Your offer letter arrives. In bold letters: ₹12,00,000 Per Annum.

Your heart leaps. You start planning — the apartment upgrade, the car upgrade, the restaurant upgrade.

Then your first salary hits your account: ₹72,000.

Wait. That is only ₹8.64 lakhs a year. Where did the other ₹3.36 lakhs go?

This confusion — between what your employer says you earn (CTC) and what actually reaches your bank account (in-hand salary) — is one of the most universal experiences of first-time and experienced employees alike. And it costs people thousands in poor financial planning, incorrect loan eligibility assumptions, and lifestyle decisions based on the wrong number.

Here is the complete 2025 guide to understanding every component of your salary structure — and calculating exactly what you will actually take home every month.

👉 Calculate your exact in-hand salary from any CTC with our free Salary After Tax Calculator →

The Three Numbers Every Employee Must Understand

Before calculations, understand the three completely different salary figures that cause most of the confusion:

CTC (Cost to Company): The total annual cost your employer incurs to employ you. Includes your salary, employer’s PF contribution, gratuity provision, health insurance, and any other benefits. This is the number on your offer letter — and it is significantly higher than what you actually receive.

Gross Salary: Your total pre-tax salary components that are actually paid to you — excluding employer contributions that go directly to third parties (PF, gratuity). CTC minus employer PF and gratuity = Gross Salary.

In-Hand / Net Salary: The actual amount credited to your bank account every month. Gross salary minus all deductions — income tax (TDS), employee PF, professional tax, and any other deductions. This is the only number that actually funds your life.

The Relationship:

CTC → minus employer contributions → GROSS SALARY

Gross Salary → minus all deductions → IN-HAND SALARY

Rule of thumb (varies by income level):

In-hand = 70–85% of CTC

(Higher income = lower % due to higher tax; lower income = higher %)Anatomy of a Salary Structure: Every Component Explained

A typical Indian private sector salary is divided into multiple components — each with different tax treatment:

Earning Components (What the Employer Pays You)

| Component | Typical % of CTC | Taxability | Notes |

|---|---|---|---|

| Basic Salary | 35–50% of CTC | Fully taxable | Foundation — drives PF, gratuity, HRA calculation |

| HRA (House Rent Allowance) | 40–50% of Basic | Partially exempt | Up to 50% basic in metro, 40% non-metro — with rent receipts |

| Special Allowance | Whatever remains | Fully taxable | Balancing component — no exemption |

| LTA (Leave Travel Allowance) | ₹10,000–₹30,000 | Partially exempt | For actual domestic travel — twice in 4-year block |

| Medical Allowance | ₹15,000/year | Exempt (old regime) | ₹1,250/month with bills submission |

| Telephone/Internet | ₹1,200–₹2,400/year | Exempt with bills | Submit telecom bills |

| Meal Coupons (Sodexo etc.) | ₹1,500–₹2,600/month | Exempt (₹50/meal × 22 days) | Specific exemption limit |

| Performance Bonus | Varies | Fully taxable | Variable — paid quarterly/annually |

| GROSS SALARY | ~85% of CTC | Total of above components |

Employer Contribution Components (Part of CTC, Not Paid to You)

| Component | Amount | Goes To | Notes |

|---|---|---|---|

| Employer PF (EPF) | 12% of Basic Salary | Your EPF account | Part of CTC but you cannot spend it monthly |

| Employer NPS (if applicable) | 0–10% of Basic | Your NPS account | Only if employer offers NPS scheme |

| Gratuity Provision | 4.81% of Basic | Your gratuity fund | Paid on exit after 5 years; part of CTC |

| Group Health Insurance | ₹5,000–₹25,000/year | Insurance company | Benefit in kind — part of CTC |

Deductions: What Gets Subtracted From Your Gross Salary

Mandatory Deductions

| Deduction | Amount | Notes |

|---|---|---|

| Employee PF (EPF) | 12% of Basic Salary | Goes to your EPF account (not lost — it is forced savings at 8.15%) |

| Income Tax (TDS) | Based on income slab | Largest variable deduction — depends on regime, declarations |

| Professional Tax | ₹200/month (max ₹2,400/year) | State-specific — Maharashtra, Karnataka, AP, Tamil Nadu, WB etc. |

| Employee NPS (if opted) | 10% of Basic (voluntary) | Additional retirement saving |

Optional/Voluntary Deductions

| Deduction | Amount | Notes |

|---|---|---|

| Employee NPS Voluntary | Any amount | Qualifies for 80CCD(1B) deduction |

| Health Insurance Top-Up Premium | Varies | If employer policy is insufficient |

| Salary Advance Repayment | Varies | If advance taken |

| Loan EMI (salary deduction) | As agreed | Some employers deduct EMI directly |

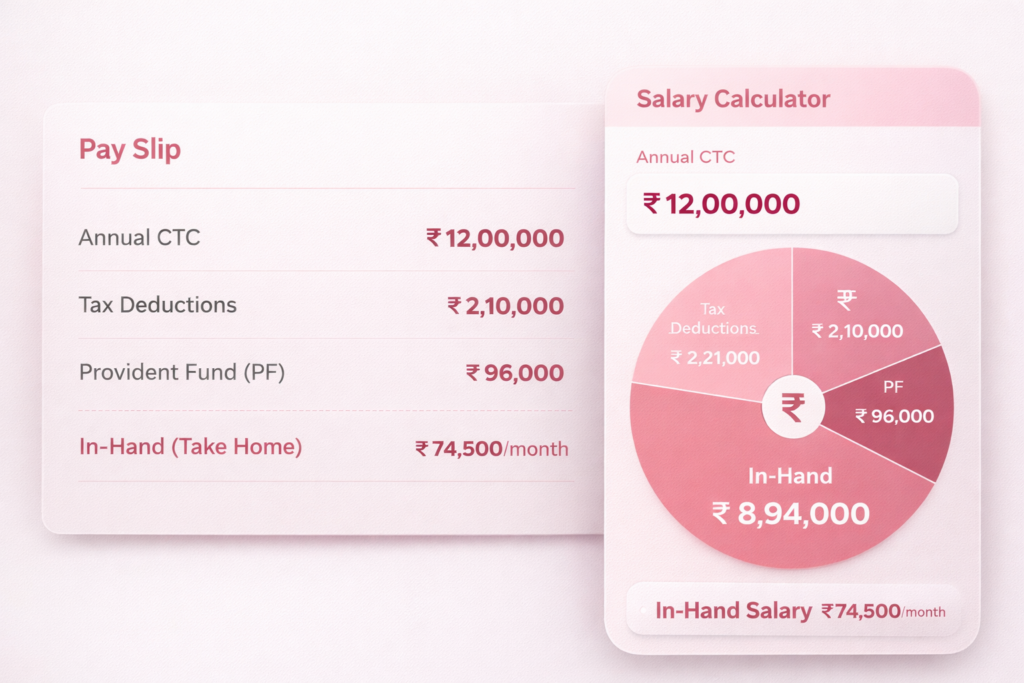

Complete CTC to In-Hand Calculation: ₹12 LPA Example

Let us do the complete calculation for a ₹12 lakh CTC employee in Mumbai under the old tax regime with all declarations:

Step 1: Break Down the CTC

| Component | Annual Amount | Monthly Amount | Notes |

|---|---|---|---|

| Basic Salary (40% of CTC) | ₹4,80,000 | ₹40,000 | |

| HRA (50% of Basic, metro) | ₹2,40,000 | ₹20,000 | |

| Special Allowance | ₹1,70,400 | ₹14,200 | Balancing amount |

| LTA | ₹20,000 | ₹1,667 | |

| Medical Allowance | ₹15,000 | ₹1,250 | |

| Meal Coupons | ₹26,400 | ₹2,200 | |

| GROSS SALARY (A) | ₹9,51,800 | ₹79,317 | |

| Employer PF (12% of Basic) | ₹57,600 | ₹4,800 | Part of CTC — not paid to employee |

| Employer NPS | ₹0 | ₹0 | Not offered |

| Gratuity Provision (4.81% Basic) | ₹23,088 | ₹1,924 | Part of CTC — not paid to employee |

| Group Health Insurance | ₹12,000 | ₹1,000 | Benefit in kind |

| TOTAL CTC | ₹12,00,000 | ₹1,00,000 | Confirms ₹12 LPA |

Step 2: Calculate Taxable Income

| Item | Annual Amount |

|---|---|

| Gross Salary | ₹9,51,800 |

| Less: Standard Deduction | −₹50,000 |

| Less: HRA Exemption (rent ₹18,000/month in Mumbai) | −₹1,50,000 (calculated — minimum of three) |

| Less: Section 80C (EPF ₹57,600 + ELSS ₹92,400) | −₹1,50,000 |

| Less: Section 80D (Health Insurance) | −₹15,000 |

| Less: Professional Tax | −₹2,400 |

| Taxable Income | ₹4,84,400 |

| Tax on ₹4,84,400 (old regime) | ₹11,720 |

| Rebate under 87A (income < ₹5L) | −₹11,720 |

| Income Tax Payable | ₹0 |

This employee pays ZERO income tax with proper planning under the old regime!

Step 3: Monthly In-Hand Salary

| Item | Monthly Amount |

|---|---|

| Gross Salary | ₹79,317 |

| Less: Employee PF (12% of ₹40,000 basic) | −₹4,800 |

| Less: Income Tax (TDS) | −₹0 (zero tax with declarations) |

| Less: Professional Tax | −₹200 |

| IN-HAND SALARY | ₹74,317/month |

| Annualised | ₹8,91,804/year |

CTC: ₹12,00,000 | Gross: ₹9,51,800 | In-Hand: ₹8,91,804

The employee takes home ₹74.3% of CTC — a gap of ₹2.58 lakhs from CTC that goes to employer PF, gratuity provision, insurance, and government.

In-Hand Salary Quick Reference Table: All Income Levels 2025

This table assumes old tax regime with standard deductions, HRA for metro city (20% rent claim), 80C fully utilised, basic = 40% of CTC:

| Annual CTC | Monthly CTC | Approx Monthly Gross | Approx Monthly In-Hand | In-Hand % of CTC |

|---|---|---|---|---|

| ₹3,00,000 | ₹25,000 | ₹21,000 | ₹19,500–₹20,500 | 78–82% |

| ₹4,00,000 | ₹33,333 | ₹28,000 | ₹26,000–₹27,500 | 78–82% |

| ₹5,00,000 | ₹41,667 | ₹35,000 | ₹32,500–₹34,000 | 78–82% |

| ₹6,00,000 | ₹50,000 | ₹42,000 | ₹38,500–₹40,000 | 77–80% |

| ₹8,00,000 | ₹66,667 | ₹56,000 | ₹50,000–₹53,000 | 75–80% |

| ₹10,00,000 | ₹83,333 | ₹70,000 | ₹61,000–₹65,000 | 73–78% |

| ₹12,00,000 | ₹1,00,000 | ₹79,000 | ₹71,000–₹75,000 | 71–75% |

| ₹15,00,000 | ₹1,25,000 | ₹1,05,000 | ₹88,000–₹93,000 | 70–74% |

| ₹18,00,000 | ₹1,50,000 | ₹1,26,000 | ₹1,03,000–₹1,09,000 | 69–73% |

| ₹20,00,000 | ₹1,66,667 | ₹1,40,000 | ₹1,12,000–₹1,18,000 | 67–71% |

| ₹25,00,000 | ₹2,08,333 | ₹1,75,000 | ₹1,35,000–₹1,43,000 | 65–69% |

| ₹30,00,000 | ₹2,50,000 | ₹2,10,000 | ₹1,58,000–₹1,68,000 | 63–67% |

| ₹40,00,000 | ₹3,33,333 | ₹2,80,000 | ₹2,00,000–₹2,15,000 | 60–65% |

| ₹50,00,000 | ₹4,16,667 | ₹3,50,000 | ₹2,40,000–₹2,60,000 | 58–62% |

Note: These are estimates. Actual in-hand varies significantly based on salary structure, city, tax regime, investment declarations, and employer-specific policies.

👉 Get your exact personalised in-hand salary with our free Salary After Tax Calculator →

New Regime vs Old Regime: Impact on In-Hand Salary

The tax regime choice directly affects your monthly take-home:

₹15 LPA CTC Employee — Regime Comparison

| Calculation Item | Old Regime | New Regime |

|---|---|---|

| Gross Salary | ₹12,50,000 | ₹12,50,000 |

| Standard Deduction | −₹50,000 | −₹75,000 |

| HRA Exemption | −₹1,20,000 | Not available |

| Section 80C | −₹1,50,000 | Not available |

| Section 80D | −₹25,000 | Not available |

| Home Loan 24(b) | −₹2,00,000 | Not available |

| NPS 80CCD(1B) | −₹50,000 | Not available |

| Taxable Income | ₹6,55,000 | ₹11,75,000 |

| Annual Tax + Cess | ₹46,176 | ₹1,21,680 |

| Monthly TDS | ₹3,848 | ₹10,140 |

| Monthly In-Hand Difference | ₹6,292 MORE with old regime |

For a ₹15 LPA employee with a home loan and investments — the old regime puts ₹6,292 more per month into their bank account. Over 12 months, that is ₹75,504 more in take-home pay — simply by choosing the right regime and submitting declarations.

👉 Related Reading: Income Tax Calculator 2025 — Save Maximum Tax Legally → — the complete guide to choosing the right tax regime and maximising every deduction.

HRA Calculation: The Biggest Exemption Most Employees Miss

HRA (House Rent Allowance) exemption is the single most impactful monthly take-home booster for employees living in rented accommodation. Yet millions of employees never claim it — either not knowing how, or assuming it is automatic.

HRA Exemption = Minimum of:

- Actual HRA received from employer

- 50% of basic (metro: Delhi, Mumbai, Kolkata, Chennai) / 40% (non-metro)

- Actual rent paid − 10% of basic salary

Example: Mumbai employee

Basic: ₹40,000/month

HRA Received: ₹20,000/month

Monthly Rent Paid: ₹18,000

Calculation:

Option 1: ₹20,000

Option 2: ₹20,000 (50% of ₹40,000 — metro)

Option 3: ₹18,000 − ₹4,000 = ₹14,000

HRA Exemption: ₹14,000/month (minimum of three)

Annual Exemption: ₹1,68,000

Tax Saved at 20% bracket: ₹34,944/year = ₹2,912/month extra in-handDocuments required for HRA claim:

- Rent receipts for every month (with ₹1 revenue stamp for rent above ₹5,000/month — though this requirement is increasingly relaxed)

- Rent agreement (registered or notarized)

- Landlord’s PAN card (mandatory if annual rent exceeds ₹1,00,000)

The parent-as-landlord strategy: If you live in your parents’ home that they own — you can legitimately pay rent to them and claim HRA exemption. Your parents declare this as rental income in their ITR. If your parents are senior citizens with low other income, their effective tax rate on the rental income may be zero — while you get the full HRA exemption saving. This is a completely legal and widely used tax planning strategy.

EPF: The Deduction That Is Actually Your Savings

The 12% Employee PF deduction surprises many employees — it feels like a loss from take-home. But EPF is not a loss — it is forced retirement saving at guaranteed 8.15% tax-free returns.

Basic Salary: ₹40,000/month

Employee EPF Contribution (12%): ₹4,800/month

Employer EPF Contribution (12%): ₹4,800/month (part of CTC)

Total Annual EPF Accumulation: ₹1,15,200

Return on your ₹57,600 contribution: 8.15% tax-free + employer match = effectively 100% return + 8.15%EPF vs alternative investment: Your ₹4,800/month contribution becomes ₹9,600/month in your EPF account (including employer match). This ₹9,600 earns 8.15% tax-free. After 20 years, ₹9,600/month at 8.15% grows to approximately ₹62.4 lakhs — entirely from a contribution that feels like ₹4,800/month.

EPF is not a salary deduction. It is forced saving that doubles immediately through employer matching — one of the best investment vehicles available to salaried employees.

Professional Tax: The Small but Mandatory Deduction

Professional tax is a state-level tax levied on salaried employees — mandatory in states like Maharashtra, Karnataka, Andhra Pradesh, Tamil Nadu, West Bengal, Gujarat, and others. Not applicable in Delhi, UP, Rajasthan, and several other states.

| State | Annual Professional Tax | Monthly Deduction |

|---|---|---|

| Maharashtra | ₹2,500 (income above ₹7,500/month) | ₹200/month (10 months) + ₹300 (February) |

| Karnataka | ₹2,400 | ₹200/month |

| Andhra Pradesh | ₹2,400 | ₹200/month |

| Tamil Nadu | ₹2,400 | ₹200/month |

| West Bengal | ₹2,400 | ₹200/month |

| Gujarat | ₹2,400 | ₹200/month |

| Delhi, UP, Rajasthan | ₹0 | Not applicable |

Professional tax is deductible from taxable income under the old regime — reducing your tax liability by the professional tax amount.

Variable Pay and Bonus: The Tax Surprise

Many employees are caught off-guard when their quarterly bonus or annual variable pay arrives — with significant TDS already deducted.

Why bonus TDS is higher than expected:

When your employer pays a bonus — they project your annual income including the bonus and calculate TDS for the entire year in that month. This can result in a large TDS deduction in the bonus month.

Example:

Monthly salary TDS: ₹3,000/month (based on base salary)

Annual bonus: ₹1,50,000 (paid in October)

In October, employer recalculates:

Annual projected income = Base salary + Bonus = ₹8,00,000 + ₹1,50,000 = ₹9,50,000

Annual TDS on ₹9,50,000 = ₹42,000

TDS already deducted (6 months × ₹3,000) = ₹18,000

Remaining TDS to collect in October = ₹42,000 − ₹18,000 = ₹24,000

October net bonus received: ₹1,50,000 − ₹24,000 = ₹1,26,000

(instead of the expected ₹1,47,000)How to minimise bonus TDS shock: Submit your investment declarations and proofs to HR well before the bonus month. Maximising declared deductions (80C, 80D, HRA, home loan) reduces the annual projected tax — and therefore the TDS deducted from your bonus.

Salary Structure Optimisation: How to Legally Increase Your In-Hand Pay

If your company offers flexible pay structuring (increasingly common in mid-to-large companies) — these components maximise your take-home legally:

High-Impact Restructuring Options

1. Maximise NPS Employer Contribution (80CCD 2) Ask HR to route part of your special allowance as employer NPS contribution. Employer NPS up to 10% of basic is completely tax-free — with no upper limit under Section 80CCD(2). This deduction is available under both old and new regimes.

Special Allowance redirected to Employer NPS: ₹4,000/month (10% of ₹40,000 basic)

Annual employer NPS: ₹48,000

Annual tax saved (30% bracket + cess): ₹14,976/year

Monthly take-home increase: ₹1,248 (from lower TDS despite same CTC)2. Increase HRA Component If your employer allows restructuring — maximise HRA to 50% of basic (metro) or 40% (non-metro). Higher HRA with legitimate rent payment increases your annual exemption.

3. Add Meal Coupons/Vouchers ₹50 per meal × 22 working days = ₹1,100/month per coupon, with maximum ₹2,200/month (two coupons) tax-free. Converting ₹2,200 of special allowance to meal coupons saves approximately ₹687/month in tax at 30% bracket.

4. Include Telephone/Internet Reimbursement ₹1,200–₹2,400/year tax-free against actual bills. Small amount, but every exemption counts.

5. Use LTA Strategically Ensure LTA is included in your CTC structure. Claim it with actual travel tickets twice in a 4-year block — converting what would be fully taxable special allowance into partially exempt LTA.

Salary After Tax Across Developing Markets: 2025 Comparison

Understanding how other developing markets structure employment taxes provides useful context:

| Country | Social Security / PF Rate (Employee) | Income Tax at ₹12L equiv. | Typical Net-to-Gross Ratio | Notable Feature |

|---|---|---|---|---|

| 🇮🇳 India | 12% EPF | 0–10% (with deductions) | 75–82% | Generous deduction system; EPF doubles with employer match |

| 🇵🇭 Philippines | SSS: 4.5%, PhilHealth: 2%, Pag-IBIG: 2% = 8.5% | 15–25% | 68–78% | TRAIN Law reformed rates; 13th month pay tax-free |

| 🇳🇬 Nigeria | Pension: 8% | 7–21% (PAYE) | 72–80% | NHF 2.5% housing fund also deducted |

| 🇧🇷 Brazil | INSS: 7.5–14% (progressive) | 7.5–27.5% (IRPF) | 60–75% | High combined deduction rate; FGTS 8% added by employer |

| 🇰🇪 Kenya | NHIF: KSh 1,700/mo, NSSF: KSh 2,160/mo | 10–30% (PAYE) | 72–80% | Affordable Housing Levy 1.5% also applies from 2023 |

| 🇵🇰 Pakistan | EOBI: 1% | 0–35% | 70–82% | Lower social security; higher income tax at upper levels |

India comparison: India’s combined employee deduction rate (12% EPF + 0–10% income tax with deductions) results in one of the more favorable net-to-gross ratios among developing markets — particularly at middle-income levels where smart tax planning can bring effective income tax to near zero.

Brazil caution: Brazil’s combined deduction rate (up to 27.5% IRPF + 14% INSS) can result in net-to-gross ratios of 60–65% for upper-middle income earners — significantly lower than India. Brazilian employees at equivalent income levels take home considerably less than Indian counterparts.

Salary Negotiation: How to Use the In-Hand Calculator as Leverage

Understanding the CTC-to-in-hand gap gives you powerful negotiating tools when evaluating job offers:

Strategy 1 — Compare Total Compensation, Not Just CTC Two offers at the same CTC can result in very different in-hand salaries based on salary structure. Request a salary breakup from any offer and calculate the actual in-hand before comparing.

Strategy 2 — Negotiate Specific Components Instead of negotiating CTC as a whole number — negotiate specific high-value components:

- Higher basic salary → higher PF accumulation (good for retirement)

- Higher HRA → more tax-exempt allowance

- NPS employer contribution → completely tax-free benefit

Strategy 3 — Value Non-Monetary Benefits Correctly Group health insurance covering family (worth ₹20,000–₹50,000/year), work from home allowance, stock options, and education reimbursement are part of total compensation that CTC calculations sometimes miss.

Strategy 4 — Account for City-Specific Tax Impact The same CTC in Delhi vs Mumbai vs Bengaluru generates slightly different in-hand due to different professional tax rates, different HRA exemption percentages, and cost of living impact on rent claims.

Salary Calculator for Different Employment Types

Freelancers and Consultants

Freelancers/consultants do not receive a structured payslip — but still need to calculate net income after tax:

Annual Freelance Income: ₹15,00,000

Less: Business Expenses (laptops, software, travel): ₹2,00,000

Less: Home Office (proportional rent + utilities): ₹60,000

Net Income Before Tax: ₹12,40,000

Tax Calculation (old regime, presumptive or actual):

Section 44ADA (50% presumptive): Taxable income = ₹7,50,000

Less: 80C, 80D, NPS: −₹2,25,000

Net Taxable: ₹5,25,000

Tax: ₹13,500 + cess = ₹14,040

Effective tax rate on ₹15L income: Just 0.9%!

Monthly net income: (₹15,00,000 − ₹14,040) ÷ 12 = ₹1,24,330/monthThe Section 44ADA presumptive taxation scheme makes consulting income extremely tax-efficient for professionals with income up to ₹50 lakhs.

Self-Employed Business Owner

Annual Business Revenue: ₹60,00,000

Less: Business Expenses (actual): ₹42,00,000

Net Profit Before Tax: ₹18,00,000

Less: Depreciation, other deductions: ₹1,00,000

Taxable Income: ₹17,00,000

Less: 80C, 80D, NPS, Home Loan: ₹4,25,000

Net Taxable: ₹12,75,000

Tax (old regime): ₹1,72,500 + cess = ₹1,79,400

Effective tax rate on ₹18L profit: 9.97%

Monthly net income: (₹18,00,000 − ₹1,79,400) ÷ 12 = ₹1,35,050/monthThe 5 Most Common Salary Misunderstandings

Misunderstanding 1 — “My CTC is my salary” CTC is what it costs the company to employ you — not what you receive. The gap includes employer PF, gratuity, insurance, and other benefits that never appear in your bank account. Always ask for the gross salary and net salary breakup — not just CTC.

Misunderstanding 2 — “EPF deduction is money lost” Employee PF is forced savings at 8.15% tax-free, matched 100% by your employer. The ₹4,800/month you contribute becomes ₹9,600/month in your EPF account. Over 20 years at 8.15%, this grows to ₹62+ lakhs. EPF is one of the best investments available to salaried employees.

Misunderstanding 3 — “I can’t reduce my TDS” TDS is calculated on your projected annual income minus your declared deductions. Submitting investment declarations (80C, 80D, home loan certificate, HRA) to your employer reduces projected taxable income and therefore monthly TDS — directly increasing your monthly take-home immediately.

Misunderstanding 4 — “New tax regime always means more take-home” For employees with home loans, investments, and HRA — the old regime often generates significantly more take-home despite higher slab rates. Always run the comparison before declaring your regime.

Misunderstanding 5 — “My bank loan eligibility equals my CTC” Banks calculate loan eligibility based on net monthly take-home — not CTC. Using CTC for loan calculations leads to serious overestimation of borrowing capacity. Always use your actual in-hand salary for all financial planning and loan eligibility calculations.

👉 Related Reading: How Banks Calculate Your Home Loan Eligibility → — understanding how lenders use your actual salary for eligibility calculation.

How to Increase Your Take-Home Salary: 8 Actionable Strategies

Strategy 1 — Submit All Investment Declarations Immediately in April Declare your planned 80C investments, home loan, HRA, and health insurance to HR at the start of the financial year. This reduces TDS from April — not February. You receive more monthly rather than waiting for a refund.

Strategy 2 — Claim HRA With Rent Receipts Every Year If you live on rent — always claim HRA with proper rent receipts and landlord PAN. This can add ₹1,500–₹5,000 per month to your take-home.

Strategy 3 — Ask for NPS Employer Contribution Employer NPS up to 10% of basic is tax-free under both regimes. Request this restructuring from HR — it reduces your TDS without reducing your total compensation.

Strategy 4 — Maximise Meal Coupons and Flexible Benefits Food coupons, telephone reimbursement, and fuel/conveyance allowances reduce taxable salary. Maximise any flexible benefits your employer offers.

Strategy 5 — Utilise Section 80CCD(1B) NPS The extra ₹50,000 NPS deduction saves ₹15,600/year at 30% bracket — increasing monthly take-home by ₹1,300/month simply by investing ₹4,167/month in NPS.

Strategy 6 — Claim LTA Regularly Submit LTA claims with travel tickets whenever eligible. Missing LTA claims forfeits a tax-free travel allowance that is part of your CTC.

Strategy 7 — Compare Regimes Annually Your optimal regime can change year to year based on income growth, new home loans, or changing investments. Run the comparison every April using our Income Tax Calculator.

Strategy 8 — File ITR and Claim Refunds Promptly If excess TDS was deducted — file ITR by July 31 and claim your refund. Refunds are typically processed within 15–45 days of e-verification. Delayed filing means delayed refund.

👉 Related Reading: Income Tax Calculator 2025 — Save Maximum Tax Legally → — maximise every deduction to increase your monthly take-home. 👉 Related Reading: Tax-Saving Investment Calculator — 5 Best Options for 2025 → — choosing the right investments to reduce TDS and save tax.

Frequently Asked Questions

Q: Why is my in-hand salary much less than my CTC? A: CTC includes employer PF (12% of basic), gratuity provision (4.81% of basic), group health insurance, and sometimes other benefits that are part of your employment cost but never reach your bank account. Additionally, TDS, employee PF (12% of basic), and professional tax are deducted from what remains. The combined effect is that in-hand is typically 70–82% of CTC depending on income level.

Q: How do I calculate my HRA exemption? A: HRA exemption is the minimum of three amounts: (1) actual HRA received, (2) 50% of basic salary (metro) or 40% (non-metro), and (3) actual rent paid minus 10% of basic salary. Use our Salary Calculator to compute your exact HRA exemption based on your salary, city, and rent paid.

Q: Does EPF deduction reduce my income tax? A: Yes — employee EPF contribution qualifies for Section 80C deduction up to ₹1.5 lakh annually under the old tax regime. So your EPF deduction is both forced retirement saving AND a tax-saving investment. The employer’s EPF contribution is also tax-free in your hands up to the 80CCD(2) limit.

Q: My employer deducted too much TDS this month — what should I do? A: Submit your investment declarations and proof documents to HR immediately. Your employer will recalculate your projected annual tax and reduce TDS for remaining months of the year. Alternatively, if the financial year has already ended — file ITR with all deductions and claim the excess as a refund.

Q: Is the 13th month salary or annual bonus taxed differently? A: No — bonus and variable pay are fully taxable at your regular income slab rate. However, the TDS pattern can appear different: employers often deduct higher TDS in the bonus month because they project the full year’s tax liability and adjust for under-deduction in prior months. The annual tax amount is the same regardless of when it is deducted.

Q: How do I calculate loan eligibility from my in-hand salary? A: Banks use your net monthly take-home salary (not CTC or gross) for loan eligibility calculation. Apply the 40–50% FOIR rule: maximum EMI equals 40–50% of net monthly take-home minus all existing EMIs. Use our Home Loan Eligibility Calculator with your actual in-hand salary for accurate results.

Conclusion

The gap between CTC and take-home salary is not a mystery — it is a formula. And once you understand every component of that formula, you can:

- Plan your monthly budget on the right number (in-hand, not CTC)

- Calculate your accurate loan eligibility

- Identify which deductions and restructuring options increase your take-home

- Choose the optimal tax regime that maximises your monthly pay

- Stop being surprised by TDS deductions and bonus tax

The most powerful immediate action for any salaried employee: submit complete investment declarations to HR in April, claim HRA with rent receipts, and run the old vs new regime comparison using our Income Tax Calculator. These three steps alone can add ₹3,000–₹10,000 per month to your take-home — without earning a single rupee more.

Use our Salary After Tax Calculator right now — enter your CTC, city, investment amounts, and rent paid — and see exactly what should be hitting your bank account every month.

👉 Calculate your exact take-home salary with our free Salary After Tax Calculator → 👉 Related Reading: Income Tax Calculator 2025 — Save Maximum Tax Legally → 👉 Related Reading: How to Save Tax Using Home Loan — Complete Guide → 👉 Related Reading: Tax-Saving Investment Calculator — 5 Best Options for 2025 → 👉 Related Reading: Capital Gains Tax Calculator — Stocks, Property & Crypto → 👉 Related Reading: How Banks Calculate Your Home Loan Eligibility → 👉 Related Reading: How to Become a Millionaire with SIP Calculator → 👉 Related Reading: GST Calculator — How GST Affects Your Business Profits →