What if I told you that investing just ₹5,000 a month — the cost of a few restaurant meals — could make you a millionaire?

Most people think becoming a millionaire requires a high salary, a lucky stock pick, or inheriting money from a rich uncle.

The truth? It requires nothing but a simple SIP and time.

In this article, you’ll discover exactly how the SIP calculator works, how much you need to invest monthly to reach ₹1 Crore (or $1 Million), and the biggest mistakes that stop ordinary people from building extraordinary wealth.

💰 Start Here: Use our Free SIP Calculator → to find your millionaire number in 30 seconds.

🤔 What is SIP and Why is it the World’s Most Powerful Wealth Tool?

SIP stands for Systematic Investment Plan.

It simply means investing a fixed amount of money every month into a mutual fund — automatically, without thinking about it.

It’s not glamorous. It’s not exciting. But it is devastatingly effective.

Here’s why SIP is the most powerful wealth-building tool available to ordinary people in developing markets:

- ✅ Start with as little as ₹500 or $10/month

- ✅ No need to time the market

- ✅ Works even during market crashes (you buy more units cheap)

- ✅ Compound interest grows your money exponentially over time

- ✅ Fully automated — set it and forget it

🔗 See how compounding works: Compound Interest Calculator →

🧮 What Does a SIP Calculator Show You?

A SIP calculator is a free tool that answers the most important investment question:

“If I invest X amount every month at Y% return for Z years — how much will I have?”

You just enter 3 numbers:

| Input | Example |

|---|---|

| Monthly Investment Amount | ₹5,000 |

| Expected Annual Return | 12% |

| Investment Duration | 20 years |

| Result: Total Wealth Created | ₹49,95,740 |

| Your Total Investment | ₹12,00,000 |

| Profit from Compounding | ₹37,95,740 |

That’s ₹38 lakhs in pure profit from investing just ₹5,000/month. No risk-taking. No stock picking. No luck needed.

💡 Run your own numbers: SIP Calculator — Try It Free →

🏆 The Millionaire Blueprint: How Much SIP to Reach ₹1 Crore?

Here’s the most searched question on the internet about SIP:

“How much SIP per month to become a Crorepati?”

The answer depends on how many years you have. Here’s the complete table:

| Monthly SIP Amount | Annual Return | Years to ₹1 Crore |

|---|---|---|

| ₹2,000 | 12% | 30 years |

| ₹3,500 | 12% | 25 years |

| ₹5,500 | 12% | 22 years |

| ₹10,000 | 12% | 18 years |

| ₹20,000 | 12% | 14 years |

| ₹50,000 | 12% | 9 years |

The lesson? The earlier you start, the less you need to invest every month.

Starting at age 25 vs 35 can mean a difference of ₹40,000/month in required SIP to reach the same goal.

🔗 Find your personal number: SIP Millionaire Calculator →

🌍 Global Millionaire SIP Goals by Country

Not from India? Here’s what the millionaire target looks like in your currency:

| Country | Millionaire Target | Monthly SIP (12% return, 20 yrs) |

|---|---|---|

| 🇮🇳 India | ₹1 Crore | ₹10,000/month |

| 🇵🇭 Philippines | ₱5,000,000 | ₱5,200/month |

| 🇳🇬 Nigeria | ₦500,000,000 | ₦520,000/month |

| 🇧🇷 Brazil | R$1,000,000 | R$1,050/month |

| 🇰🇪 Kenya | KSh 13,000,000 | KSh 13,600/month |

| 🇵🇰 Pakistan | PKR 2,80,00,000 | PKR 29,000/month |

💡 Note: Returns vary by country and fund type. Use our calculator for accurate local projections.

📈 The Magic of Compounding — Why Time Beats Money

Albert Einstein reportedly called compound interest “the 8th wonder of the world.”

Here’s why that statement is so powerful with a real example:

Meet Priya and Anjali — same salary, very different futures:

| Priya (Starts at 25) | Anjali (Starts at 35) | |

|---|---|---|

| Monthly SIP | ₹5,000 | ₹5,000 |

| Annual Return | 12% | 12% |

| Invests Until Age | 55 | 55 |

| Years Invested | 30 years | 20 years |

| Total Invested | ₹18,00,000 | ₹12,00,000 |

| Final Wealth | ₹1,76,49,569 | ₹49,95,740 |

Priya invested only ₹6 lakhs MORE than Anjali — but ended up with ₹1.27 CRORE MORE.

That extra ₹1.27 crore came from nothing but 10 extra years of compounding.

This is why every financial expert in the world says: “The best time to start a SIP was yesterday. The second best time is today.”

🔗 See your compounding growth: Compound Interest Calculator →

💡 Step-Up SIP Strategy — Reach ₹1 Crore 3x Faster

Most people do a regular SIP. Smart investors do a Step-Up SIP.

A Step-Up SIP means increasing your SIP amount by 10–15% every year — in line with your salary hike.

Here’s the difference it makes:

| Strategy | Monthly SIP (Year 1) | Annual Increase | Wealth at 20 Years |

|---|---|---|---|

| Regular SIP | ₹10,000 | 0% | ₹99,91,480 |

| Step-Up SIP | ₹10,000 | 10% per year | ₹1,91,21,354 |

| Step-Up SIP | ₹10,000 | 15% per year | ₹2,74,33,812 |

Same starting amount. Nearly 3x the result.

When you get your annual salary raise, give a part of it to your future self through a Step-Up SIP.

🔗 Calculate Step-Up SIP: Step-Up SIP Calculator →

🔥 5 Reasons SIP is Perfect for Developing Market Investors

1. 📉 No Need to Time the Market

Markets go up and down. SIP buys more units when markets are low and fewer when they’re high — automatically averaging your cost. This is called Rupee Cost Averaging.

2. 💸 Start With Very Little Money

You don’t need to be rich to invest. In India, you can start a SIP for as low as ₹100/month. In the Philippines, some funds accept as low as ₱1,000/month.

3. 🔄 Total Flexibility

Increase, decrease, pause, or stop your SIP anytime. No penalties, no lock-in periods on most mutual funds.

4. 🛡️ Beats Inflation

Keeping money in a savings account gives you 3–4% interest. Inflation in developing markets is often 5–8%. That means your savings are actually LOSING value. A SIP returning 10–14% beats inflation comfortably.

5. 📊 Transparent and Trackable

Every rupee is tracked. You can see your investment, current value, and returns at any time — unlike real estate or gold.

⚠️ 5 SIP Mistakes That Stop People From Becoming Millionaires

Mistake #1: Starting Too Late Every year of delay costs you lakhs. There is no “right time” to start. The right time is always NOW.

Mistake #2: Stopping SIP During Market Crashes This is the single biggest wealth-destroying mistake. When markets crash, your SIP is buying units at DISCOUNT. Stopping it is like leaving a sale early.

Mistake #3: Picking the Wrong Fund Not all mutual funds are equal. A difference of just 2% in annual returns over 20 years can mean a difference of ₹30–40 lakhs in final wealth.

Mistake #4: Not Increasing SIP Over Time Your income grows every year. Your SIP should too. A fixed SIP that never increases is silently losing purchasing power to inflation.

Mistake #5: Withdrawing Early The real magic of SIP happens in the LAST few years of compounding — not the first. Withdrawing early is like blowing out the candles on your own birthday cake.

🧠 Which Mutual Fund Should You Choose for SIP?

While we don’t give specific fund recommendations (always consult a financial advisor), here are the general categories investors in developing markets use:

| Fund Type | Risk Level | Expected Returns | Best For |

|---|---|---|---|

| Large Cap Equity | Medium | 10–12% | Conservative investors |

| Mid Cap Equity | Medium-High | 12–15% | Moderate risk takers |

| Small Cap Equity | High | 14–18% | Aggressive, long-term |

| Index Fund | Low-Medium | 10–12% | Beginners |

| Balanced/Hybrid | Low-Medium | 9–11% | First-time investors |

💡 Pro Tip: Index funds are the best starting point for most first-time investors. Low fees, market-matching returns, zero fund manager risk.

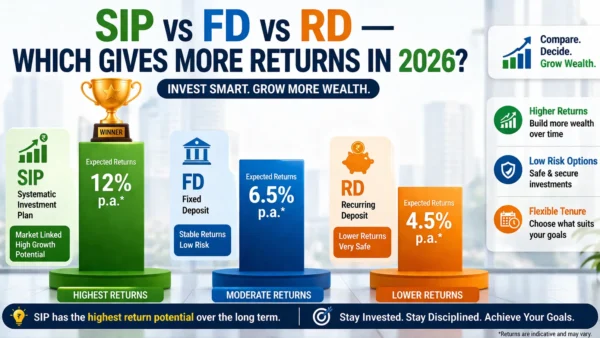

📊 SIP vs Other Investment Options — Which Wins?

| Investment | Return (10 yr avg) | Risk | Liquidity | Inflation-Beating? |

|---|---|---|---|---|

| SIP (Equity MF) | 12–14% | Medium | High | ✅ Yes |

| Fixed Deposit | 5–7% | Very Low | Medium | ❌ No |

| Gold | 8–10% | Low-Medium | Medium | ✅ Borderline |

| Real Estate | 8–12% | Low | Very Low | ✅ Yes |

| Savings Account | 3–4% | None | High | ❌ No |

| Crypto | Unpredictable | Extreme | High | ❓ Maybe |

SIP wins on the combination of returns + liquidity + accessibility + risk management. No other investment available to a common person matches this combination.

🔗 Compare all options: Investment Returns Comparison Calculator →

🎯 Your Personal SIP Action Plan — 5 Steps

Step 1: Calculate your millionaire target using our SIP Calculator →

Step 2: Choose a monthly SIP amount you can commit to — even if it’s just ₹1,000 to start

Step 3: Pick a low-cost index fund or diversified equity fund from a trusted platform

Step 4: Set up an auto-debit from your bank account on salary day (before you can spend it)

Step 5: Increase your SIP by 10% every year when you get a salary hike

That’s it. Five steps. One decision. A completely different financial future.

✅ SIP Millionaire Checklist

- Decided my monthly SIP amount

- Set a clear goal (₹1 Crore / $1 Million / retirement fund)

- Chosen a fund type suitable for my risk level

- Set up auto-debit so I never miss a payment

- Planned 10% annual Step-Up SIP increase

- Committed to NOT stopping SIP during market crashes

🔗 Related Calculators You’ll Love

- 📈 SIP Returns Calculator → — See exact returns for your SIP amount

- 🔼 Step-Up SIP Calculator → — Plan your annual SIP increase

- 💹 Lumpsum vs SIP Calculator → — Which works better for you?

- 🏦 FD vs SIP Calculator → — Compare fixed deposit vs mutual fund

- 🎯 Retirement Planning Calculator → — How much SIP to retire comfortably?

💬 Frequently Asked Questions

Q: Is SIP safe? Can I lose money? SIP in equity mutual funds carries market risk — your value can go down in the short term. However, historically, equity SIPs held for 10+ years have never given negative returns in most markets.

Q: What is the minimum SIP amount? In India, you can start with as low as ₹100–₹500/month depending on the fund. Most developing markets have similar low entry points.

Q: Can I stop my SIP anytime? Yes. Most mutual funds allow you to pause or stop your SIP without penalties. However, stopping it — especially during market downturns — is a financially costly decision.

Q: What return rate should I use in the SIP calculator? For long-term equity SIPs (10+ years), 10–12% is a reasonable and conservative estimate. Avoid using returns higher than 12% in your planning.

Q: SIP vs lumpsum — which is better? For salaried individuals, SIP is better because it spreads risk and builds discipline. For those with a large one-time amount, lumpsum during market corrections can work well. Use our Lumpsum vs SIP Calculator → to compare.

🚀 Final Word: Your Millionaire Journey Starts With One SIP

You don’t need to be born rich. You don’t need to win the lottery. You don’t need to take crazy risks.

You just need to start a SIP today, stay consistent, and let time do the heavy lifting.

The SIP calculator is your roadmap. The mutual fund is your vehicle. Compound interest is your engine.

The only thing missing is your first step.

💰 Calculate Your Millionaire SIP Number Now — It’s Free → Takes 30 seconds. No sign-up required. Results are instant.

📌 Share this article with someone who thinks becoming a millionaire is only for the rich. It might change their life.