Your gold jewellery has been sitting in a locker for years — beautiful, sentimental, and financially idle.

But right now, you need ₹2–₹3 lakhs quickly. A medical emergency. A business opportunity. A rent gap. A child’s exam fee that cannot wait.

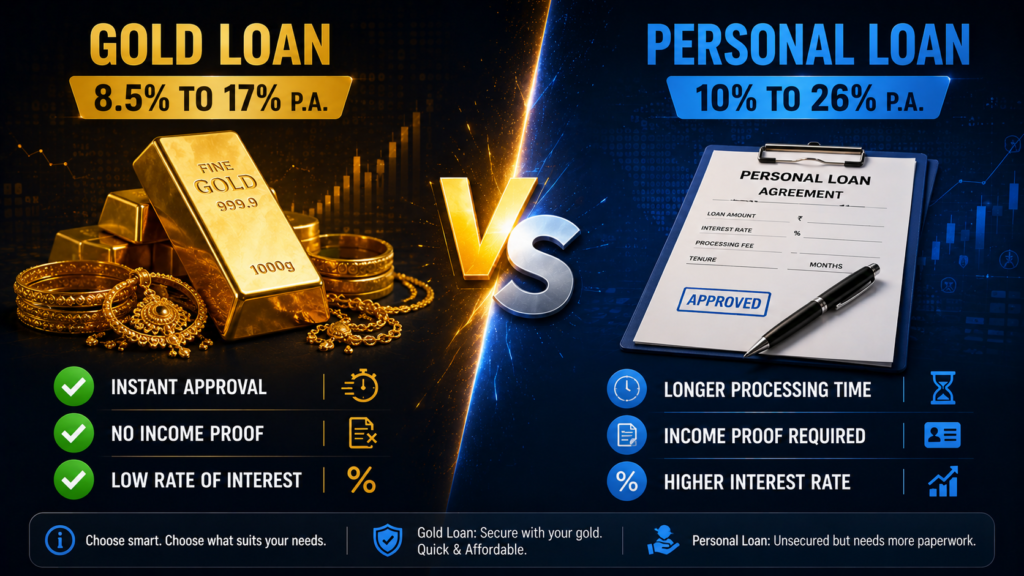

You have three options: sell the gold (and lose it permanently), apply for a personal loan (approval takes days, rates are high), or take a gold loan — get the money in 30 minutes, keep ownership of your gold, and repay on your terms.

Gold loans are one of India’s oldest and most misunderstood financial products. Used wisely, they are among the cheapest, fastest forms of credit available to any borrower. Used carelessly, they are a rollover trap that quietly consumes your jewellery.

Here is everything you need to know — with our free Gold Loan Calculator to make the decision clear in seconds.

👉 Calculate your gold loan amount and EMI instantly with our free Gold Loan Calculator →

What is a Gold Loan and How Does It Work?

A gold loan is a secured loan — you pledge your gold jewellery (or gold coins) as collateral, receive a loan of up to 75–90% of the gold’s market value, and reclaim your gold once the loan is fully repaid.

The lender holds your gold in a locked vault for the duration of the loan. You retain full ownership — the gold is never sold unless you default after multiple missed payments and legal notices.

Gold Loan Formula:

Maximum Loan Amount = Gold Weight (grams) × Current Gold Price × LTV Ratio

Example:

Gold jewellery weight: 50 grams (22 karat)

Current 22K gold price: ₹5,500/gram

Gold market value: 50 × ₹5,500 = ₹2,75,000

LTV (Loan-to-Value) ratio: 75% (RBI mandate)

Maximum loan: ₹2,75,000 × 75% = ₹2,06,250The RBI mandated a maximum LTV of 75% for gold loans in 2020 — meaning you can borrow a maximum of 75 paise for every ₹1 worth of gold pledged. This protects both borrower and lender.

Gold Loan Calculator: What It Shows You

Our Gold Loan Calculator computes four critical numbers in seconds:

| Input | What You Enter |

|---|---|

| Gold weight (grams) | Total grams of jewellery you are pledging |

| Karat purity | 18K, 22K, or 24K |

| Current gold price | Auto-updated market rate |

| Interest rate offered | Bank or NBFC rate |

| Loan tenure | 1 month to 36 months |

| Output | What You Get |

|---|---|

| Maximum eligible loan amount | Based on 75% LTV |

| Monthly interest amount | If interest-only payment opted |

| EMI (if EMI repayment) | Fixed monthly payment |

| Total interest cost | Over full tenure |

| Effective annual interest rate | True cost comparison |

👉 Use our Gold Loan Calculator → to find your eligible amount and monthly cost in 30 seconds.

Gold Loan Interest Rates 2026: Complete Lender Comparison

Interest rates on gold loans vary significantly between banks and NBFCs. Understanding who offers the best rate for your loan size and tenure can save thousands in interest:

| Lender | Interest Rate Range | Processing Fee | Max Tenure | Special Feature |

|---|---|---|---|---|

| State Bank of India (SBI) | 8.75–9.50% p.a. | 0.5% + GST | 36 months | Lowest rate — income proof required |

| HDFC Bank | 9.00–17.00% p.a. | 1% + GST | 24 months | Fast disbursement |

| ICICI Bank | 9.00–19.76% p.a. | 1% + GST | 12 months | Doorstep service available |

| Axis Bank | 10.00–17.00% p.a. | 1% + GST | 12 months | High LTV available |

| Muthoot Finance | 11.00–26.00% p.a. | 0.25–1% | 12 months | No income proof; instant |

| Manappuram Gold Loan | 12.00–28.00% p.a. | Minimal | 12 months | Online auctions; flexible |

| IIFL Gold Loan | 11.00–24.00% p.a. | 0–1% | 11 months | Doorstep gold collection |

| Bajaj Finance | 9.50–26.00% p.a. | 1% + GST | 12 months | High loan amounts |

The rate gap is enormous: SBI at 8.75% vs Manappuram at 28% — on a ₹2 lakh gold loan for 12 months, the interest cost difference is ₹17,500 vs ₹56,000. Choosing your lender carefully can save more than ₹38,000 on the same loan.

Why the gap exists:

- PSU banks (SBI, Bank of Baroda) require basic income documents and typically offer lower rates

- NBFCs (Muthoot, Manappuram) offer no-document, 30-minute disbursement but at significantly higher rates

- For urgent needs — NBFC’s speed premium may be worth paying; for planned borrowing — always go with the bank

Gold Loan Repayment Options: Choose What Fits You

Unlike most loans with a fixed EMI structure, gold loans offer three distinct repayment options — each suited to different financial situations:

Option 1: Bullet Repayment (Most Popular)

Pay nothing during the tenure — principal + accumulated interest paid as a single lump sum at the end.

| Gold Loan | ₹2,00,000 at 12% p.a. for 12 months |

|---|---|

| Monthly Payment | ₹0 (no payments during tenure) |

| Final Bullet Payment | ₹2,24,000 (principal + full year interest) |

| Best For | Seasonal income earners, farmers, business owners with irregular cash flow |

| Risk | High — if you cannot arrange ₹2,24,000 at year end, rollover trap begins |

Option 2: Interest-Only Monthly (Moderate)

Pay only the monthly interest during the tenure, repay the full principal at maturity.

| Gold Loan | ₹2,00,000 at 12% p.a. for 12 months |

|---|---|

| Monthly Interest Payment | ₹2,000/month |

| Final Principal Payment | ₹2,00,000 at maturity |

| Total Cost | ₹2,24,000 (same as bullet — just spread) |

| Best For | Those with regular monthly income who want lower monthly burden |

Option 3: EMI Repayment (Safest)

Pay fixed EMI every month (principal + interest), like a regular loan.

| Gold Loan | ₹2,00,000 at 12% p.a. for 12 months |

|---|---|

| Monthly EMI | ₹17,769/month |

| Total Paid | ₹2,13,228 |

| Total Interest | ₹13,228 |

| Best For | Salaried individuals who want systematic repayment and lower total cost |

The EMI option is always the cheapest — because you repay principal monthly, reducing the outstanding balance on which interest is calculated. The bullet option costs the same total interest as interest-only (interest on full principal throughout) — but creates the dangerous lump sum obligation.

Real Example: Gold Loan Calculator in Action

Scenario: Priya owns 45 grams of 22-karat gold jewellery. She needs ₹1.5 lakhs for her father’s medical treatment. She is comparing a gold loan vs personal loan.

Gold Loan Option (HDFC Bank, 12%, 12 months, EMI repayment)

Gold weight: 45 grams (22K)

Gold price (22K): ₹5,450/gram

Gold market value: 45 × ₹5,450 = ₹2,45,250

LTV (75%): ₹1,83,938 — Maximum eligible

Priya needs: ₹1,50,000 (within limit)

Loan: ₹1,50,000 at 12% p.a. for 12 months

Monthly EMI: ₹13,327

Total paid: ₹1,59,924

Total interest: ₹9,924

Processing fee (1%): ₹1,500

Effective total cost: ₹11,424Personal Loan Option (Bank, 16%, 12 months, same amount)

Loan: ₹1,50,000 at 16% p.a. for 12 months

Monthly EMI: ₹13,618

Total paid: ₹1,63,416

Total interest: ₹13,416

Processing fee (1.5%): ₹2,250

Effective total cost: ₹15,666Gold loan saves Priya ₹4,242 on a ₹1.5 lakh loan — simply because the secured gold reduces the lender’s risk, resulting in a lower interest rate.

And her gold jewellery? Safely locked in HDFC’s vault — returned to her in full within 24 hours of final repayment.

👉 Compare gold loan vs personal loan for your amount with our free Gold Loan Calculator →

The Rollover Trap: The Most Dangerous Gold Loan Mistake

Here is the scenario that destroys thousands of gold loan borrowers every year — particularly through NBFCs:

Month 1: You take a gold loan of ₹1,50,000 at 24% p.a. (bullet repayment)

Month 12: Repayment due — ₹1,86,000. But you do not have it.

The NBFC offers: “Rollover — just pay the ₹36,000 interest, and we extend the loan for another 12 months.”

Month 24: Now you owe ₹1,50,000 principal + another year of ₹36,000 interest = ₹1,86,000 again

Month 36: Same situation — but NBFC revalues gold (gold price may have fallen), and says your gold now covers only ₹1,20,000 of your loan. You must pay ₹30,000 immediately or they auction your gold.

The result: You paid ₹1,08,000 in rollover interest over 3 years — and still owe the original principal. The jewellery your grandmother left you is sold at auction for less than its emotional worth.

How to Avoid the Rollover Trap

- Never choose bullet repayment unless you have absolute certainty of the repayment source

- Set a repayment reminder 3 months before maturity — begin accumulating funds early

- Choose EMI repayment — your balance reduces monthly, making final repayment manageable

- Use gold loans only for short-term, specific purposes — not as rolling working capital

- If you cannot repay — contact the lender before maturity, not after. Banks and regulated NBFCs have restructuring options

Gold Loan vs Personal Loan vs LAP: Side-by-Side Comparison

| Feature | Gold Loan | Personal Loan | Loan Against Property |

|---|---|---|---|

| Collateral | Gold jewellery | None | Property |

| Approval Time | 30 minutes | 1–3 days | 7–14 days |

| Interest Rate | 8.75–28% | 10–26% | 8–14% |

| Income Proof | Not always required | Mandatory | Mandatory |

| Maximum Amount | 75% of gold value | ₹5L–₹40L (income-based) | 60–75% of property value |

| Maximum Tenure | 3 years | 5 years | 15 years |

| Credit Score Impact | Minimal if repaid | Significant inquiry | Significant inquiry |

| Risk If Default | Gold auctioned | Legal suit | Property auctioned |

| Best Use Case | Short-term urgent need | Medium-term planned expense | Large long-term need |

The verdict: Gold loan beats personal loan on rate and speed for amounts below ₹5 lakhs and tenures below 24 months — provided you have sufficient gold and a clear repayment plan.

Gold Loan Process: Step-by-Step

Taking a gold loan is one of the simplest loan processes available:

Step 1 — Bring Your Gold (Day 1)

Carry your gold jewellery, coins, or bars to the lender branch. Documents needed: ID proof (Aadhaar/PAN), address proof, one passport photo. No income documents required at most NBFCs; banks may ask for basic income proof.

Step 2 — Gold Valuation (30 Minutes)

An in-house goldsmith or certified valuer assesses your gold: purity testing (acid test or XRF machine), weight measurement, and calculation of net weight (deducting stones and non-gold components). The value is based on average of the past 30-day gold price (IBJA standard).

Step 3 — Loan Amount Determined

Based on the gold value — and the lender’s LTV ratio (up to 75% as per RBI mandate) — the maximum loan amount is offered. You choose how much you actually want to borrow.

Step 4 — Choose Repayment Option

Select bullet, interest-only, or EMI repayment. Sign the loan agreement. Carefully read: interest rate, tenure, processing fee, foreclosure charges, and auction policy for default.

Step 5 — Disbursal in 30 Minutes

Cash (up to ₹20,000 as per RBI cash restriction), NEFT, or IMPS transfer to your bank account. Some NBFCs credit within 10–15 minutes of documentation.

Step 6 — Safe Storage of Your Gold

Your gold is stored in a secured, insured vault at the lender’s branch — fully protected under the lender’s insurance. You receive a receipt describing every item pledged.

Step 7 — Repay and Reclaim

Upon full repayment — principal, interest, and any applicable charges — your gold is returned within 24 hours. In EMI repayment, gold is returned immediately on final payment.

When Gold Loan Makes Clear Financial Sense

Use a gold loan when:

- You need money urgently (medical emergency, rent gap, travel) and cannot wait for personal loan approval

- Your credit score is low or you have limited credit history — gold loan does not require a strong CIBIL score

- The amount needed is below ₹3–₹5 lakhs — gold loan rates are competitive with personal loans at these amounts

- You have a clear repayment source within 6–12 months — business income, FD maturity, family contribution

- You want to avoid a hard credit inquiry on your CIBIL report that would affect other loan applications

- The interest rate offered is meaningfully lower than your personal loan alternative rate

Avoid a gold loan when:

- You cannot clearly identify how and when you will repay — rollover risk is very real

- The amount needed far exceeds your gold’s value — gold loan cannot fully solve the problem

- You need money for over 3 years — LAP or personal loan offers longer tenures with similar rates

- The lender is unregistered or informal — only borrow from RBI-regulated banks and NBFCs

- Your gold has significant sentimental value that you cannot risk losing to auction

Gold Loan by Developing Market: Who Has Access?

Gold ownership and gold loan markets vary significantly across developing economies:

| Country | Gold Loan Prevalence | Typical Rate | Key Lenders | Notes |

|---|---|---|---|---|

| 🇮🇳 India | Very High — world’s largest market | 8.75–28% p.a. | SBI, Muthoot, Manappuram, IIFL | ₹7+ lakh crore market; South India dominant |

| 🇵🇭 Philippines | Moderate | 18–36% p.a. | Palawan Pawnshop, ML Kwarta Padala | Pawnshop model; very accessible |

| 🇳🇬 Nigeria | Low-Moderate | 25–40% p.a. | Informal pawnbrokers, some banks | Regulation limited; informal sector large |

| 🇧🇷 Brazil | Low | 30–60% p.a. | Caixa Econômica Federal | Penhor (pawn) model; limited gold jewellery culture |

| 🇰🇪 Kenya | Low | 20–35% p.a. | Pawnbrokers, some SACCOs | Growing demand; limited formal market |

| 🇱🇰 Sri Lanka | High | 18–30% p.a. | Banks and finance companies | Strong gold culture similar to South India |

India’s gold loan market is the world’s most sophisticated — with publicly listed, RBI-regulated NBFCs (Muthoot Finance is listed on NSE/BSE) offering competitive rates and strong consumer protections. Borrowers in India have significantly more protection than those using informal gold pawning in other developing markets.

Gold Loan Tax Implications

Unlike home loans — gold loans carry no income tax deduction on interest paid under any section of the Income Tax Act.

However, there is an important tax consideration if you use the gold loan proceeds for investment or business:

| Use of Gold Loan Proceeds | Interest Deduction Available? |

|---|---|

| Personal consumption (medical, travel, education) | No deduction |

| Purchase of house property | Section 24(b) deduction — up to ₹2 lakhs p.a. |

| Business investment | Business expense — fully deductible |

| Investment in assets (rental property) | Deductible against income from that asset |

| Stock market investment | No specific deduction |

If you take a gold loan to fund a business — the interest is fully deductible as a business expense, reducing your taxable profit. Maintain clear documentation of the purpose of the loan proceeds for this deduction.

👉 Related Reading: How to Save Tax Using Home Loan — Complete Guide → — comparison of tax benefits across different loan types.

Frequently Asked Questions

Q: What types of gold are accepted for a gold loan?

A: Banks and NBFCs accept gold jewellery (18 to 24 karat) and RBI-approved gold coins (up to 50 grams). Gold bars, digital gold, gold ETFs, and Sovereign Gold Bonds are generally NOT accepted as collateral. The purity and weight of your jewellery determines the eligible loan amount.

Q: What happens to my gold if I cannot repay?

A: After a missed payment, lenders follow a process: reminder notices, legal notice, then auction after a mandatory notice period (typically 30–60 days for regulated lenders). The gold is auctioned, proceeds applied to outstanding loan + interest + charges, and any surplus returned to you. For regulated NBFCs and banks, this process is transparent. Never borrow from unregulated gold pawnbrokers who may skip these protections.

Q: Can I get a gold loan without a PAN card?

A: For loans below ₹50,000 — some lenders accept only Aadhaar. For loans above ₹50,000 — PAN is typically mandatory under income tax reporting requirements. NBFCs like Muthoot and Manappuram have simplified their documentation significantly, but PAN remains essential for larger amounts.

Q: Is it safe to pledge gold jewellery with an NBFC?

A: Yes — if the NBFC is registered and regulated by RBI. Muthoot Finance, Manappuram Gold Loan, IIFL Gold Loan, and Bajaj Finance are all publicly listed, RBI-regulated entities with stringent vault security and insurance. Verify your lender’s RBI registration before pledging. Never use unlicensed money lenders or informal pawnbrokers for gold pledging.

Q: Can I partially repay a gold loan and retrieve some gold?

A: Most lenders allow partial release of pledged gold items upon proportional repayment. For example, if you pledged three items and repay 60% of the outstanding, you can request release of items worth 60% of the total pledged value. This flexibility makes gold loans particularly suitable for situations where you may have partial funds available before full repayment.

Q: What is the difference between a gold loan and a pawn shop gold loan?

A: A bank or NBFC gold loan is governed by RBI regulations — maximum LTV of 75%, maximum rate regulated, mandatory notice before auction, full surplus returned after auction. A pawn shop may operate under the Pawnbroker Act (state-specific) with different terms, potentially higher rates, and less stringent consumer protections. Always prefer RBI-regulated lenders for gold loans.

Conclusion

A gold loan is one of the most powerful financial tools available to developing market households — instant, unsecured-feeling but actually secured, and competitive in rate when used correctly.

The gold sitting in your locker is not just jewellery. It is a financial asset that can be activated in 30 minutes without selling it, without a credit score check, and often at rates better than a personal loan.

But it is only smart when used with complete clarity about repayment. The rollover trap is real. The auction at the end of repeated defaults is real. The lost family heirloom is real.

Three rules for using a gold loan wisely:

- Know your repayment source before you pledge — not after

- Choose EMI repayment over bullet unless you have absolute certainty of a lump sum

- Borrow from a regulated lender — never from unregulated pawnbrokers

Use our free Gold Loan Calculator to find your eligible loan amount, compare EMI vs interest-only payments, and calculate the true total cost before you walk into any branch.

Your gold works for you — not against you — when you use it wisely.

👉 Calculate your gold loan amount and EMI with our free Gold Loan Calculator →

👉 Related Reading: Personal Loan vs Credit Card — Which Is Cheaper? →

👉 Related Reading: How to Calculate EMI for Personal Loan →

👉 Related Reading: What Happens If You Miss an EMI Payment? →

👉 Related Reading: EMI vs Lump Sum Repayment — Which Saves More Money? →

👉 Related Reading: How to Use a Financial Calculator to Escape the Debt Trap →

👉 Related Reading: Best Loan Tenure — Short vs Long EMI Calculator →