When FD rates are already in the 15–20% range (as in Nigeria), the risk-adjusted advantage of equity SIP narrows significantly. In high-interest-rate environments, FDs become more competitive relative to equity. Always compare the real return (nominal rate minus local inflation) before deciding.

The SIP Market Crash Test: What Really Happens?

The most common fear about SIP: “What if the market crashes right when I need my money?”

This is a legitimate concern — but the data shows SIP investors who stayed invested through every major crash came out dramatically ahead.

| Market Event | SIP Response | Outcome for Investors Who Continued |

|---|---|---|

| 2008 Global Financial Crisis (-52% fall) | SIP bought heavily at low prices | Those who continued saw 100%+ gains by 2010 |

| 2011 European Debt Crisis (-25% fall) | Continued SIP accumulated cheaply | Recovery and gains within 18 months |

| 2020 COVID Crash (-40% in March) | SIP at record low NAVs | Market recovered fully within 6 months |

| 2022 Rate Hike Correction (-15%) | Continued SIP benefited | Recovery and new highs within 12 months |

The rule: Market crashes are a SIP investor’s best friend, not worst enemy. The worst thing you can do during a crash is stop your SIP. The best thing you can do is increase it.

Frequently Asked Questions

Q: Is SIP guaranteed to give better returns than FD? A: Over 10+ years, equity SIPs have consistently outperformed FDs historically in all major markets. But SIP returns are not guaranteed — they depend on market performance. FD returns are contractually guaranteed. The trade-off is risk vs reward. For any horizon above 7 years, history strongly favours SIP. For anything shorter, FD’s certainty has genuine value.

Q: Can I do both SIP and FD simultaneously? A: Absolutely — and this is the recommended approach. Keep 3–6 months of expenses in an FD as your untouchable emergency fund. Invest everything beyond that emergency fund in equity SIP for long-term wealth building. The two serve completely different purposes and complement each other perfectly.

Q: What happens to my SIP during a market crash? A: During a crash, your monthly SIP investment buys more mutual fund units at lower prices — this is the Rupee Cost Averaging advantage. Investors who continued SIP through every major crash in history ended up significantly wealthier than those who paused or stopped. The math consistently rewards those who stay the course.

Q: Is RD or FD better for short-term goals? A: FD usually offers slightly higher rates (0.25–0.5% more) than RD and works better if you have a lump sum. RD is better if you only have a regular monthly surplus and want structured saving discipline. For returns alone, FD marginally wins — but RD wins for building the saving habit.

Q: At what income level should I start SIP? A: There is no minimum income level — SIP starts at ₹100–₹500 per month on most platforms. The right time to start is whenever you have any surplus after essential expenses. Even ₹1,000/month started at age 22 grows to ₹35+ lakhs by age 52. Start with whatever you have today.

Q: How do I choose a mutual fund for SIP? A: For beginners, a low-cost Nifty 50 or Sensex index fund is ideal — it mirrors the market, has minimal fees (0.1–0.2% expense ratio), and removes fund manager selection risk. For those with 10+ year horizons, a diversified flexi-cap or multi-cap fund adds growth potential. Avoid sector funds and thematic funds until you have solid experience.

Conclusion

The data is unambiguous: for any goal that is 7 years or more away, SIP in equity mutual funds generates dramatically more wealth than FD or RD on the same monthly investment.

The gap is not small. It is ₹23–₹47 lakhs more on just ₹5,000–₹10,000 per month over 20 years. It is the difference between a comfortable retirement and a financially stressed one. It is the difference between funding your child’s dream education and falling short.

But FD and RD are not wrong — they are simply the right tool for the wrong job when used for long-term wealth building. Keep them for their genuine purpose: safety, certainty, and short-term goals.

Use SIP for what it is genuinely built for: building serious, inflation-beating, life-changing long-term wealth.

The best investment strategy is not choosing one — it is using all three for the purpose each serves best.

👉 Compare SIP vs FD vs RD for your exact investment amount with our free Investment Returns Calculator → 👉 Related Reading: How to Become a Millionaire with SIP Calculator → 👉 Related Reading: Step-Up SIP Calculator — Grow Wealth 3X Faster → 👉 Related Reading: Compound Interest Calculator — The 8th Wonder of the World → 👉 Related Reading: How to Use an Investment Calculator to Beat Inflation → 👉 Related Reading: Tax-Saving Investment Calculator — 5 Best Options for 2025 →